Confused by your bill? Our expert guide on how to read your credit card statement makes it simple. Learn how to read your credit card statement like a pro, understand every charge, and avoid costly hidden fees forever.

The Most Misunderstood Document in Your Mailbox

The “Bill Shock” and Confusion Moment

Your credit card bill arrives. It’s a wall of numbers, dates, and confusing terms. You know what you spent, but the final total, the “Finance Charges,” and the different dates can feel like a complex puzzle. This confusion is common, and this guide will make you an expert.

I’ve spoken with countless new cardholders who experience this “bill shock.” They feel like they’ve been penalized, but they’re not even sure what rule they broke. This is why knowing how to read your credit card statement is the most fundamental skill for any cardholder.

What This Guide Will Do For You

My name is Anwar Hashmi, and at cibilized.in, my mission is to replace that confusion with confidence. This is a complete masterclass on how to read your credit card statement.

By the end, you will understand every single section, from the “summary of charges” to the “interest calculation,” and you will have a foolproof plan to pay your bill correctly and avoid all fees.

This guide will give you a clear, step-by-step framework. You will not only learn the basics of how to read your credit card statement, but you will also learn to spot potential red flags and manage your account like a pro.

This skill is the foundation of a healthy financial life. By taking control of your bills, you are taking the first and most important step in your journey to improve your CIBIL score.

The Anatomy of Your Statement: A Visual Breakdown

To protect yourself from unexpected fees and take control of your finances, you must first learn to read your credit card bill like an expert. Banks often design these statements to be dense and confusing, highlighting the large, friendly “Total Amount Due” while burying the most important details in columns of fine print.

This is where the traps are hidden, and it’s why mastering how to read your credit card statement is such a critical skill.

In my experience as a financial writer, the vast majority of “bill shock” moments happen simply because people don’t know where to look. This section is your guided tour. We will dissect the anatomy of a typical bill and show you exactly where to focus your attention to spot every important detail.

