……Learn how to close a credit card without affecting Cibil score with Anwar Hashmi’s expert guide. Discover a safe plan to close a credit card without damaging your score…..

It’s a common scenario I see all the time as a financial writer. You open a drawer and find that old, dusty credit card you haven’t used in years. Your first instinct, a very responsible one, is to “tidy up” your finances by calling the bank to close it. It feels like the right thing to do.

But here’s a crucial question most people don’t ask: could this seemingly smart move be a hidden trap for your CIBIL score? This is a major point of confusion, and one of the most common questions I get is, “how to close a credit card without affecting Cibil score?” The answer is more complex than you might think.

My name is Anwar Hashmi, and at cibilized.in, my mission is to give you that clarity. The truth is, closing a card can have a surprisingly negative impact on your Credit Report. While this guide will give you a specific plan for how to close a credit card without affecting Cibil score, it’s important to remember this decision is part of your overall journey to improve your CIBIL score. This guide will teach you the system and give you a clear strategy for how to close a credit card without affecting Cibil score the right way.

The Two Hidden Dangers: Why Closing an Old Credit Card Decreases Your CIBIL Score

To truly understand how to close a credit card without affecting Cibil score, you must first understand the two hidden dangers that this seemingly simple action can trigger. When you call the bank to close an account, you’re not just removing a piece of plastic from your wallet; you are altering the core data on your Credit Report, and the CIBIL algorithm notices immediately.

These two consequences are the primary reasons why your score can drop unexpectedly after you close a card. Let’s break them down in detail.

Danger #1: It Shortens Your Credit History Age

The “Age of Your Credit History” is a significant factor in your score, making up about 15% of the total calculation. Lenders value a long and well-managed credit history because it provides them with more data to assess your reliability and trustworthiness as a borrower.

Think of it like a long-term friendship. A friend you’ve known and trusted for 10 years is seen as more reliable than someone you just met last month. Your oldest credit card is the anchor of that financial friendship.

It proves you have a long, stable history of managing credit. When you close that 10-year-old credit card account, you are essentially erasing your longest-standing financial “friendship” from your active record.

While the closed account will still appear on your CIBIL report for several years, it no longer contributes to the average age of your open accounts. This action reduces the average age of your credit history, which can cause an immediate and often surprising drop in your score.

Losing this history is a major setback, and it’s why the first rule of how to close a credit card without affecting Cibil score is to be extremely cautious about closing your oldest accounts.

Danger #2: It Spikes Your Credit Utilization Ratio (CUR)

This second danger is even more immediate and often more damaging. It is a critical concept in learning how to close a credit card without affecting Cibil score.

When you close a credit card, you don’t just lose its history; you lose its credit limit. This can cause your overall Credit Utilization Ratio (CUR) to spike, even if your spending habits haven’t changed at all.

Your CUR is a measure of how much of your available credit you are using. A lower CUR (below 30%) is a strong positive signal. A high CUR (above 50%) is a major red flag.

Let’s look at a simple, real-world example to see the devastating impact.

| Your Credit Profile | Before Closing Old Card | After Closing Old Card |

| Card A (10 years old) | Limit: ₹1,00,000 Balance: ₹0 | CLOSED |

| Card B (2 years old) | Limit: ₹50,000 Balance: ₹25,000 | Limit: ₹50,000 Balance: ₹25,000 |

| Total Available Limit | ₹1,50,000 | ₹50,000 |

| Total Outstanding Balance | ₹25,000 | ₹25,000 |

| Credit Utilization Ratio (CUR) | 16.6% (Excellent) | 50% (High Risk) |

As you can see, by making one simple phone call, your CUR has tripled. You’ve instantly gone from looking like a highly responsible borrower to a high-risk one in the eyes of the CIBIL algorithm, and your score will drop accordingly.

This sudden spike is why understanding how to close a credit card without affecting Cibil score is not just about the act of closing, but about its mathematical impact. Avoiding these two dangers is the real secret behind how to close a credit card without affecting Cibil score effectively.

