You’ve taken the crucial first step by learning how to Check Your CIBIL Report. But the multi-page document you receive can be confusing, filled with codes and numbers. This is where the hard part ends and clarity begins.

Our free, secure tool does the heavy lifting for you; it’s the easiest way to understand the data you get when you Check Your CIBIL Report. In under 60 seconds, it analyzes your entire report, pinpoints the exact issues holding back your score, and generates a simple, personalized action plan to help you improve it. Simply upload your PDF below to turn your data into a clear roadmap for success.

The Instant Credit Report Analysis Tool

Confused by your CIBIL or Credit Report? Get a free, personalized action plan in 60 seconds.

A Note From Our Chief Editor

“Seeing a list of problems on your report can be stressful. But remember, every problem has a solution. This tool is designed to give you the clarity and confidence to take the first step. Follow the plan, be consistent, and you will see results. I’m here to guide you on this journey.” – Anwar Hashmi

Your Personalized Action Plan

Get a permanent copy of your plan and subscribe for more tips.

Join Thousands Who Have a Clearer Financial Plan

“This tool did in 60 seconds what I couldn’t figure out in 6 months. I finally have a clear, prioritized plan to improve my score. Thank you, Anwar!”

“We were so anxious about our home loan application. The Action Plan Generator identified one error on our report that we got fixed, and our score jumped 40 points!”

Your Immediate Questions, Answered

Absolutely not. When you use our tool, it only analyzes the PDF file you already have. This is considered a “soft inquiry,” just like when you check your own score. It is completely private and has zero impact on your CIBIL score.

A “Settled” or “Written-Off” status is a permanent part of your credit history for up to 7 years. While you cannot have it removed, the best course of action is to focus on building a positive payment history on all your active accounts. Over time, the impact of these old negative marks will lessen.

Significant improvement doesn’t happen overnight. If you follow a disciplined plan—paying all bills on time and reducing credit card balances—you can start to see positive changes in your score within 6 to 12 months. The most recent 24 months of your payment history have the biggest impact.

While lenders have their own policies, a general guideline is that a score of 750 or above is considered excellent and will get you the best terms on most loans, including home and personal loans. For credit cards, some lenders may have slightly more flexible criteria, but a higher score always gives you better options and higher limits.

This is a common situation. The first priority should always be to make the minimum payment on all accounts to avoid late fees and further negative marks. After that, focus any extra funds on paying down the credit card with the highest utilization (the one closest to its limit), as this can often provide the quickest boost to your score.

Ready for the Next Step in Your Journey?

Official Guide: How to Check Your CIBIL Score & Download Your Credit Report for Free (2025-26)

Before you apply for that home loan you’ve been dreaming of, or the credit card with great rewards, there’s one crucial step that can make or break your application: knowing your CIBIL score. A strong score can unlock the best offers, while a low one can lead to instant rejection.

But when you try to check your CIBIL report online, the path isn’t always clear. You’re met with dozens of websites offering a ‘free score’, often leaving you questioning if your personal data is truly safe.

As the chief editor of Cibilized, I believe financial clarity should be simple and secure. That’s why I’ve created this guide. It provides the official, step-by-step method to check your CIBIL report for free, exactly as mandated by the Reserve Bank of India (RBI).

My goal is to give you the confidence to check your CIBIL report safely and understand its power. Let’s begin.

Why You Must Check Your CIBIL Report Before Lenders Do

Think of your CIBIL report as your financial report card. It’s a detailed history of your borrowing and repayment habits, and it’s the very first document banks and lenders will look at when you apply for credit. What you see on that report is exactly what they see; there are no secrets. This is why the decision to check your CIBIL report is the single most empowering first step you can take in any financial journey.

Waiting for a lender to review your report for you is like letting a professor grade an exam you’ve never studied for. By reviewing it beforehand, you get the opportunity to understand your standing, correct any mistakes, and approach lenders from a position of strength and confidence. Let’s explore the three critical advantages this gives you.