The Core of the Guide

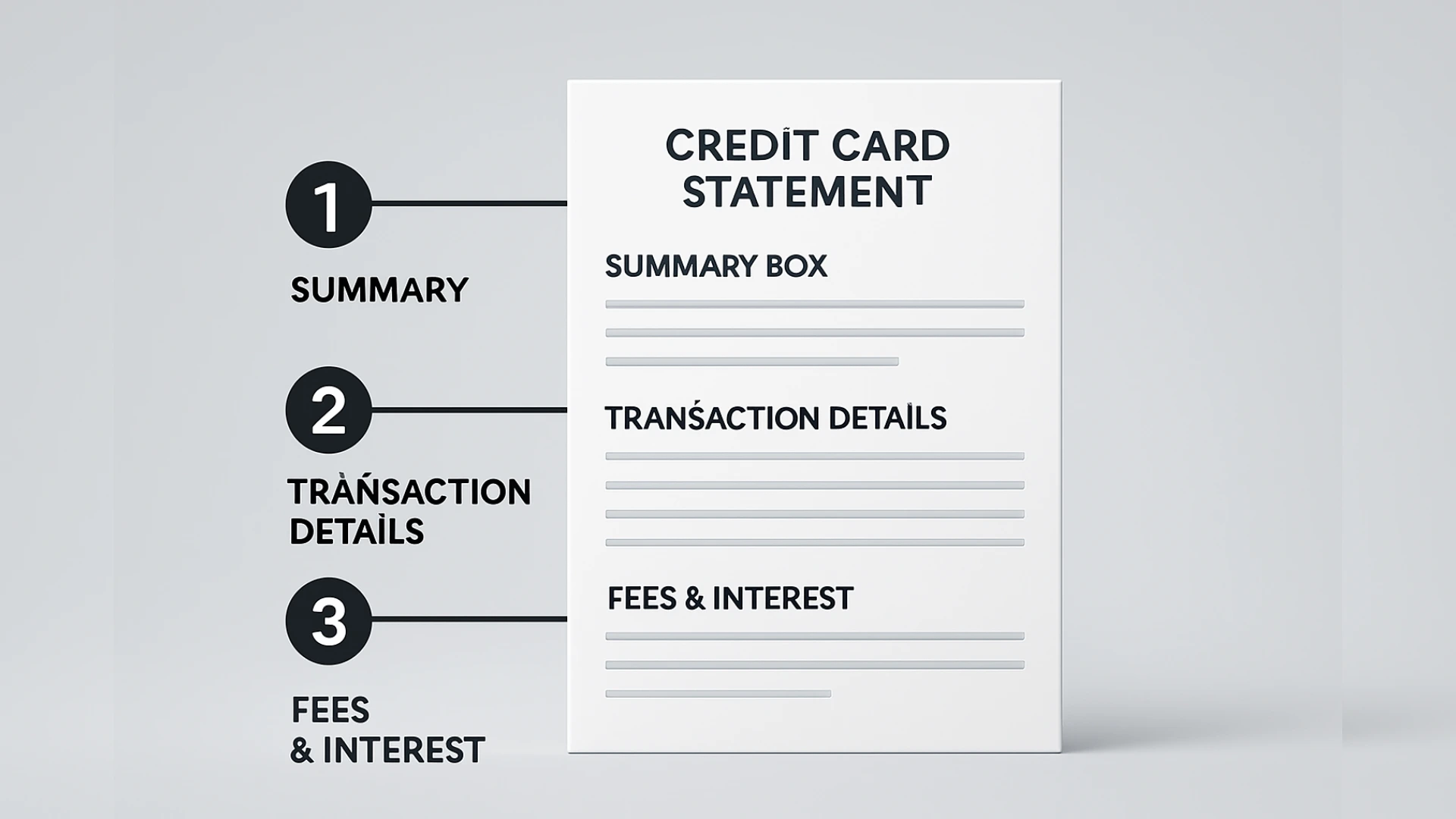

Learning how to read your credit card statement is not about reading every single line; it’s about knowing which three sections hold all the power. We will use a visual breakdown to guide you through your own bill.

Section 1 – The Summary Box: Your Financial Dashboard

This is the most important section, usually located at the very top of your bill. It provides a quick snapshot of your account’s current status. You should never pay your bill without first verifying every number in this box.

Here are the critical numbers you need to understand:

- Total Amount Due: This is the full amount you need to pay by the due date to avoid all interest charges.

- Minimum Amount Due: This is the small percentage (usually 5%) that the bank requires you to pay to avoid a “late payment” penalty. As we’ll discuss later, paying only this amount is a significant financial trap.

- Payment Due Date: This is the final deadline to make your payment.

- Statement Date: This is the date the bill was generated and is the secret to a powerful credit score hack we will cover later.

- Credit Limit: Your total approved spending limit.

- Available Credit Limit: Your total limit minus your current outstanding balance.

Understanding these key figures is the first and most important part of how to read your credit card statement.

Section 2 – The Transaction Details: Your Spending Diary

This is a detailed, line-by-line list of every transaction you have made during the billing cycle. It includes purchases, payments you’ve made, credits or refunds you’ve received, and any fees that have been charged.

When you are learning how to read your credit card statement, it is essential to scan this section for two things:

- Accuracy: Do you recognize every single transaction? An unfamiliar charge could be a simple billing error or, in a worst-case scenario, a sign of fraudulent activity.

- Refunds: If you returned an item and were expecting a refund, have you confirmed that the credit has been applied to your account?

A key part of how to read your credit card statement is treating it like a bank account passbook—every entry must be verified.

Section 3 – The Fees & Interest Calculation: The Hidden Costs

This is often a small, dense table at the bottom of your statement, but it’s where the most expensive secrets are hidden. This is where you will find the answers to why your bill is higher than you expected.

Look for specific line items such as:

- Annual Fees: A yearly charge for using the card.

- Late Payment Charges: The penalty for missing a due date.

- Finance Charges (Interest): The interest charged on any unpaid balance.

Understanding these charges is a critical part of learning how to read your credit card statement effectively. In the next sections, we will do a deep dive into these traps and show you how to avoid them.

Mastering this section is the most advanced part of how to read your credit card statement, and it’s the skill that will save you the most money. The entire process of how to read your credit card statement is about moving from being a passive consumer to a vigilant financial manager.