Is It Better to Close a Credit Card or Leave It Open with a Zero Balance?

Now we arrive at the central strategic question. If closing a card can damage your score, what is the right course of action for that unused piece of plastic? The answer, in most cases, is surprisingly simple: it is almost always better to leave an old credit card open with a zero balance.

An old, well-managed credit card is not a liability; it is a powerful asset for your Credit Report. It is a testament to your long-term financial reliability. The trick isn’t to get rid of it, but to manage it correctly so it continues to work in your favor. This is the most important principle of how to close a credit card without affecting Cibil score—often, the best move is not to close it at all.

The “Sock Drawer” Strategy for Unused Cards

In my years of advising people on their credit, the best strategy I’ve found for managing old, unused cards is what I call the “Sock Drawer” strategy. It’s a simple, powerful way to preserve your credit history and keep your credit utilization low without any real effort.

This strategy applies specifically to your oldest cards that are “Lifetime Free” or have no annual fee. You simply put the physical card away in a safe place (like a sock drawer) and follow a simple plan to keep the account active and in good standing. This is the professional’s method for how to close a credit card without affecting Cibil score—by safely managing it instead.

Your “Sock Drawer” Action Checklist

Follow this simple checklist to turn your old card into a score-boosting asset:

- [ ] Set Up One Tiny Recurring Payment: Use the card for a single, small, recurring monthly bill, like your Netflix subscription, mobile recharge, or a single utility payment. This proves to the bank that the account is still active.

- [ ] Automate the Full Payment: Log in to your bank’s net banking portal and set up an auto-pay instruction to pay the “Total Amount Due” for that card every month. Since the charge is small and predictable, this is completely safe and ensures you never miss a payment.

- [ ] Store the Card Securely: Put the physical card away. This prevents you from being tempted to use it for daily spending, which could increase its balance.

By following this checklist, you get the best of all worlds: you keep your long credit history, maintain a low utilization ratio, and build a perfect payment record on the account, all on autopilot.

The Only Good Reasons to Close a Credit Card

Of course, there are some specific, logical situations where closing a credit card is the right decision. However, you should only consider it if one of the following conditions applies, and you should always be aware of the potential short-term negative impact on your CIBIL report.

- The Card Has a High Annual Fee: If an old card has a high annual fee (e.g., over ₹1,000) and you are no longer using the benefits that justify that fee (like lounge access or travel points), it makes financial sense to close it.

- You Are Upgrading to a Better Card (with the same bank): If your bank offers you an upgrade to a better card, they will often close the old one as part of the process. This is generally a safe move.

- You Are Managing a Debt Problem: If you have a serious problem with overspending, closing a credit card can be a necessary step. This is especially true if you are at risk of having the account marked as ‘Settled’, which is far more damaging to your CIBIL score.. In this case, the long-term benefit to your financial health outweighs the short-term CIBIL score dip.

- After a Divorce or Separation: If you have a joint credit card with a former partner, it is crucial to close that account to separate your financial lives and protect your Credit Report from their future spending habits.

Even in these cases, the core strategy of how to close a credit card without affecting Cibil score remains the same: ensure your other cards have very low balances to absorb the impact of the reduced credit limit. Understanding how to close a credit card without affecting Cibil score is about making a calculated, strategic decision, not an emotional one.

How to Close a Credit Card Without Affecting CIBIL Score (As Much as Possible)

You’ve weighed the pros and cons and have decided that closing a specific credit card is the right financial move for you. Now, the goal is to execute this process in the most professional and strategic way possible to minimize the negative impact on your CIBIL score.

While the two dangers we discussed—a shorter credit history and a higher CUR—are often unavoidable, following a clean, official process can prevent further complications. This is the practical, step-by-step answer to the question of how to close a credit card without affecting Cibil score more than absolutely necessary.