Unlock Better Loan & Card Offers

Your CIBIL score is the primary factor that determines your loan eligibility and the terms you will be offered. Lenders use this 3-digit number to quickly assess the risk of lending to you. A higher score signifies lower risk, which makes you a highly desirable customer.

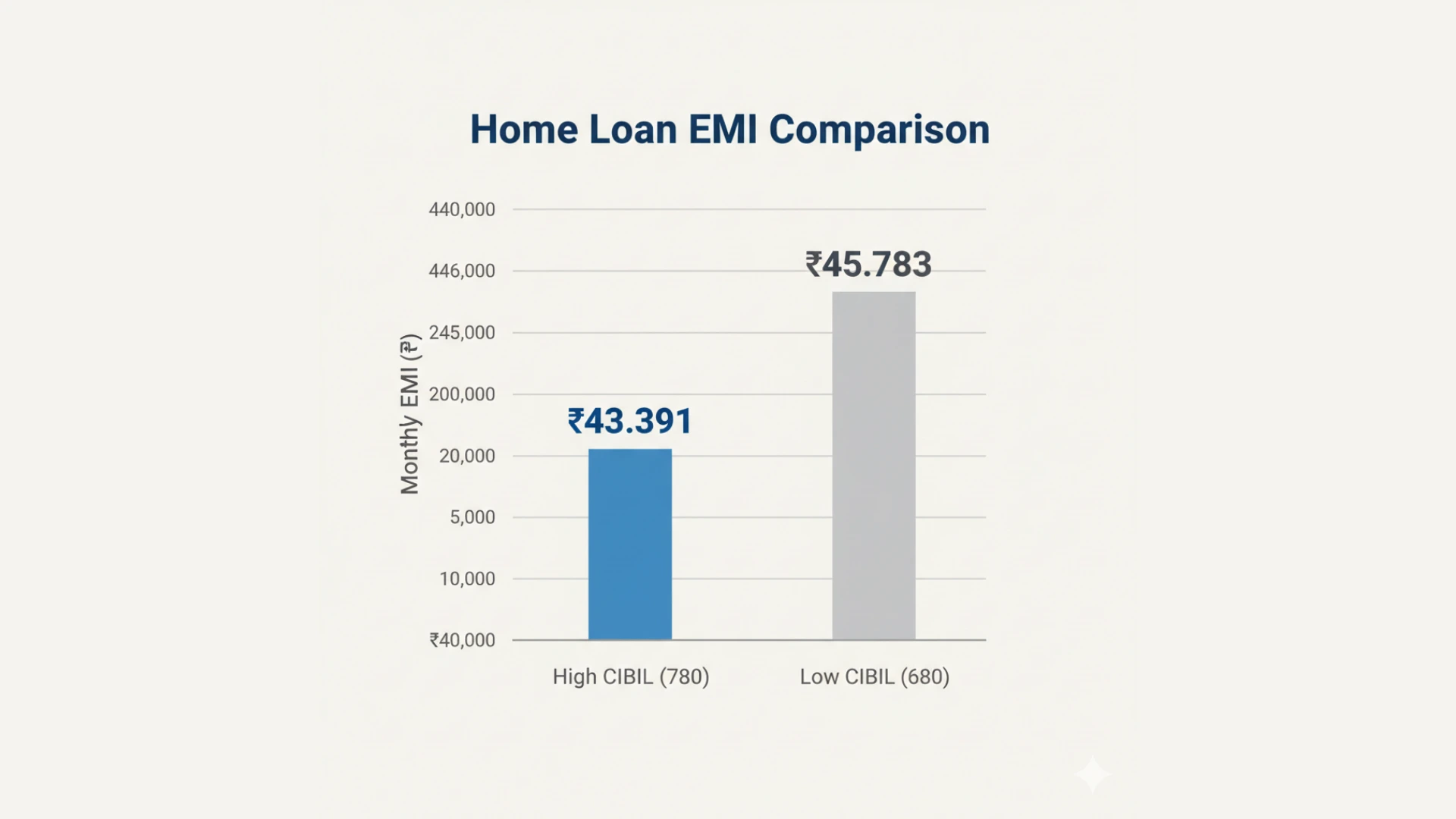

This directly translates into significant financial savings. Consider this real-world scenario for a ₹50 lakh home loan for a 20-year tenure in 2025:

- An applicant with a CIBIL score of 780 might be offered a preferential interest rate of 8.50% p.a. Their EMI would be approximately ₹43,391.