The “Minimum Amount Due” Trap: The Most Dangerous Number on Your Bill

We now arrive at the single most dangerous and misunderstood number on your entire bill: the “Minimum Amount Due.” This small figure, usually just 5% of your total balance, is presented by banks as a helpful, flexible payment option.

In my experience as a financial writer, I can tell you with absolute certainty that it is not. It is a carefully designed trap that keeps millions of Indians in a cycle of high-interest debt.

Understanding this trap is the most important lesson in learning how to read your credit card statement. It is the difference between using a credit card as a convenient tool and letting it become a source of significant financial stress. This section will be a deep dive into this crucial concept.

The High Cost of Convenience

When you pay only the minimum amount, you are not charged a “late fee,” and your payment history on your CIBIL report remains clean. This gives the false impression that you are managing your account responsibly.

However, the moment you fail to pay the Total Amount Due, you lose your interest-free grace period, and the bank begins charging a devastatingly high interest rate on your remaining balance.

This is not a simple interest calculation; it is a system of daily compounding interest that can cause your debt to snowball exponentially. This is the painful secret that makes understanding how to read your credit card statement so vital.

H4: The Math of the Minimum Payment Trap

Let’s look at a clear, real-world example to see the devastating impact. Imagine you have an outstanding bill of ₹20,000 on a card with a monthly interest rate of 3.5% (which is a massive 42% APR). The minimum payment is 5%, or ₹1,000.

You decide to pay only the minimum each month. Here’s what happens:

| Month | Opening Balance | Interest Charged (at 3.5%) | Minimum Payment | Principal Paid | Closing Balance |

| 1 | ₹20,000 | ₹700 | ₹1,000 | ₹300 | ₹19,700 |

| 2 | ₹19,700 | ₹690 | ₹1,000 | ₹310 | ₹19,390 |

| 3 | ₹19,390 | ₹679 | ₹1,000 | ₹321 | ₹19,079 |

Export to Sheets

As you can see, after three months of paying ₹3,000, you have only reduced your original debt by less than ₹1,000. The vast majority of your payment has been eaten up by interest.

If you continue this pattern, it could take you over 7 years to pay off that single ₹20,000 purchase, and you would end up paying over ₹30,000 in interest alone. This is not a hidden fee; it’s a feature of the system that preys on those who don’t know how to read their credit card statement properly.

This is why learning how to read your credit card statement is so crucial for your financial health.

The Impact on Your CIBIL Score

The trap is even more insidious because of its dual impact on your CIBIL score. Paying the minimum amount is a clever way to avoid one negative mark while creating another, more serious one. This is a critical nuance in understanding how to read your credit card statement for CIBIL health.

H4: The Payment History Illusion

When you pay the minimum amount by the due date, the bank reports your payment as “on-time” to CIBIL. This means you will not get a “DPD” (Days Past Due) mark on your payment history. This creates the illusion that your CIBIL score is safe.

H4: The Real Damage: Your Credit Utilization Ratio (CUR)

This is where the real damage happens. By paying only the minimum, you are carrying over a large balance to the next month. This means your Credit Utilization Ratio (the percentage of your available credit limit that you are using) will remain very high.

As we know, a high CUR is the second biggest factor that pulls your CIBIL score down. The CIBIL algorithm sees your high balance as a major red flag, signaling that you are overly reliant on credit and are under financial stress.

So, even though your payment history looks perfect, your score will stagnate or even drop because your CUR is consistently high. This is the expert’s insight into how to read your credit card statement—looking beyond the payment status to the utilization.

A key part of how to read your credit card statement is understanding that paying the minimum is a signal of financial distress to the CIBIL system. In summary, if your goal is how to read your credit card statement to improve your score, the “Minimum Amount Due” is a number to be ignored. The only number that matters is the “Total Amount Due.”