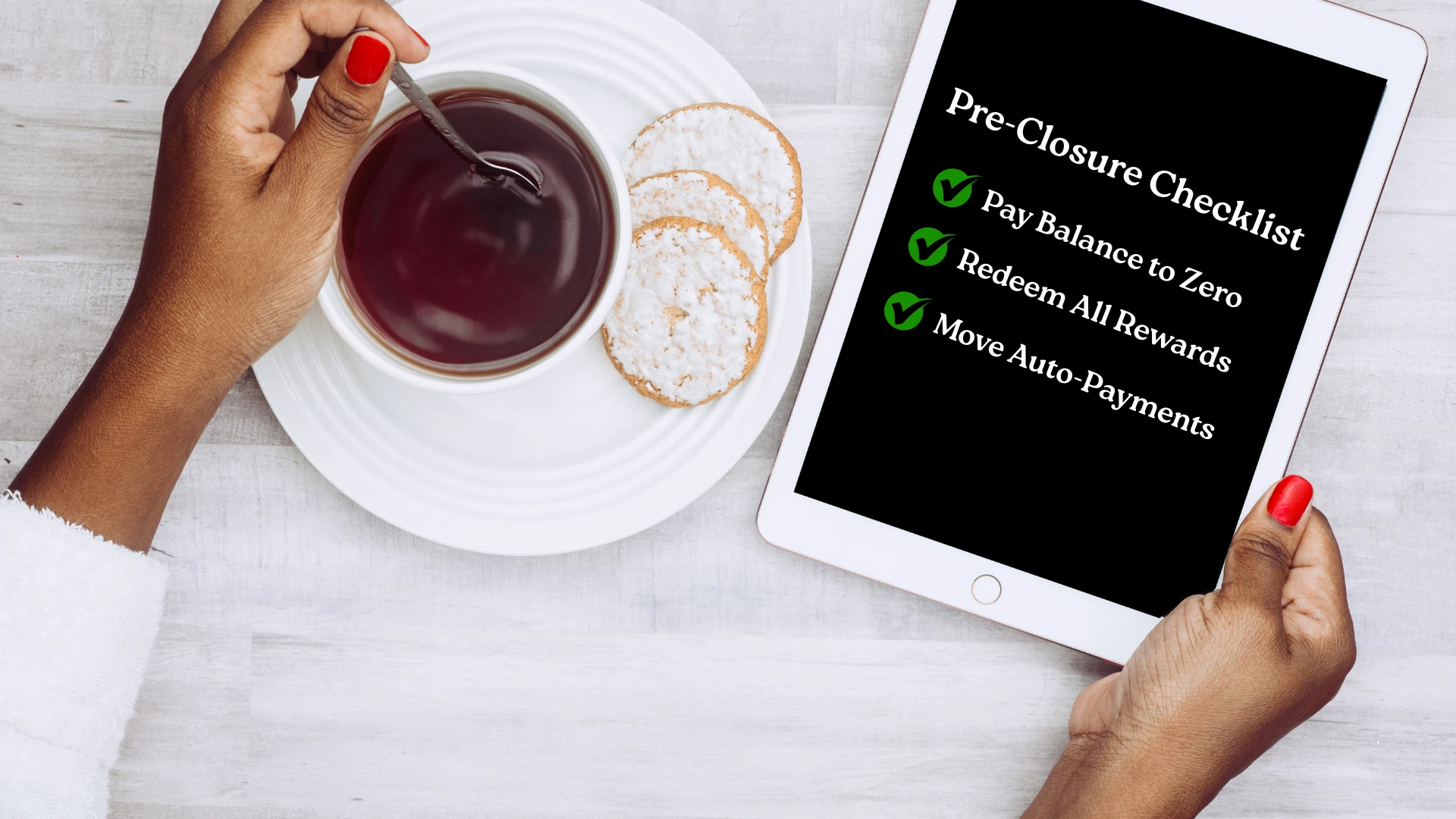

The Pre-Closure Checklist

Before you even think about contacting the bank, you must do some essential housekeeping. Completing this checklist is a non-negotiable first step. Rushing to close a card without this preparation can lead to missed payments and further credit damage, which is the opposite of our goal.