- An applicant with a score of 680 is seen as higher risk and might be offered a standard rate of 9.25% p.a. Their EMI would be approximately ₹45,783.

That small difference in score results in an extra payment of ₹2,392 every single month. Over the full 20-year loan period, the applicant with the lower score would pay over ₹5.7 lakhs more in total interest. This is why you must check your CIBIL report before you even start comparing loan options. When you know you have a strong score, you gain immense negotiating power and can confidently ask for the best possible terms.

Find and Fix Costly Errors

Your CIBIL report is compiled from data sent by various banks and financial institutions. With millions of data points being processed, mistakes can and do happen. You can’t afford to let someone else’s clerical error damage your financial future.

The only way to catch these issues is to proactively check your CIBIL report. Some of the most common—and damaging—errors include:

- Incorrect Ownership: An account or a late payment belonging to someone else with a similar name might be incorrectly mapped to your report.

- Outdated Account Status: A loan that you have fully paid off might still be showing as active or having an outstanding balance, which can negatively impact your score.

- Inaccurate Personal Details: Simple mistakes in your name, address, or PAN can lead to identity mismatches and delays in

credit approval. - Incorrect DPD Reporting: A payment made on time could be wrongly reported as delayed by 30 or 60 days, severely hurting your score.

These silent errors are precisely why you need to check your CIBIL report at least once a year, a right guaranteed to every Indian resident for free by the RBI. The only way to begin the correction process is to first identify the mistake, and that starts with getting your hands on the official document.

Guard Against Identity Theft

In today’s digital age, financial identity theft is a growing threat. A common tactic used by fraudsters is to use stolen personal information (like your PAN and Aadhaar details) to apply for loans or credit cards in your name. Often, the first sign of trouble appears on your credit report.

Making it a habit to check your CIBIL report is one of the simplest yet most effective ways to monitor your financial identity. Be on high alert if you spot any of these red flags:

- A Hard Inquiry You Don’t Recognize: This means a lender has pulled your report for a new credit application that you never made.

- A New Account You Didn’t Open: This is a clear sign that your identity has been compromised.

- A Sudden, Unexplained Drop in Your Score: This could indicate fraudulent activity on an existing account or a new one opened without your knowledge.

Treating your annual credit history check as a security routine is essential. It allows you to catch fraud at its earliest stage, report it to the bureaus and authorities, and protect your hard-earned financial reputation. Ultimately, the decision to check your CIBIL report is the difference between reacting to your financial situation and taking control of it.

The Official Step-by-Step Guide to Check Your CIBIL Report for Free

This section is your definitive guide to check your CIBIL report directly from the source, ensuring the information you receive is 100% authentic and secure. Under a mandate by the Reserve Bank of India (RBI), every Indian citizen is entitled to receive one full, free credit report from each of the four credit bureaus (including CIBIL) every calendar year.

Many third-party websites offer to provide your score, but the method outlined below is the official process to get your complete credit information report (CIR) from TransUnion CIBIL itself. Following these steps ensures your sensitive financial data remains protected.

Step 1: Navigate to the Official CIBIL Website

Your first and most important step is to ensure you are on the correct website. Scammers often create look-alike “phishing” sites to steal personal information.

The official CIBIL website for obtaining your free score and report is: https://www.cibil.com. Once on the homepage, you will typically see a prominent button or link with text like “Get Your Free CIBIL Score” or “Get Your Free Annual Credit Report.”