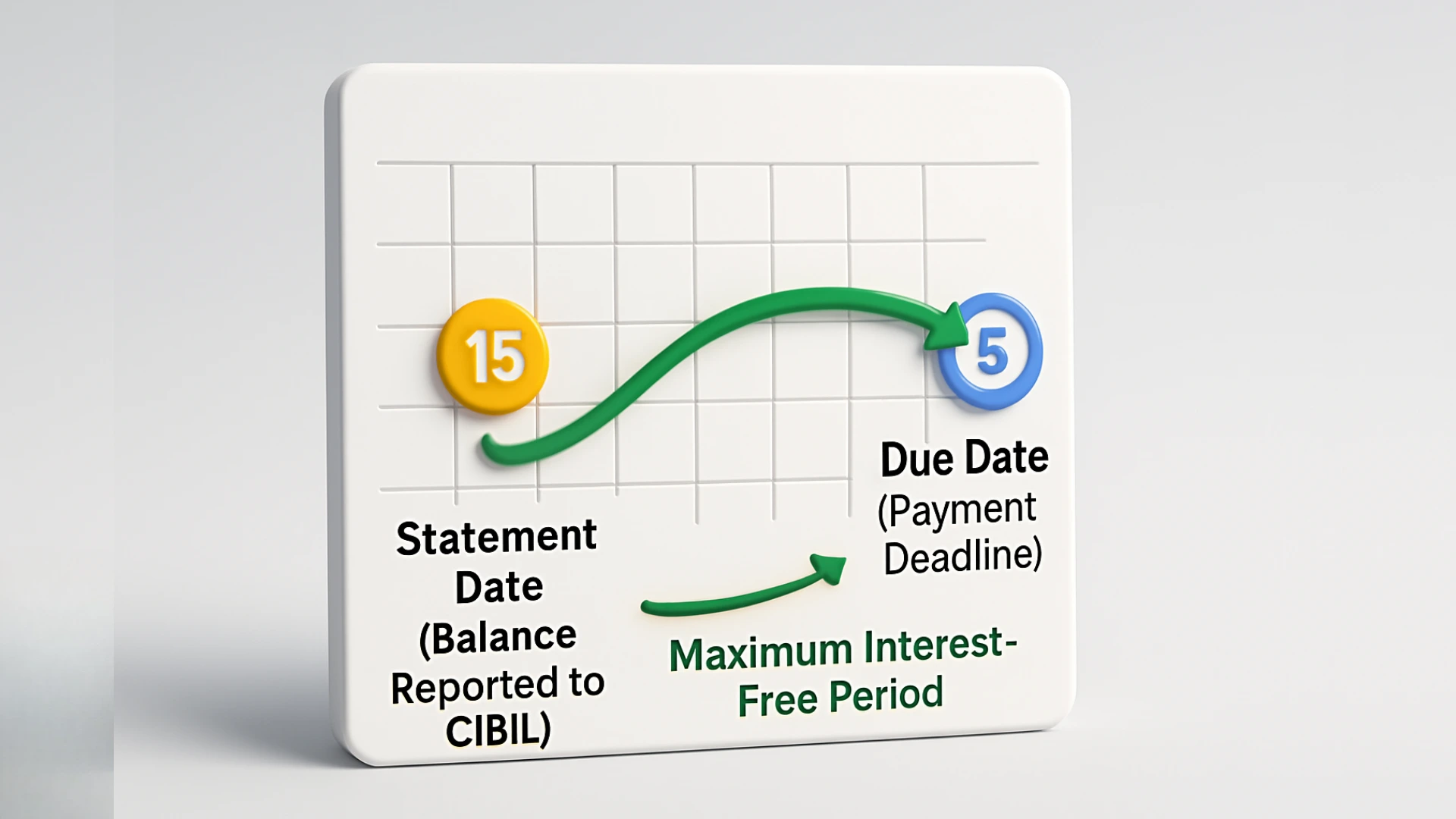

Mastering the Dates: Statement Date vs. Due Date

You now understand the main sections of your bill, but to truly become a master of your credit card, you must understand the engine that runs it: the billing cycle. The interplay between your “Statement Date” and your “Due Date” is where you can either save a significant amount of money or fall into a costly interest trap.

In my experience, this is the single most valuable piece of knowledge for any cardholder. It transforms you from a passive user into a strategic planner. This is the expert level of how to read your credit card statement, and it’s the key to unlocking your card’s most powerful feature: the interest-free period.

