Unmask the common credit card hidden charges in India with our expert guide. Learn how to spot and avoid every credit card hidden charges in India and save money.

Introduction: The “Bill Shock” Moment

The Story of the Unexpected Charge

You check your credit card bill online, expecting a certain amount, but the total is significantly higher than you calculated. Tucked away in the fine print is a charge you don’t recognize: a “Finance Charge,” a “Late Fee,” or a mysterious “GST” component. It’s a frustrating moment that can make you feel powerless against the confusing world of credit card hidden charges in India.

This experience is incredibly common. Banks often rely on complex fee structures that can be difficult to understand, leading to what I call “bill shock.” You feel like you’ve been penalized, but you’re not even sure what rule you broke.

What This Guide Will Do For You

My name is Anwar Hashmi, and at cibilized.in, my mission is to give you back that power. This guide is your shield against unfair fees. It will unmask every common credit card hidden charges in India and explain it in simple, clear language.

We will go beyond just listing the fees. By the end of this guide, you will have a clear, step-by-step framework to audit your bill like a pro and proven strategies to avoid these costly charges forever.

Understanding these credit card hidden charges in India is the first step to true financial control. Learning how to spot a potential credit card hidden charges in India is a skill that will save you thousands.

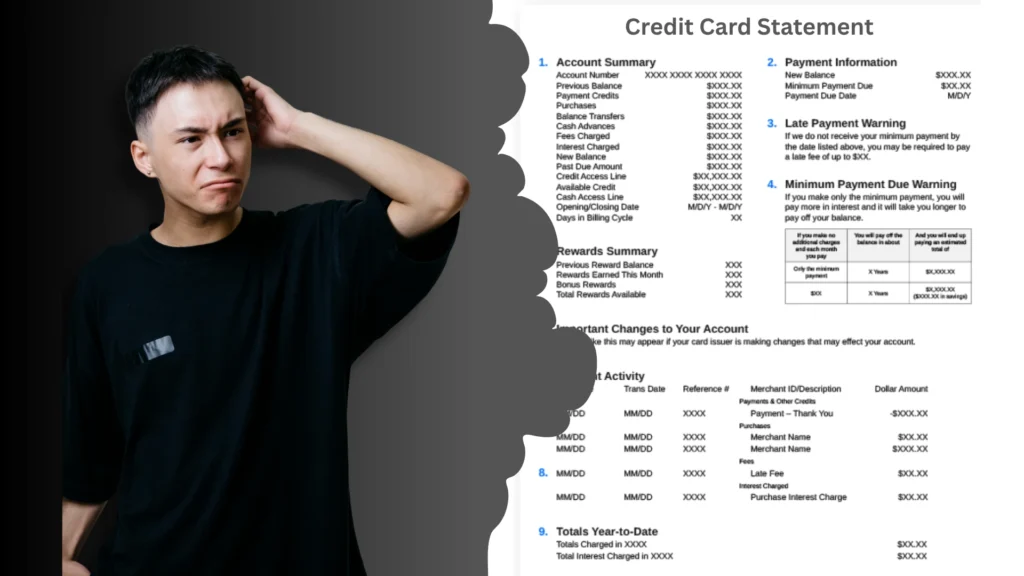

The Anatomy of a Credit Card Bill: Where to Find the Traps

To protect yourself from unexpected fees, you must first learn to read your credit card bill like an expert. Banks often design these statements to be confusing, highlighting the large, friendly “Total Amount Due” while burying the most important details in the fine print.

This is where the traps are hidden. In my experience as a financial writer, the vast majority of people who are hit with a credit card hidden charges in India simply didn’t know where to look. This section is your guide to becoming a financial detective. We will dissect the anatomy of a typical bill and show you exactly where to focus your attention to spot every potential fee.

The “Minimum Amount Due” Trap

Before we even get to the fine print, we must address the most dangerous trap on your entire statement: the “Minimum Amount Due.” This small number, usually just 5% of your total balance, feels like a helpful option from the bank. It is not. It is the single most effective tool the bank has to keep you in a cycle of high-interest debt.