Anwar’s Note of Caution: Always double-check that the URL in your browser’s address bar starts with https://www.cibil.com/. Do not enter your personal information on any other site claiming to be the official CIBIL portal.

To begin the process to check your CIBIL report, click on this button to proceed to the account creation page.

Step 2: Creating Your Account and Entering Personal Details

To accurately locate your unique credit profile from millions of records, CIBIL requires you to provide key personal information. This step is crucial for identity verification.

You will be presented with a form asking for the following details. Have them ready to ensure a smooth process:

- Personal Information: Your full name and date of birth as they appear on your official documents.

- Identity Information: Your PAN (Permanent Account Number). This is the most critical piece of information as it is the primary identifier used by financial institutions.

- Contact Information: A valid email address (this will be your username for future logins) and your mobile number (for OTP verification).

- Address Information: Your current residential address and PIN code.

Providing these details accurately is the most important step to check your CIBIL report that truly belongs to you. This information is used solely to match you with your existing credit history and create a secure account for you to access it.

Step 3: Verifying Your Identity

Once you submit your details, CIBIL will initiate a two-part identity verification process to ensure that only you can access your sensitive financial data.

First, you will receive an OTP (One-Time Password) on the mobile number you provided. Enter this OTP on the website to complete the initial verification.

Second, and this is the step where many users get confused, you will be asked a series of authentication questions based on your credit history. These questions are designed so that only you would know the answers. They may look something like this:

- “Which bank issued your credit card ending in 8452?”

- “What is the sanctioned amount on your home loan with ICICI Bank?”

- “Do you have an active auto loan with HDFC Bank?”

Answer these questions carefully. If you have multiple loans or cards, it can be helpful to have recent statements nearby. This robust security step confirms your identity before you can check your CIBIL report, preventing any unauthorized access.

Step 4: Accessing Your Dashboard and CIBIL Report

Upon successful verification, you will be redirected to your personal CIBIL dashboard. The first thing you will see is your 3-digit CIBIL score displayed prominently. It will likely be color-coded to indicate your credit health (e.g., green for excellent, red for poor).

Congratulations on accessing your score! However, the score is just the headline. The real, actionable information lies within the full report. While you can now see your score, the task to check your CIBIL report isn’t complete until you have the full document. Your next crucial action is to view and download the detailed report.

Step 5: How to Download Your Full Credit Report PDF

The PDF version of your report is the document you will need for your own records and for use with analysis tools. From your CIBIL dashboard, follow these steps:

- Look for a tab or a button labeled “Credit Report” or “View Report”. Click on it.

- This will navigate you to a detailed, section-by-section view of your credit history, including your personal information, account details, and enquiry history.

- On this page, look for a “Download” or “Print” icon or button, usually located in the top-right corner.

- Clicking this will generate and download your full credit report as a password-protected PDF file. The password is typically your date of birth in DDMMYYYY format, but CIBIL will provide instructions on the screen.

This final action completes the process to check your CIBIL report. Having this PDF saved means you don’t have to go through the verification process every time you want to review your detailed credit history. You can now analyze the document you’ve successfully downloaded after you chose to check your CIBIL report and take the next steps toward improving your financial health.

Of course, Anwar. This section is critical for building trust and demonstrating true expertise. It bridges the gap between simply getting the report and actually understanding it.

Here is the detailed content, written in your voice and based on authoritative financial best practices in India, designed to be insightful, accurate, and within the specified length.

A Personal Note from Anwar Hashmi: What I Look for After a Download

After years of analyzing reports for myself and our readers at Cibilized, I’ve learned that the score is just a headline. The real story—the one that determines your financial future—is in the details of the report itself. The score tells you what, but the report tells you why.

Once you check your CIBIL report and have the PDF open, the sheer amount of information can be overwhelming. To cut through the noise, I personally scan for these three critical areas first. They are the most common sources of problems and the biggest opportunities for improvement.