Your Pre-Closure Action Checklist:

- [ ] Pay Off the Entire Outstanding Balance to Zero: You cannot close a credit card that has any outstanding balance, even a single rupee. Log in to your net banking portal and clear the entire amount due, not just the minimum.

- [ ] Redeem All Your Reward Points: This is a step most people forget, and it’s like throwing away free money. Once you close your account, any accumulated reward points, cashback, or air miles are forfeited forever. Redeem every last point before you proceed.

- [ ] Move All Linked EMIs or Auto-Payments: Do you have any ongoing EMIs on the card? Or have you linked it for auto-payments on services like Netflix or your mobile bill? You must contact those service providers and move these payments to another card before you request closure. Forgetting this step will cause those payments to fail, resulting in late fees and a new negative mark on your Credit Report.

Completing this checklist is the foundation of how to close a credit card without affecting Cibil score professionally.

The Official Closure Process

Once your pre-closure checklist is complete, you can formally request the closure. It’s crucial to follow the official process to ensure the account is properly closed and updated with the credit bureaus.

Step 1: Contact the Bank

You can typically request a closure through several channels:

- Phone Banking: Call your bank’s customer care helpline and follow their instructions.

- Email: Send a formal written request to the bank’s official support email address.

- Branch Visit: Visit your nearest bank branch and submit a physical application form.

Step 2: Get Written Confirmation

This is the most important part of the entire process of how to close a credit card without affecting Cibil score. After the bank processes your request, they must provide you with a formal, written confirmation of the account closure. This could be a final letter or an email. Do not consider the account closed until you have this proof in your hands.

Step 3: Check Your Next Credit Report

About 30-45 days after receiving your closure confirmation, download a fresh CIBIL report. Check the “Account Information” section to verify that the card’s status is now officially marked as “Closed.” This final verification is the ultimate confirmation that you have successfully learned how to close a credit card without affecting Cibil score in the long run. If the account is still showing as “Active,” you must immediately contact the bank with your written confirmation and demand they update the bureaus. This meticulous follow-up is a key part of how to close a credit card without affecting Cibil score and protecting your financial record.

The “Oops” Moment: I Already Closed My Oldest Card. How Do I Recover?

It’s a moment of panic I’ve heard about from countless readers. You close an old credit card, thinking you’re being responsible. A month later, you check your CIBIL score and see that it has dropped by 20, 30, or even 50 points. You realize, with a sinking feeling, that you might not have known how to close a credit card without affecting Cibil score the right way.

If this has happened to you, the first thing I want you to know is this: do not panic. While the short-term damage is real, it is not an irreversible disaster. You have a clear path to recovery. This section is your step-by-step guide to rebuilding your score after closing an old account.

Assessing the Damage on Your Credit Report

Before you can start rebuilding, you need to understand the exact extent of the damage. You must become a detective and analyze your new credit profile to see how the closure has impacted the two most critical factors we discussed.

Your Damage Assessment Checklist:

- Pull Your Latest Credit Report: Wait about 30-45 days after you receive closure confirmation from the bank, then download a fresh CIBIL report. This will give you the updated data you need for your analysis.

- Check Your New “Average Credit Age”: While your report won’t explicitly state your “average” age, you can get a good idea by looking at the “Date Opened” for your oldest remaining credit account. If your 10-year-old card is gone and your oldest remaining card is only 2 years old, you know your credit history has been significantly shortened.

- Re-Calculate Your Credit Utilization Ratio (CUR): This is the most important calculation you will make. Look at the total outstanding balance on all your remaining credit cards and the new, lower total credit limit. Re-calculate your CUR. This will show you exactly how much “riskier” you now appear to lenders, and why it’s so important to know how to close a credit card without affecting Cibil score.