How the Trap Works: The Power of Compounding Interest

When you pay only the minimum, you are not charged a “late fee,” so your CIBIL payment history remains clean. However, the bank immediately begins charging a very high interest rate (often 3-4% per month, which is over 40% per year) on your remaining balance. This interest then gets added to your principal, and the next month, you are charged interest on the interest.

Let’s look at a simple, real-world example:

- Your Outstanding Bill: ₹50,000

- Minimum Payment: ₹2,500

- You Pay: Only the minimum.

You might think you’ve cleared most of your obligation, but the remaining ₹47,500 is now subject to a massive interest rate. It could take you years to clear that single month’s bill, and you could end up paying more in interest than the original amount you spent. This isn’t technically a credit card hidden charges in India, but it is the most costly trap of all.

Reading the Fine Print: Your Bill’s Most Important Section

Now, let’s find the real hidden fees. Every month, you must dedicate just five minutes to auditing the “Summary of Charges” or “Transaction Details” section of your bill. This is your first line of defense.

Where to Look

On your statement PDF or your net banking portal, look for a detailed table that breaks down your total bill. It will have line items for your purchases, and then separate line items for all fees and taxes. This is where you will find any credit card hidden charges in India.

Your Monthly Audit Checklist

When you review this section, you are looking for specific line items that are not your purchases. Keep an eye out for:

- Annual Fees: Is this a fee you were aware of?

- Late Payment Charges: Was your payment actually late?

- Finance Charges (Interest): Is this being calculated correctly?

- Cash Advance Fees: Did you withdraw cash from an ATM?

- Over-Limit Charges: Did your spending exceed your credit limit?

- GST: Is GST being correctly applied only to the fee and interest components, not your whole bill?

By diligently checking this section every single month, you will never be surprised by a credit card hidden charges in India again. This proactive audit is the most important habit you can build. It’s the core of any strategy to avoid a credit card hidden charges in India and take control of your finances. This simple check is how you beat the system and ensure every credit card hidden charges in India is identified and questioned.

Of course. Let’s build the crucial third section of your new cluster article, “The Ultimate Guide to Unmasking and Avoiding Hidden Credit Card Charges in India.”

Unmasked: A Deep Dive into the 5 Most Common Hidden Charges

Now that you know where to look on your bill, it’s time to unmask the culprits. In my years of analyzing credit card statements, I’ve seen that the same handful of fees are responsible for the vast majority of “bill shock” moments. These are the charges that banks often don’t advertise but are detailed in the fine print of your cardholder agreement.

This section is your field guide. We will do a deep dive into the five most common fees, explaining exactly what they are, how they are calculated, and, most importantly, the expert-level strategies you can use to avoid them. By understanding these, you will master the art of spotting and preventing every common credit card hidden charges in India.

Trap #1: The Annual Maintenance Fee (AMF)

The Annual Maintenance Fee (or simply Annual Fee) is a yearly charge that banks levy for the benefits and privileges associated with your credit card. It is one of the most common types of credit card hidden charges in India that surprises new users.

What it is and how it’s charged

This fee is not tied to your spending. It is a fixed charge, ranging from ₹250 for a basic card to over ₹50,000 for a super-premium one, that is automatically added to your bill once every year, usually in the same month you first received the card. Banks justify this fee as the cost of providing services like reward points, lounge access, insurance, and concierge services.

The Pro-Level Strategy: How to Get Your Annual Fee Waived

Here is a secret that banks don’t widely advertise: for many cards, the annual fee is negotiable, especially if you are a good customer. Banks would rather waive a ₹1,000 fee than lose a customer who spends lakhs on their card each year.