1. The “Account Information” Section: Find the Hidden Killers

This section is the heart of your report. It lists every single loan and credit card you’ve ever had. While you should scan for accounts you don’t recognize, the most important columns to check are “Current Balance” and, crucially, “Account Status.”

I immediately look for two specific, highly damaging statuses:

- “Settled”: This means you had a dispute with a lender and paid only a partial amount of the total due to close the account. While it’s better than not paying at all, a “Settled” mark is a significant negative event. Lenders see it as a failure to meet your original obligation, and it can severely impact your

loan eligibilityfor up to seven years. It’s vital to check your CIBIL report for these specific statuses, especially on older accounts you may have forgotten about. - “Written-off”: This is even more serious. It means the lender has essentially given up on recovering the debt from you after a long period of non-payment (typically 180+ days) and has marked it as a loss in their books. An account that is “Written-off” is one of the biggest score killers. When I check my CIBIL report, this is the first status I scan for, as its presence almost guarantees a loan rejection from prime lenders.

2. The “Days Past Due (DPD)” Column: Your Payment Calendar

Your payment history makes up the largest portion of your CIBIL score. The DPD column shows a 36-month calendar of your payment discipline for each account. Understanding this is key.

You only want to see one thing here: “000” or “STD” (Standard). This indicates that your payment was made on time for that month.

Any other number is a red flag. For instance:

- “030” means you were late by 30 days.

- “060” means you were late by 60 days.

- “090” means you were 90 days overdue, which is when banks often report an account as a Non-Performing Asset (NPA).

Even a single late payment can drop your score, and the more recent it is, the more damage it does. This detailed history is why it’s so important to check your CIBIL report regularly. You can pinpoint the exact months where payments were missed and ensure that any payments you have since caught up on are being reported correctly by the lender.

3. The “Enquiry Information” Section: Who Is Looking at Your Data?

This section lists every time a financial institution has pulled your credit report. It’s crucial to understand the two types of inquiries:

- Soft Inquiry: This happens when you check your CIBIL report yourself or when a company does a pre-approval check without a formal application. Soft inquiries have zero impact on your CIBIL score.

- Hard Inquiry: This happens only when you formally apply for a new loan or credit card. Each hard inquiry can temporarily dip your score by a few points. Too many in a short period signals credit-hungry behavior to lenders.

The most important action here is to scan the list of hard inquiries and make sure you recognize every single one. If you see a hard inquiry from a lender you’ve never contacted, it’s a major red flag for an identity theft attempt. Pay close attention to this section every time you check your CIBIL report to ensure your data hasn’t been used for fraudulent applications.

Are Third-Party Websites Safe for a Free CIBIL Check?

In your search for financial information, you’ve likely seen numerous websites and apps offering a “free CIBIL score check” in just a few clicks. With so many options available to check your CIBIL report, it’s natural and wise to question their safety and legitimacy. Are they providing a genuine service, or is there a hidden cost?

The short answer is that while reputable third-party platforms are generally secure, they operate on a different business model than the official CIBIL bureau. Understanding this model is key to making an informed decision about where you share your sensitive financial data.

Most of these third-party websites are “financial marketplaces.” Their primary business is not just to show you your score, but to act as a bridge between you and potential lenders. They offer a free and convenient way to check your CIBIL report in exchange for your personal and financial information. This data is then used to match you with pre-approved loan and credit card offers from their partner banks and NBFCs. If you apply for a product through their platform, they earn a commission from the lender.

There is nothing inherently wrong with this model, but it’s a trade-off: you receive a free score in exchange for becoming a lead for financial products.

To help you decide what’s best for your needs, let’s directly compare the official CIBIL process with what typical third-party apps offer.

| Feature | Official CIBIL Website | Third-Party Apps |

| Report Type | Full, detailed official report | Often a summary or a score only |

| Data Privacy | Regulated by RBI; data is not sold | May share your data with partners |

| Cost | One truly free report per year | Free, but may lead to sales calls |

| Accuracy | The source of truth | Generally accurate score, but may lack detail |

Export to Sheets

Let’s look at what these differences mean for you.

