Getting a home loan with a low CIBIL score isn’t about luck; it’s about following a proven, step-by-step plan to turn rejection into approval.

Getting a home loan with a low CIBIL score isn’t about finding a lenient bank. It’s about following a proven plan to become the borrower a bank trusts.

— Anwar Hashmi, Chief Editor, cibilized.in

Authored By: Anwar Hashmi | Last Updated: September 18, 2025

The dream of owning a home is a cornerstone of financial security for many Indians. But that dream can quickly turn into a nightmare when you see your CIBIL score. The question, “Can I even get a home loan with a low CIBIL score?” is one of the most stressful questions an aspiring homeowner can ask.

You might feel stuck, frustrated, or even too afraid to apply. Perhaps you’ve already faced the heartbreak of a rejection letter. It’s a deeply personal and discouraging experience. But I want to tell you right now: this is a temporary setback, not a permanent failure.

This guide is not just another article filled with vague advice. It is a practical, user-centric roadmap. We have developed a proven, 6-month action plan designed for anyone who has been rejected or is struggling to get a home loan with a low CIBIL score. Following this plan will empower you to take control, rebuild your creditworthiness, and re-approach lenders with confidence.

The Reality Check: What is the Actual Minimum CIBIL Score for a Home Loan?

Before you can fix the problem, you need to understand the landscape. Many applicants believe there’s a single magic number that guarantees a home loan, but the reality is more nuanced. Lenders operate in ranges, and understanding these ranges is the first step toward your goal, even if you are starting with a home loan with a low CIBIL score in mind.

There is no official “minimum” score set by the RBI, but based on lending patterns from major Indian banks like SBI, HDFC, and ICICI, we can establish clear benchmarks. For banks, offering a home loan with a low CIBIL score is a significant financial risk, which is why they scrutinize applications in the lower ranges much more carefully.

CIBIL Score Ranges and Their Meaning for Lenders

| CIBIL Score Range | Lender’s Perception | Likelihood of Home Loan Approval |

| 750 and above | Excellent / Low Risk | Very High, with best interest rates. |

| 700 – 749 | Good / Acceptable Risk | High, with competitive interest rates. |

| 650 – 699 | Fair / Moderate Risk | Possible, but may come with higher interest rates or require a higher down payment. |

| Below 650 | Poor / High Risk | Very Low. Most major lenders will reject the application outright. |

If your score is below 700, don’t lose hope. It simply means you need a clear strategy. The challenge of securing a home loan with a low CIBIL score is significant, but it’s a challenge that can be overcome with a disciplined approach.

Why Lenders Reject a Home Loan with a Low CIBIL Score (The Top 5 Reasons)

When a lender rejects an application, the low CIBIL score is often just the headline. The real reasons for rejection of a home loan are found in the details of your credit report. Understanding these specific issues is critical to fixing them.

A lender sees each of these issues as a sign of financial instability, which makes them hesitant to approve a large, long-term loan. Each of these factors is a major roadblock for anyone trying to get a home loan with a low CIBIL score.

Here are the top five reasons your application might be denied:

- 1. High Credit Utilization Ratio (CUR): If you are consistently using more than 30-40% of your available credit card limit, lenders see you as credit-hungry and potentially overleveraged.

- 2. Multiple Recent Hard Inquiries: Applying for many loans in a short period signals desperation. If you believe some of these are errors, you should learn how to remove hard inquiry from CIBIL report to clean up your history.

- 3. Errors or Inaccuracies on Your Report: A mistake you didn’t even make, like an incorrectly reported late payment or a closed account still showing as active, can unfairly drag your score down.

- 4. Poor Credit Mix: If your credit history only consists of unsecured loans (like personal loans or credit cards) and no secured loans (like a car loan), lenders may see your profile as less stable.

- 5. History of Late Payments or Settlements: This is the most damaging factor. Understanding the critical difference between a loan settlement vs loan closure credit report is key, as “settled” accounts are major red flags.

Loan Rejected? Your Critical First 48 Hours

Receiving a rejection notification can trigger panic. Your first instinct might be to immediately apply with a different bank, hoping for a different outcome. This is the single biggest mistake you can make.

A panicked reaction is the worst thing you can do when your goal is to eventually get a home loan with a low CIBIL score. You need to pause and strategize, not react.

The #1 Mistake to Avoid

Do not, under any circumstances, rush to another lender and fill out a new application. Every new application results in a hard inquiry on your CIBIL report, which can lower your score even further. This makes your situation worse, not better.