If you see an annual fee on your bill, you can call the bank’s customer care and politely request a waiver. Here is a sample script you can adapt:

“Hello, my name is [Your Name], and I’m calling about the annual fee of [Amount] that was just charged to my credit card ending in [Last 4 Digits]. I’ve been a loyal customer with your bank for [Number] years and have always paid my bills on time. I would like to request a goodwill waiver of this annual fee. If a waiver is not possible, I may have to consider closing this account and switching to a lifetime-free card from another bank.”

This script is effective because it is polite, highlights your value as a customer, and shows that you are prepared to take your business elsewhere.

Trap #2: The Late Payment Fee

This is perhaps the most painful credit card hidden charges in India because it feels like a penalty for a small mistake. A late payment fee is charged if you fail to pay at least the Minimum Amount Due by the specified Due Date.

How it’s calculated

Late payment fees are not a flat amount. According to RBI guidelines, these fees are typically charged on a tiered basis, based on your total outstanding balance. A typical structure might look like this:

| Total Outstanding Balance | Late Payment Fee |

| Less than ₹500 | ₹0 |

| ₹501 to ₹1,000 | ₹100 |

| ₹1,001 to ₹10,000 | ₹500 |

| More than ₹10,000 | up to ₹1,300 |

This means a single day’s delay on a large bill can cost you over a thousand rupees, in addition to the negative impact on your CIBIL score.

The “Goodwill Reversal”: How to get a one-time late fee reversed

If you have a long and excellent history with your bank and have made a single, genuine mistake, you can often get this fee reversed. Call customer care, be polite, and explain the situation.

Here is a sample script:

“Hello, I’m calling about a late payment fee on my recent statement. As you can see from my [Number]-year history with your bank, I have never missed a payment before. The delay this month was due to [a genuine reason, e.g., a medical emergency/technical issue]. As a long-time, loyal customer, I would like to request a one-time goodwill reversal of this charge.”

Banks will often grant this request for their best customers to maintain a good relationship. This is a powerful tactic for dealing with an unexpected credit card hidden charges in India.

Trap #3: The Cash Advance Fee & High Interest Rate

This is, without a doubt, the single most expensive transaction you can ever make with your credit card. Using your credit card to withdraw cash from an ATM is treated completely differently from a normal purchase, and it comes with two devastating charges. This is a credit card hidden charges in India that can lead to a massive debt spiral.

- The Immediate Cash Advance Fee: The moment you withdraw the cash, the bank charges you a transaction fee. This is typically 2.5% of the withdrawn amount, with a minimum of ₹300-₹500. So, withdrawing ₹10,000 will instantly cost you ₹250 plus GST.

- Immediate, High-Interest APR: Unlike regular purchases, cash withdrawals have no interest-free period. The bank starts charging you a very high interest rate (often 3-4.5% per month, which is up to 54% per year) from the very second you take the cash.

This combination makes cash withdrawal a financial emergency option only.

Trap #4: The Over-Limit Fee

An over-limit fee is a penalty charged by the bank if your outstanding balance exceeds your assigned credit limit.

What most people don’t know is that, thanks to RBI guidelines, banks cannot automatically allow you to spend over your limit and then charge you a fee. They must first get your explicit consent (usually via an opt-in at the time of application) to enable over-limit spending.

If you have not opted-in and the bank allows an over-limit transaction and then charges you a fee, this is an unauthorized credit card hidden charges in India, and you have the right to dispute it. Always check your card’s terms to see if you have opted in for this facility.

Trap #5: Hidden Forex Markup Fees

This is the most common credit card hidden charges in India for people who travel or shop on international websites. The Forex (Foreign Exchange) Markup Fee is a charge levied by your bank for converting a foreign currency transaction into Indian Rupees.

This fee is typically a percentage of the transaction amount, usually ranging from 1.99% to 3.5%, plus GST. It is not explicitly listed as a separate fee on your bill; it is bundled into the final INR amount of the transaction, making it very difficult to spot.

For example, if you make a $100 purchase on a US website when the exchange rate is ₹83 per dollar, you would expect the charge to be ₹8,300. However, with a 3.5% markup fee, the bank will actually charge you around ₹8,590. That extra ₹290 is the hidden fee. Understanding this is key to avoiding a common credit card hidden charges in India.