- Report Type: When you get your report from the CIBIL website, you receive the complete, official Credit Information Report (CIR). This is a detailed, multi-page document showing your 36-month payment history for every account. Most third-party services provide just the 3-digit score and a summary, which is not sufficient for a deep analysis or for finding specific errors.

- Data Privacy: The purpose of the official CIBIL portal is to allow you to check your CIBIL report as per the RBI mandate. They are heavily regulated and do not sell your data to marketing partners. When you use a third-party app, you typically agree to terms and conditions that allow them to use your financial profile to market relevant products to you via calls, SMS, and emails.

- Cost: While both are “free,” the nature of the cost is different. The official report is a right, provided once per year at no cost, with no strings attached. The “cost” of using a third-party service is your consent to be marketed to.

- Accuracy: The score you see on reputable third-party platforms is generally accurate, as they pull it directly from the credit bureaus. However, the “source of truth” is the bureau itself. For the most critical tasks, like preparing a legal dispute, you need the official document that you get when you check your CIBIL report directly.

The Final Verdict

For quick, periodic monitoring of your score, reputable third-party apps can be a convenient tool.

However, for the most important and sensitive tasks—such as performing your first detailed credit history check, searching for errors to dispute, or preparing for a major application like a home loan—our strong recommendation is to always use the official CIBIL website first. This is the only way to get your complete, authentic report securely, without any obligation or concern that your data will be used for marketing purposes.

You’ve Managed to Check Your CIBIL Report – What’s Next?

Congratulations on taking the most important step towards mastering your credit health. Now that you have the official data from your decision to check your CIBIL report, it’s time to turn that information into action.

Your next move depends entirely on what you found in the report. Find your current situation below for a clear, step-by-step guide on what to do right now.

If your score is lower than you expected…

Did the number you saw cause some concern? Don’t worry. A low score is not a permanent label; it’s simply a starting point for improvement. After you check your CIBIL report and see a score below the ideal 750 mark, your next step is to build a clear, effective improvement plan.

These comprehensive guides provide proven strategies to help you systematically increase your score:

- For a general action plan: Unlock 750+: A Step by Step Plan on How to Improve Your CIBIL Score

- For a targeted recovery plan: How to Increase Your CIBIL Score From 600 to 750: A Proven Step by Step Guide

If you’ve found a mistake on your report…

Did you spot an account that isn’t yours, an incorrect late payment, or a loan that should be marked as closed? Don’t panic. The RBI mandates a clear process for correcting these errors, and doing so can provide a significant boost to your score.

Your next step is to file an official dispute with CIBIL. Our guide walks you through the entire process:

- For a step-by-step walkthrough: How to Dispute Errors on Your CIBIL Report: Best Step By Step Guide

If you’re planning to apply for a home loan…

If the reason you chose to check your CIBIL report was to prepare for a home loan application, understanding how lenders view your report is critical. Lenders have specific criteria, and knowing them beforehand can dramatically increase your chances of approval.

To ensure you are fully prepared, your next step is to understand the home loan process from a credit perspective.

- For an in-depth guide: The Ultimate Guide to CIBIL Score for Home Loans in India

Turn Your Report Into a Roadmap for Success

You’ve now learned the crucial reasons why you should monitor your credit and, most importantly, the official, secure process to get your report. The entire journey to better loans, lower interest rates, and financial security begins with the single, powerful decision you just learned to make: the decision to check your CIBIL report.

Now that you have your official report, don’t just stare at the data. The numbers and codes don’t have to be confusing. It’s time to translate that document into a clear, simple roadmap.

Use our free Credit Report Analysis Tool right here on this page to instantly get a personalized action plan. It will pinpoint your exact score killers and give you the clear, confident next steps you need to take to build a stronger financial future.

Frequently Asked Questions

1. Is the Cibil Report Analysis Tool safe and private?

Yes, 100%. The Cibil Report Analysis Tool is designed with a “Privacy First” guarantee. All processing happens directly within your browser. Your PDF file is never uploaded to our servers, and your personal data is never stored.