The “Interest-Free Period” Explained

Every credit card in India offers a feature called the “interest-free period” or “grace period.” This is a window of time, often advertised as “up to 45-50 days,” during which you are not charged any interest on your purchases. This is the superpower of a credit card; it’s essentially a free, short-term loan.

However, this period is not a fixed number of days. It is a dynamic window that depends entirely on when you make a purchase within your billing cycle. Understanding this timing is a huge “aha!” moment for anyone learning how to read their credit card statement strategically.

Let’s use a clear, step-by-step example with a visual timeline to make this simple.

Meet Priya. Here is her credit card’s billing cycle:

- Statement Date: The 15th of every month.

- Due Date: The 5th of the following month.

Scenario A: Priya makes a purchase at the START of her billing cycle. On October 16th, the very first day of her new cycle, Priya buys a new phone for ₹30,000. This transaction will appear on her next bill, which is generated on her Statement Date, November 15th. The Due Date for this bill is December 5th.

Let’s count the days. From the date of her purchase (Oct 16) to the final payment deadline (Dec 5), Priya has received 50 days of an interest-free loan from the bank.

Scenario B: Priya makes a purchase at the END of her billing cycle. Now, let’s say Priya buys the same phone on November 14th, just one day before her statement is generated. This transaction will also appear on her November 15th bill, and the Due Date is still December 5th.

Let’s count the days again. From the date of her purchase (Nov 14) to the final payment deadline (Dec 5), Priya has only received 21 days of an interest-free period.

This is the secret. By strategically timing her large purchase to be right after her statement date, she could have maximized her interest-free period. This is the ultimate pro-level technique for how to read your credit card statement to your advantage. This is how to read your credit card statement not just for information, but for strategy.

The Golden Rule: How You Lose the Grace Period

The interest-free period is a privilege, not a right. It is a reward the bank gives you for being a “transactor”—someone who uses the card for convenience and pays it off in full. The moment you become a “revolver”—someone who carries a balance—that privilege is instantly revoked.

This is the Golden Rule of credit cards, and it is absolute: If you do not pay your “Total Amount Due” in full by the “Due Date,” you lose the interest-free grace period on ALL new purchases.

Let’s be very clear about what this means. If your bill is ₹20,000 and you only pay ₹19,999, you have not just incurred interest on the remaining ₹1; you have flipped a switch in the bank’s system. From that point forward, every new purchase you make will start accruing high-interest charges from the very day of the transaction.

You will only get your interest-free period back after you have paid your entire outstanding balance down to zero. Forgetting this rule is the most common reason people get caught in a debt spiral, and it highlights why knowing how to read your credit card statement and its terms is so critical.

This is a non-negotiable part of how to read your credit card statement for wealth building. The best way to use this guide on how to read your credit card statement is to apply this rule without fail.

A key takeaway for how to read your credit card statement is that the “Total Amount Due” is the only number that guarantees you pay zero interest.

Frequently Asked Questions About How to Read Your Credit Card Statement

1. What is the most important part of how to read your credit card statement for the first time?

The most important part of how to read your credit card statement is to focus on the “Summary Box.” This section contains the three critical numbers: Total Amount Due, Minimum Amount Due, and the Payment Due Date. Mastering this part is the foundation of how to read your credit card statement correctly.

2. What is the main difference in a credit card billing cycle?

The main difference in a credit card billing cycle is between the Statement Date and the Due Date. The Statement Date determines what balance is reported to CIBIL, while the Due Date is your deadline to pay. Understanding this is key to managing your credit card billing cycle.

3. Why is it so important how to read your credit card statement carefully every month?

It is crucial how to read your credit card statement carefully to spot incorrect charges, fraudulent transactions, or hidden fees. By learning how to read your credit card statement, you transform from a passive consumer into a vigilant financial manager, saving money and protecting your CIBIL score.

4. How does the minimum amount due trap work?

The minimum amount due trap works by charging a very high-interest rate on the remaining balance if you don’t pay in full. It can take years to clear your debt if you only pay the minimum amount due, costing you thousands in interest.