The Interest Rate Trap: How “Finance Charges” Really Work

Of all the fees we’ve discussed, the one that causes the most financial damage is the “Finance Charge,” more commonly known as interest. This isn’t just a simple fee; it’s a complex system designed to be confusing. In my experience, understanding this system is the key to protecting yourself from the single most costly credit card hidden charges in India.

Many people I’ve spoken with feel that the way interest is calculated is deliberately opaque. This section will pull back the curtain. We will unmask the two biggest interest-related traps: the illusion of the “monthly” rate and the painful secret of “residual” interest.

APR vs. Monthly Rate: The Bank’s Favorite Illusion

When you look at your credit card’s fine print, you will often see the interest rate advertised as a “small” monthly number, like 3.5%. This is a deliberate marketing choice designed to make the rate seem less intimidating. However, to understand the true cost, you must look at the Annual Percentage Rate (APR).

The APR is the real, yearly cost of your debt. To calculate it, you simply multiply the monthly rate by 12.

- The Illusion: A “small” 3.5% monthly rate.

- The Reality: A massive 42% Annual Percentage Rate (APR).

This massive annual rate is what generates the painful finance charges that can feel like a devastating credit card hidden charges in India. If you carry a balance of ₹1,00,000 for a year at this rate, you will pay ₹42,000 in interest alone. This illusion is a common source of unexpected credit card hidden charges in India.

The Residual Interest Rule: The Sneakiest Credit Card Hidden Charges in India

This is, without a doubt, the most confusing and frustrating trap for even the most responsible credit card users. It’s the reason you can still be charged interest even after you’ve paid what you thought was your full bill. It’s what I call “ghost” interest.

How It Works: The Daily Compounding Trap

Here is the secret banks don’t advertise: interest on your credit card balance is calculated daily, not monthly. When you don’t pay your entire bill by the due date, you lose your interest-free grace period. From that point on, interest starts accruing on your remaining balance every single day.

Let’s use a clear, real-world example:

- Your statement is generated on January 15th with a total bill of ₹20,000. Your due date is February 5th.

- On the due date, you make a large payment of ₹19,500, leaving a small remaining balance of just ₹500. You feel responsible.

- However, because you did not pay the full ₹20,000, the bank now goes back and calculates interest on your average daily balance for the entire billing period.

- Furthermore, interest now starts accruing on your new purchases from the day you make them, with no grace period.

- When your next bill arrives on February 15th, you are shocked to see not just your new purchases, but an extra “Finance Charge.”

This “ghost” interest is a true credit card hidden charges in India because it’s not explicitly shown on your bill until it’s too late. This small remaining balance is why people are shocked by this credit card hidden charges in India the following month.

The Only Solution: The “Pay in Full” Rule

The only way to escape the residual interest trap… is to follow one simple, non-negotiable rule: pay your ‘Total Amount Due’ in full before the due date. An even more powerful, expert-level strategy to ensure you never pay interest and also boost your CIBIL score is to pay your credit card bill before the statement date.

When you pay in full, you maintain your interest-free grace period, and the bank cannot charge you a single rupee of interest on your purchases. Avoiding this specific credit card hidden charges in India requires paying your bill in full every single time. It is the most powerful financial habit you can build.

Your “Bill Audit” Checklist: How to Scan Your Statement in 5 Minutes

Knowledge is the first step, but action is what creates real change. You now understand the most common traps hidden within your credit card statement. The next step is to build a simple, powerful habit that will protect you from these fees forever: the 5-Minute Bill Audit.

In my years as a financial writer, I’ve found that the best way to stay in control of your finances is to create simple, repeatable systems. This is my personal checklist. I follow it every single month, and it’s the single most effective way to ensure you never pay a rupee more than you have to. This audit is your best defense against any potential credit card hidden charges in India.