Your 3-Step Immediate Action Plan

- Pause & Breathe: Take a day or two. Do not make any financial decisions. The path to a home loan with a low CIBIL score starts with calm, calculated moves.

- Ask “Why?”: Formally contact the lender that rejected your application. You have the right to know the specific reason for the rejection. Get it in writing if possible.

- Download Your Full CIBIL Report: Immediately get a fresh copy of your detailed report from the official CIBIL website. You need to see exactly what the lender saw.

The 6-Month Action Plan for a Home Loan with a Low CIBIL Score

This is the core of our guide. This structured recovery mission is your path to success, following the proven principles of how to increase your CIBIL score from 600 to 750. Follow these steps diligently for six months, and you will transform your credit profile from high-risk to highly eligible.

Phase 1: Month 1-2 (The Clean-Up Phase)

This initial phase is about damage control and fixing the foundation. This is the most crucial part of turning your situation around and is non-negotiable for anyone serious about getting a home loan with a low CIBIL score.

- Action 1 – Dispute Every Error: The first and most powerful action is to correct any mistakes on your report. Our detailed guide explains exactly how to dispute errors on your CIBIL report step-by-step.

- Action 2 – Attack High Balances: Your goal is to get your Credit Utilization Ratio (CUR) below 30% on all credit cards. Pay down your balances as aggressively as you can.

- Action 3 – Stop All New Applications: Do not apply for any new credit cards or loans during this period. Your profile needs to stabilize.

Phase 2: Month 3-4 (The Build Phase)

With the clean-up done, this phase is about building a track record of positive credit behavior. This consistency is how you prove to lenders that you are a responsible borrower.

- Action 1 – Perfect Your Payment History: This is non-negotiable. Pay every single bill—credit cards, existing EMIs, utilities—on time, without fail. Set up auto-debit if necessary.

- Action 2 – Monitor Your Progress: Check your CIBIL score once a month (this is a soft inquiry and won’t hurt your score) to see the positive impact of your efforts.

- Action 3 (Optional) – Improve Your Credit Mix: If your report lacks a credit card, consider getting a secured credit card against a fixed deposit. This is a low-risk way to build a positive payment history and is a smart move on the path to a home loan with a low CIBIL score.

Phase 3: Month 5-6 (The Strategy Phase)

You have now done the hard work. This final phase is about preparing for a successful reapplication. You are no longer just applying; you are now strategically positioning yourself to successfully get a home loan with a low CIBIL score.

- Action 1 – Verify Your New Score: Your score should have seen a significant improvement. Ideally, you should aim to cross the 700-720 mark to be considered a viable candidate.

- Action 2 – Prepare Flawless Documentation: Gather all your necessary documents—payslips, bank statements, ITRs, property documents—and ensure they are perfect.

- Action 3 – Choose the Right Lender: Don’t just go back to the biggest banks. Research NBFCs, which are regulated by the National Housing Bank, or smaller banks that may have more flexible criteria for a home loan with a low CIBIL score.

How to Reapply After Rejection and Get Approved

Reapplying for a home loan after a rejection is not about hoping for a different outcome; it’s about demonstrating growth and responsibility. Your new application should tell a story of how you’ve improved your credit health.

You can even approach the same lender that rejected you initially. This can be a powerful move, as it directly shows them you took their feedback seriously and made concrete changes. This approach shows lenders you’re a safe bet now, even if you previously applied for a home loan with a low CIBIL score.