The Recovery Plan

Now that you understand the damage, it’s time to execute a disciplined recovery plan. Think of this as the damage control phase. While the ideal situation is knowing how to close a credit card without affecting Cibil score beforehand, this plan is your path to rebuilding.

Step 1: Flawless Payment History is Now Non-Negotiable

From this moment forward, every single EMI and credit card bill must be paid on time, without fail. A perfect payment history is the most powerful tool you have to counteract the negative impact of the account closure. Set up auto-pay and calendar reminders immediately.

Step 2: Keep Balances on Remaining Cards Ultra-Low

Because your total credit limit is now lower, your remaining cards are more sensitive to high balances. Your new goal should be to keep your overall CUR not just below 30%, but ideally below 10% for the next few months. This will help to offset the damage from the increased utilization and is a key part of how to close a credit card without affecting Cibil score in the future.

Step 3: Re-Anchor Your Credit History (The Authorized User Strategy)

This is a powerful, advanced strategy that can directly counteract the damage of a shortened credit history. You can ask a trusted family member with a long and perfect credit history (like a parent or spouse) to add you as an “authorized user” on their oldest credit card.

When they do this, the entire positive history of their old, well-managed account can be added to your Credit Report. A strong credit history is particularly crucial when you are planning for major life goals, such as applying for a home loan.

This is an excellent recovery tactic for those who didn’t know how to close a credit card without affecting Cibil score and are now looking to fix it.

Your Top Questions About Closing a Credit Card, Answered

1. What is the most common reason a CIBIL score drops after closing a credit card?

The most common reason your CIBIL score drops is the sudden spike in your Credit Utilization Ratio (CUR). When you close a card, you lose its credit limit, which can make your existing balances seem much larger in comparison, instantly impacting your CIBIL score.

2. What is the biggest myth about how to close a credit card without affecting Cibil score?

The biggest myth is that closing a card with a zero balance has no impact. The best strategy for how to close a credit card without affecting Cibil score is often not closing it at all to preserve your valuable credit history. Following a safe plan for how to close a credit card without affecting Cibil score is about understanding both your CUR and your credit history age.

3. How long does a closed account stay on my credit report?

A closed account will remain on your credit report for a significant period. An account in good standing can stay on your credit report for up to 10 years, which is a good thing as it continues to contribute positively to your credit history age.

4. Is there a “right” time of the month to close a credit card account?

While there’s no magic day, the best time to request a closure is right after you have confirmed your outstanding balance is exactly zero and your statement has been generated showing this. This ensures there are no lingering charges that could complicate the process.

5. If I made a mistake, is there a recovery plan for how to close a credit card without affecting Cibil score?

Yes, if you’ve already closed an old card, the recovery plan is to focus on the other factors. The best recovery plan after not knowing how to close a credit card without affecting Cibil score correctly is to maintain a flawless payment history and keep the balances on your remaining cards ultra-low. Rebuilding from this mistake requires following a disciplined plan for how to close a credit card without affecting Cibil score with your other accounts.

6. Does the age of my credit history really matter that much?

Yes, the age of your credit history is a very important factor, making up about 15% of your score. A longer age of your credit history shows lenders that you have a stable, long-term track record of managing credit responsibly.

7. Is it better to have one high-limit card or multiple low-limit cards?

From a CIBIL score perspective, it is generally better to have a few well-managed cards than just one. This helps build a more diverse credit profile. However, the most important factor is always keeping your overall Credit Utilization Ratio low across all cards.

8. What is the most important pre-closure step in how to close a credit card without affecting Cibil score?

The most critical step is ensuring all linked auto-payments and EMIs are moved to another account before you request closure. This single action prevents failed payments, which would be a huge setback in your plan for how to close a credit card without affecting Cibil score. Forgetting this is a common mistake, so a careful plan for how to close a credit card without affecting Cibil score must include this check.