2. What is the difference between a hard and soft inquiry?

A soft inquiry happens when you check your own report or a company runs a pre-approval check. It does not affect your score. A hard inquiry happens when a lender checks your report after you apply for a loan or credit card. Too many hard inquiries in a short time can temporarily lower your CIBIL score.

3. Is it truly free to check your CIBIL report?

Yes. As per a mandate from the Reserve Bank of India (RBI), every individual is entitled to one full, free credit report from each of the four credit bureaus (including CIBIL) once per calendar year. This guide shows you the official process to get that free report.

4. What kind of PDF does the Cibil Report Analysis Tool accept?

Our Cibil Report Analysis Tool is designed to work with the official, password-protected PDF reports downloaded directly from the TransUnion CIBIL website. It is also compatible with reports from other major Indian bureaus like Experian.

5. How much does one late payment really affect my score?

A single late payment can have a significant negative impact, potentially dropping your score by 30 to 80 points. The severity depends on how late the payment was (30, 60, or 90+ days) and how recent it was. A recent late payment is more damaging than an old one.

6. How often should I check my CIBIL report?

It’s a best practice to check your CIBIL report at least once a year. Additionally, you should always check it 3-6 months before you plan to apply for a major loan, like a home loan or car loan, to give yourself time to correct any errors.

7. Why is this Cibil Report Analysis Tool different from others?

Most “free score” websites require you to create an account and store your data on their servers, often using it for marketing. Our Cibil Report Analysis Tool is unique because it works entirely on your device, offering a truly private and secure analysis without requiring you to share your data with us.

8. Why is a ‘Settled’ account considered negative on my credit report?

A “Settled” account means you paid back less than the full amount you owed the lender. While it’s better than not paying at all, lenders view it as a failure to meet your original agreement. It acts as a serious negative mark on your report for up to seven years.

9. What documents or information do I need to check my CIBIL report?

To verify your identity, you will need your PAN card number, date of birth, an email address, and a mobile number for OTP verification. The official CIBIL portal will then ask you a few questions based on your existing credit accounts to confirm your identity.

10. Can I use the Cibil Report Analysis Tool for my Experian or CRIF report?

Yes. While optimized for the CIBIL format, the intelligence built into the Cibil Report Analysis Tool can accurately parse and analyze official reports from other major Indian credit bureaus like Experian, Equifax, and CRIF High Mark.

11. What is credit utilization and why does it matter?

Credit utilization is the percentage of your available credit card limit that you are currently using. For example, if your limit is ₹1,00,000 and your balance is ₹50,000, your utilization is 50%. High utilization (generally above 30%) is a major red flag for lenders, as it suggests you might be over-reliant on credit.

12. Will I lower my score if I check my CIBIL report myself?

No. When you check your CIBIL report yourself, it is considered a “soft inquiry.” Soft inquiries are only visible to you and have zero impact on your credit score. “Hard inquiries,” which can temporarily lower your score, only happen when a lender pulls your report after you formally apply for credit.

13. I have my results from the Cibil Report Analysis Tool. What is the most important first step?

The most crucial first step is to address any high-impact “Score Killers” the tool identified. If it flagged an error, your priority is to file a dispute. If it flagged high credit card balances, your priority is to create a repayment plan. The tool’s purpose is to turn data into a clear, prioritized action plan.

14. What’s the difference between checking my score and getting my full report?

Your CIBIL score is just a 3-digit number summarizing your credit health. The action to check your CIBIL report provides you with the complete, multi-page document that shows the detailed data behind that score, including your account-by-account payment history for the last 36 months.

15. What is a realistic CIBIL score for getting a home loan approved?

While policies vary, most major banks in India consider a CIBIL score of 750 or above to be excellent for a home loan application. A score above 750 significantly increases your chances of approval and helps you qualify for the lowest possible interest rates.