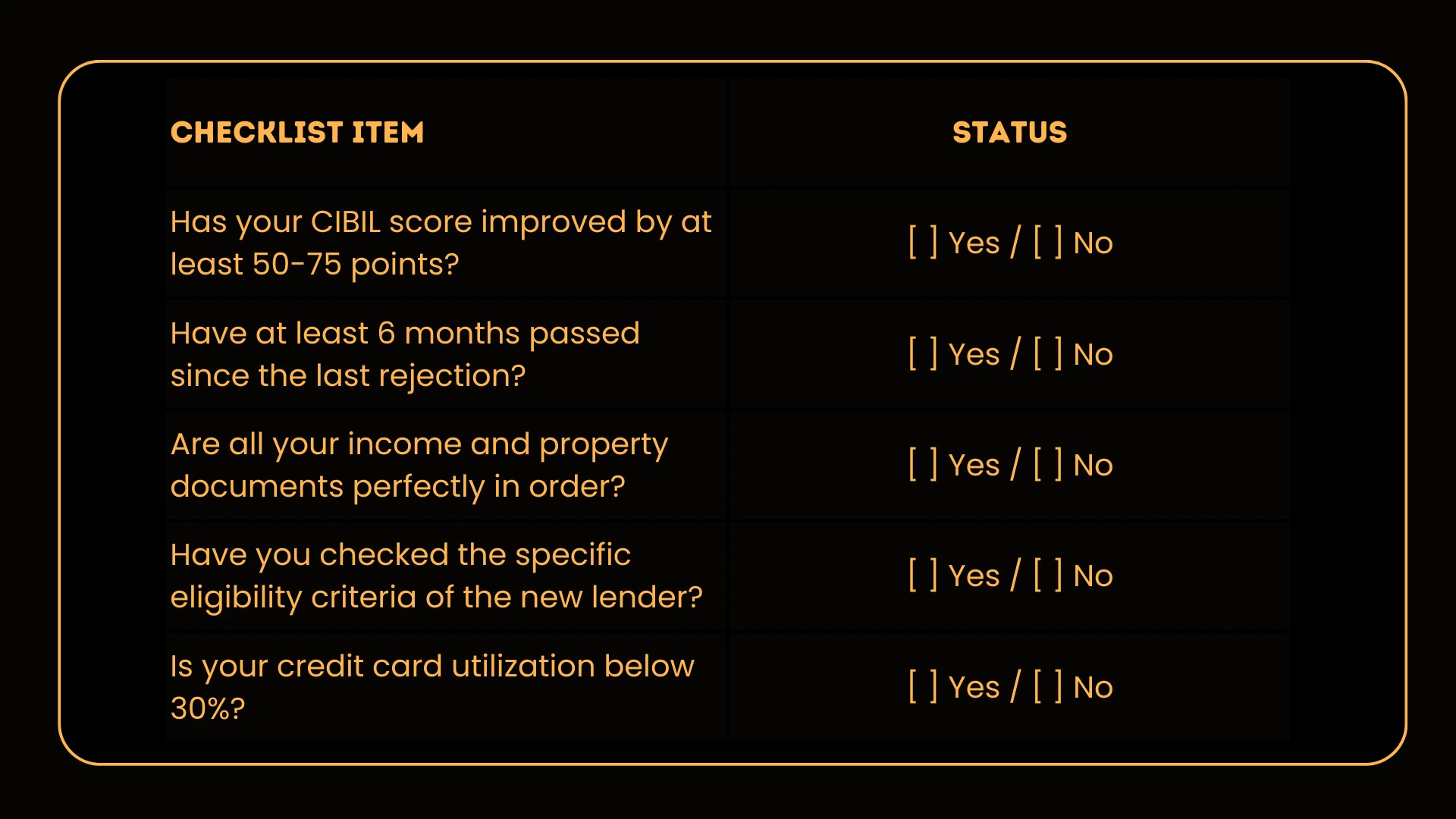

Your Final Reapplication Checklist

This checklist is your final review before you reapply for home loan after rejection, ensuring you have the best possible chance to secure a home loan with a low CIBIL score. If your individual score is still on the borderline, you might also consider the positive joint home loan CIBIL score impact, which can significantly increase your eligibility.

Conclusion: From a “No” to a “Yes”

The journey from a home loan rejection to an approval can feel long, but it is a journey you can control. A rejection is not a permanent failure; it’s a data point that reveals what needs to be fixed. Panicking and rushing will only dig a deeper hole.

By following a disciplined, strategic plan, you can transform your credit profile. You can walk back into a bank not as a high-risk applicant, but as a responsible and well-prepared future homeowner. The goal of securing a home loan with a low CIBIL score is a challenge, but with the right action plan, it is entirely achievable.

This process is a critical action item in your journey towards financial freedom, perfectly complementing our main guide, “The Ultimate Guide to CIBIL Score for Home Loans in India (2025).” Getting a home loan with a low CIBIL score is possible when you replace hope with a plan. For a broader overview of this topic, this action plan perfectly complements The Ultimate Guide to CIBIL Score for Home Loans in India (2025).

Frequently Asked Questions (FAQs)

1. What is the very first thing to do after a home loan rejection?

The absolute first thing what to do after home loan rejection is to pause and avoid immediately reapplying elsewhere, as this will only hurt your score. Your initial step in figuring out what to do after home loan rejection is to formally ask the lender for the specific reason and download your full CIBIL report for analysis.

2. What are the most common reasons for rejection of a home loan?

Beyond just a low score, the most common reasons for rejection of a home loan include a high credit utilization ratio (using too much of your credit card limit) and multiple recent hard inquiries. These reasons for rejection of a home loan signal financial instability to lenders.