Your Monthly 5-Minute Action Plan

Once a month, when your credit card bill arrives, take just five minutes—before you even think about paying it—to go through this checklist.

[ ] 1. Verify the Annual Fee

- What to Look For: Scan the “Fees and Charges” section for a line item labeled “Annual Fee” or “Renewal Fee.” This is usually charged in the same month your card was first issued.

- Your Action: Ask yourself: “Was I aware of this fee? Do the benefits I get from this card justify this cost?” If not, this is your trigger to call the bank and use the script from our previous section to request a waiver.

[ ] 2. Scrutinize for Late Payment Fees

- What to Look For: Look for a charge labeled “Late Payment Fee.”

- Your Action: Cross-reference this with your bank records. Did you actually miss the due date? If it’s an error, you must dispute it immediately. If it was a genuine mistake and you have a good history, this is your trigger to call the bank and request a one-time goodwill reversal. Ignoring this is how a credit card hidden charges in India can damage both your wallet and your CIBIL score.

[ ] 3. Hunt for Cash Advance Fees

- What to Look For: Check for any “Cash Advance Fee” and the immediate, high “Finance Charges” that accompany it.

- Your Action: Did you withdraw cash from an ATM using your card this month? If you did not, this is a major red flag for a fraudulent transaction and you must contact the bank immediately. This is a particularly dangerous credit card hidden charges in India due to the high interest.

[ ] 4. Check for Over-Limit Charges

- What to Look For: A fee labeled “Over-Limit Charge” or “Over-Limit Penalty.”

- Your Action: First, check if your spending actually exceeded your credit limit. Second, and more importantly, confirm if you ever gave the bank explicit consent to allow over-limit spending. If you did not, this is an unauthorized credit card hidden charges in India that you can and should dispute with the bank.

[ ] 5. Confirm the GST Calculation

- What to Look For: A line item for “GST” (Goods and Services Tax).

- Your Action: This is a crucial check. Remember, GST should only be calculated on the fee and interest components of your bill, not on your total transaction amount. If you have a ₹500 late fee and a ₹1,000 interest charge, the 18% GST should only be applied to that ₹1,500. Verifying the GST is a key step in spotting an incorrect credit card hidden charges in India.

By making this 5-minute audit a non-negotiable monthly habit, you transform from a passive consumer into a vigilant financial manager. This simple checklist is your most powerful tool to identify and challenge every potential credit card hidden charges in India and keep your hard-earned money where it belongs—with you.

Frequently Asked Questions About Credit Card Hidden Charges In India:

1. How is the late payment fee calculated on a credit card?

A late payment fee is typically calculated on a tiered basis depending on your total outstanding balance, often ranging from ₹100 to ₹1,300. To avoid this costly late payment fee, always pay at least the minimum amount due before the deadline.

2. What is the most common credit card hidden charges in India that surprises new users?

The most common credit card hidden charges in India is often the Annual Maintenance Fee (AMF), as it’s a yearly cost not tied to spending. To avoid this unexpected credit card hidden charges in India, always check if your card is “Lifetime Free” before applying.

3. What are finance charges on a credit card bill?

Finance charges are the interest you are charged when you don’t pay your entire bill in full by the due date. These finance charges are calculated on a daily basis at a very high Annual Percentage Rate (APR), often exceeding 40%.

4. Why is the interest rate on a cash advance fee so high?

The interest rate on a cash advance fee is high because the bank views withdrawing cash from a credit card as a sign of high financial risk. This high interest, combined with the initial cash advance fee, makes it the single most expensive transaction you can make.

5. How can I get a credit card hidden charges in India reversed?

For fees like a one-time late payment, you can often get a credit card hidden charges in India reversed by calling customer care and requesting a “goodwill reversal.” Proactively managing your account is the best way to prevent a credit card hidden charges in India from appearing in the first place.

6. Can I really get my annual maintenance fee waived by the bank?

Yes, if you are a good customer with a strong payment history, banks will often waive the annual maintenance fee upon request. Don’t be afraid to call and ask for your annual maintenance fee to be reversed; the worst they can say is no.