5. What is a credit card’s interest-free period?

A credit card’s interest-free period is the time between your purchase and your payment due date, during which you are not charged interest if you pay the total bill in full. You lose the interest-free period on all new purchases if you fail to pay your previous bill completely.

6. What is the best strategy for how to read your credit card statement to save money?

The best strategy for how to read your credit card statement to save money is to find your Statement Date and Due Date. By timing large purchases for right after the Statement Date, you can maximize your interest-free period. This pro-level tip is the essence of how to read your credit card statement strategically.

7. How do banks calculate finance charges?

Banks calculate finance charges on a daily basis on your outstanding balance once you lose your interest-free grace period. These finance charges are what make carrying a balance so expensive.

8. What is the main difference between the statement date vs due date?

The main difference between the statement date vs due date is their CIBIL impact. The statement date sets the balance for your utilization ratio, while the due date determines your payment history. Understanding the statement date vs due date is critical for score improvement.

9. How does understanding how to read your credit card statement help my CIBIL score?

Understanding how to read your credit card statement directly helps your CIBIL score by allowing you to manage your Credit Utilization Ratio. By knowing your statement date, you can pay down your balance before it’s reported, which is a key part of how to read your credit card statement for a higher score.

10. How does a high Credit Utilization Ratio get calculated from my statement?

Your Credit Utilization Ratio is calculated using the outstanding balance shown on your statement. A high Credit Utilization Ratio is a major negative factor for your CIBIL score, even if you pay on time.

11. Can I dispute an incorrect charge I find on my bill?

Yes, if you find an incorrect charge, you should call your bank’s customer service immediately to dispute it. Regularly checking your transaction list for an incorrect charge is a vital habit.

12. Is the Total Amount Due the only amount I should focus on?

Yes, the Total Amount Due is the most important number on your bill. Paying the Total Amount Due in full by the due date is the only way to avoid all interest charges.

13. What is a common mistake when learning how to read your credit card statement?

A common mistake when learning how to read your credit card statement is only looking at the Due Date and ignoring the Statement Date. The secret to a faster score boost lies in managing the balance on your Statement Date, a key lesson for how to read your credit card statement like a pro.

14. Does my payment history get affected if I only pay the minimum?

No, your payment history will be marked as “on-time” as long as you pay the minimum amount by the due date. However, your CIBIL score will still be damaged by the high utilization, which is why a good payment history alone is not enough.

15. Where do I find fees and charges on the statement?

You can find fees and charges in the “Summary of Charges” or “Transaction Details” section of your bill. It’s crucial to audit this section every month to spot any unexpected fees and charges.

16. How does the transaction list help me understand my credit card bill?

The transaction list helps you understand your credit card bill by providing a line-by-line record of your spending. You should always review it to ensure all charges are accurate and to get a clear picture of your spending habits, which is the first step to better understanding your credit card bill.

From Confused User to Confident Cardholder

That credit card statement that once felt like a confusing, intimidating puzzle is now a clear and simple roadmap. As this guide has shown, the power to control your finances has been in your hands all along; you just needed to know where to look.

The most important takeaway is this: learning how to read your credit card statement is the single most important skill for responsible credit card ownership.

It is your first and best defense against hidden fees, costly interest traps, and billing errors. By making the 5-minute “Bill Audit” a non-negotiable monthly habit, you have transformed from a passive consumer into a vigilant and empowered financial manager.

You now understand the critical difference between your Statement Date and your Due Date. This knowledge is the key to unlocking more advanced strategies.

Now that you’ve mastered reading your bill, the next step is to use that knowledge to proactively boost your score. The ultimate pro-level tactic for this is learning how to pay your bill before the statement date, a hack that can dramatically accelerate your CIBIL score improvement.

Author’s Note

A Note from the Author: I wrote this guide because the question of how to read your credit card statement is the first and most important step to avoiding hidden fees and taking control of your finances. My mission is to make these complex documents simple for everyone.

- Anwar Hashmi, founder of

cibilized.in. For expertise on American finance, he is also the lead author atClaimCredits.online, specializing in USA Tax Credits.

Pingback: Unauthorized Transaction on Credit Card India: 3 Critical Steps To Resolve it