3. Is it truly possible to get a home loan with a low CIBIL score in 2025?

Yes, while it is more challenging, getting a home loan with a low CIBIL score is possible, often with stricter terms like higher interest rates. This guide’s 6-month action plan is designed to improve your profile, significantly boosting your chances of securing a home loan with a low CIBIL score on better terms.

4. What is the absolute minimum CIBIL score for a home loan that banks consider?

While there is no official minimum CIBIL score for a home loan set by the RBI, most major lenders consider a score below 650 to be very high-risk. To avoid issues, your goal should be to get your score well above the perceived minimum CIBIL score for a home loan before applying.

5. What is the best way to improve a CIBIL score for a home loan?

The single best way how to improve a CIBIL score for a home loan is to create a consistent record of on-time payments for all your existing debts. Additionally, a crucial step in how to improve a CIBIL score for a home loan is to pay down credit card balances to keep your utilization below 30%.

6. Will lenders offer a home loan with a low CIBIL score if I offer a larger down payment?

Offering a larger down payment can sometimes help your case for a home loan with a low CIBIL score, as it reduces the lender’s risk. However, it is not a guarantee. Lenders will still heavily weigh your credit history, so improving your score is the most reliable strategy for getting a home loan with a low CIBIL score.

7. How long should I wait to reapply for a home loan after rejection?

It is highly recommended that you wait at least 6 months to reapply for a home loan after rejection. This period gives you sufficient time to implement a credit improvement strategy. When you reapply for a home loan after rejection, you want to present a significantly improved credit profile to the lender.

8. Are there any specific lenders who approve a home loan with a low CIBIL score?

Some NBFCs (Non-Banking Financial Companies) and smaller housing finance companies may have more flexible criteria for a home loan with a low CIBIL score compared to major national banks. However, this flexibility often comes with higher interest rates. It is always better to first improve your score before seeking a home loan with a low CIBIL score.

9. Are there other reasons for rejection of a home loan besides the CIBIL report?

Yes, other major reasons for rejection of a home loan can include unstable employment history, insufficient or unverifiable income, or issues with the property’s legal documentation. While your CIBIL is critical, these non-credit-related reasons for rejection of a home loan are also very important.

10. How can I effectively improve my CIBIL score for a home loan in just a few months?

To quickly learn how to improve your CIBIL score for a home loan, you should focus on two things: disputing any errors on your report and aggressively paying down credit card debt. Following these steps is the fastest way how to improve your CIBIL score for a home loan and see a noticeable difference.

11. Is there a waiting period before I can reapply for a home loan after rejection?

There is no official “waiting period,” but rushing to reapply for a home loan after rejection is a critical mistake that will harm your score. To successfully reapply for a home loan after rejection, a 6-month gap is the recommended timeframe to allow for meaningful credit score improvement.

12. Why do banks care about the minimum CIBIL score for a home loan so much?

Banks use the minimum CIBIL score for a home loan as a primary filter to gauge a borrower’s creditworthiness and the risk of default. A score below the acceptable minimum CIBIL score for a home loan indicates a history of poor credit management, making the applicant a high-risk investment for the bank.

13. What should I do if my home loan rejection was due to a CIBIL error?

If this is what to do after home loan rejection due to an error, you must immediately file a dispute with CIBIL. Once the error is corrected and your score improves, you can re-approach the lender with the updated report. This is the most straightforward scenario for figuring out what to do after home loan rejection.

14. Are joint applications a good strategy for getting a home loan with a low CIBIL score?

A joint application can be an excellent strategy. If your co-applicant has a high CIBIL score, it can significantly improve your chances of getting a home loan with a low CIBIL score. The lender will consider the stronger credit profile, but remember that getting a home loan with a low CIBIL score will still require your co-applicant’s score to be very strong.

15. My loan was rejected, but my score seems okay. What should I do?

If you are wondering what to do after home loan rejection with a decent score, you need to look at the other details in your report. The lender may have seen too many recent inquiries or high credit card balances. The first step in knowing what to do after home loan rejection is always to analyze the full report for these hidden red flags.

About the Author

Anwar Hashmi is the chief editor of cibilized.in, where he is dedicated to demystifying India’s credit system. He specializes in creating actionable plans for complex financial challenges, such as this guide on getting a home loan with a low CIBIL score. His expertise also crosses borders as the founder of claimcredits.online, a platform focused on helping clients navigate and claim USA Tax Credits.

Pingback: What to Do After Credit Card Application Rejected: Best 3 Step Solution - CIBILized