7. Does the bank need my permission to charge an over-limit fee?

Yes, according to RBI guidelines, a bank cannot charge an over-limit fee unless you have explicitly opted-in for the over-limit facility. An unexpected over-limit fee can often be disputed if you did not give prior consent.

8. Is the Forex Markup a significant credit card hidden charges in India?

Yes, the Forex Markup is a major credit card hidden charges in India for international transactions, often adding 2-3.5% to your bill. This credit card hidden charges in India is hard to spot as it’s bundled into the final transaction amount.

9. How is GST on a credit card calculated?

The GST on a credit card is calculated at 18% on all fee and interest components, not on your purchase transactions. Understanding how GST on a credit card is applied can help you spot billing errors.

10. What should I do if I find a credit card hidden charges in India on my bill?

If you find a credit card hidden charges in India, your first step is to call your bank’s customer service immediately to dispute it. To protect yourself from a future credit card hidden charges in India, make a habit of auditing your statement every month as outlined in our checklist.

11. What is a goodwill reversal and when can I ask for one?

A goodwill reversal is when a bank agrees to reverse a charge, like a late fee, for a loyal customer as a gesture of goodwill. You can ask for a goodwill reversal if you have a long history of on-time payments and have made a single, genuine mistake.

12. Does the forex markup fee apply to online international purchases?

Yes, the forex markup fee applies to all transactions made in a foreign currency, including online shopping from international websites. This forex markup fee is often a surprise for many users who don’t read the fine print.

13. How does paying only the minimum amount due trap me in debt?

Paying only the minimum amount due is a trap because the remaining balance is charged a very high interest rate that compounds daily. It can take years and cost you thousands in interest to clear your debt if you only pay the minimum amount due each month.

14. Why is the Cash Advance Fee considered the worst credit card hidden charges in India?

The Cash Advance Fee is the worst credit card hidden charges in India because it triggers two penalties: an immediate transaction fee and an extremely high interest rate that starts from day one with no grace period. This combination makes it the most costly credit card hidden charges in India.

15. Can I dispute an incorrect finance charge on my bill?

Yes, if you believe a finance charge has been calculated incorrectly (for example, you were charged interest even after paying in full), you have the right to dispute it with your bank. Understanding how finance charges are calculated is the first step to identifying an error.

16. What is the best way to manage my credit card bill to avoid fees?

The single best way to manage your credit card bill is to pay the “Total Amount Due” in full before the due date. This simple habit ensures you never pay interest or late fees and is the foundation of a healthy credit card bill management strategy.

From Victim to Vigilant Consumer: The Final Verdict

That feeling of “bill shock”—of seeing an unexpected charge and feeling powerless—is exactly what credit card companies often rely on. However, as this guide has shown, you are never powerless. The real power is in your hands, and it comes from knowledge.

The most important takeaway is this: the best defense against a credit card hidden charges in India is a vigilant offense. By understanding the traps, from the illusion of the “minimum amount due” to the intricacies of residual interest, you transform from a potential victim into a savvy, empowered consumer. You now have the checklist and the strategies to audit your bill like a pro and challenge any fee that is unfair or incorrect.

Avoiding these costly fees is a critical part of smart credit management. This proactive financial control is a key component of the overall strategy for how to improve your CIBIL score, which provides a complete framework for building an excellent credit profile.

Author’s Note

A Note from the Author: I wrote this guide because the world of credit card fees is designed to be confusing. My mission is to give you the clarity to fight back against every unfair credit card hidden charges in India.

- Anwar Hashmi, founder of

cibilized.in. For expertise on American finance, he is also the lead author atClaimCredits.online, specializing in USA Tax Credits.

Pingback: How to Read Your Credit Card Statement: The Best Step By Step Guide for 25-26 - CIBILized

Pingback: Does No Cost EMI on Flipkart Damage CIBIL Score in 25-26? The Truth - CIBILized