9. How does my Credit Utilization Ratio impact my CIBIL score?

Your Credit Utilization Ratio is the second most important factor in your score. A high Credit Utilization Ratio (above 30%) signals to lenders that you may be financially stressed, making you a higher risk.

10. What is the absolute best way to handle an old, unused credit card?

The best strategy is to keep the card open and use the “Sock Drawer” method. Make one tiny, recurring purchase on it each month and set up an auto-pay for the full amount. This preserves your credit history and keeps the account active with almost no effort.

11. Is there a simple checklist for how to close a credit card without affecting Cibil score?

Yes, our pre-closure checklist is your best guide. The key steps in any plan for how to close a credit card without affecting Cibil score are: 1) Pay the balance to zero, 2) Redeem all rewards, and 3) Move all auto-payments. This disciplined approach is the foundation of how to close a credit card without affecting Cibil score safely.

12. If I close a card with a negative history, will the negative marks disappear?

No. Closing a card with a negative history (like past late payments) will not remove those negative marks. The account will be marked as “Closed,” but the record of late payments will remain on your credit report for up to seven years.

13. What is the primary benefit of the “Sock Drawer Strategy”?

The primary benefit of this strategy is that it preserves the age of your credit history, which is a crucial positive factor for your CIBIL score. By keeping your oldest account active, you are protecting a valuable asset on your credit history.

14. What if I want to close a card with a high annual fee?

Closing a card with a high annual fee that you no longer get value from is one of the few valid reasons to close an account. This is a smart financial decision, and it is a key exception to the rule of not closing old cards.

15. What is the most critical advice for someone learning how to close a credit card without affecting Cibil score?

The most critical advice is to be strategic, not emotional. The best plan for how to close a credit card without affecting Cibil score is to always analyze the impact on your Credit Utilization Ratio and your credit history age before you make the call. Remember, the ultimate goal of learning how to close a credit card without affecting Cibil score is to protect your long-term financial health.

What’s the best strategy for how to close a credit card without affecting Cibil score if I have several cards and want to simplify?

This is an excellent strategic question. When you have multiple cards, the best plan for how to close a credit card without affecting Cibil score is to follow a “Keep Your Best, Cut the Rest” hierarchy. First, never close your oldest card, as it is the anchor of your credit history. Second, prioritize keeping the card with your highest credit limit, as this will protect your overall Credit Utilization Ratio. After that, you can consider closing newer cards with low limits and high annual fees. Following this careful prioritization is the professional’s approach to how to close a credit card without affecting Cibil score while still successfully simplifying your finances.

The Final Verdict: Your Strategic Decision

The decision to close a credit card often comes from a responsible place—a desire to simplify your financial life. However, as this guide has shown, this seemingly simple action has complex and often negative consequences for your CIBIL score.

The most important lesson is to shift your perspective: an old, well-managed, no-fee credit card is not a liability; it is one of your most powerful credit-building assets.

It anchors the age of your Credit Report and provides a vital boost to your total available credit limit, which helps keep your utilization ratio low. Managing this asset correctly is a key component of a larger financial strategy.

Now that you understand how to protect your credit history, you can focus on the other core principles of building a flawless credit profile. For those ready to explore the complete framework, from mastering on-time payments to leveraging advanced tactics, our main guide on improving your CIBIL score provides a comprehensive, step-by-step plan.

Author

I wrote this guide because the question of how to close a credit card without affecting Cibil score is one of the most misunderstood topics in personal finance, often leading to costly mistakes. My goal is to provide you with the strategic clarity to make the right choice for your long-term financial health.

- Anwar Hashmi, founder of

cibilized.in. For expertise on American finance, he is also the lead author atClaimCredits.online, specializing in USA Tax Credits.

Pingback: 5 Credit Card Hidden Charges in India Draining Your Bank Account - CIBILized

Pingback: Unauthorized Transaction on Credit Card India: 3 Critical Steps To Resolve it