Can you fix this? Yes. To completely clear a “settled” remark, you must contact your original lender, pay the remaining outstanding balance in full, obtain a No Dues Certificate (NOC), and have the bank update your account to “Closed”.

While the process sounds simple in theory, banks often make it incredibly difficult and time-consuming. In this complete 2026 guide, we will give you the exact blueprint to fix your credit report without getting trapped by fake settlement agencies or losing your hard-earned money.

Inside this guide, you will discover:

- The critical difference between “Settled” and “Written-off”.

- Our interactive Loan Settlement Future Cost Analyzer.

- A step-by-step action plan to legally convert your status to “Closed”.

Quick Answer: How to Remove Settled Status from CIBIL

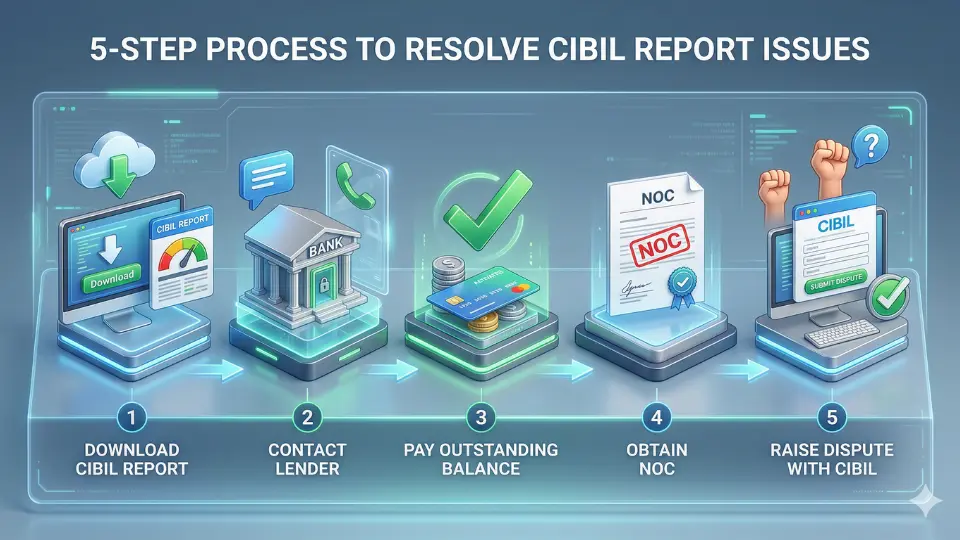

If you want to remove settled status from CIBIL and restore your credit profile, you must follow these legal steps:

- Download your CIBIL report and identify the account marked as “Settled”.

- Contact the original lender (bank or NBFC) that reported the settlement.

- Pay the remaining outstanding balance in full to clear the bank’s financial loss.

- Obtain a No Dues Certificate (NOC) confirming that the loan balance is zero.

- Raise a dispute with CIBIL online and upload the NOC to update the account status to “Closed”.

Once the lender confirms the correction, the credit bureau usually updates the report within 30–45 days. After the status changes from Settled to Closed, you can gradually rebuild a good CIBIL score in India by maintaining timely payments and responsible credit usage.

Settled Meaning in CIBIL”: What Does it Actually Indicate?

Imagine you owe ₹5 Lakh on an HDFC personal loan, but due to severe financial hardship, you miss multiple EMIs. After months of intense follow-ups, the bank finally offers a compromise: pay just ₹2 Lakh to end the matter.

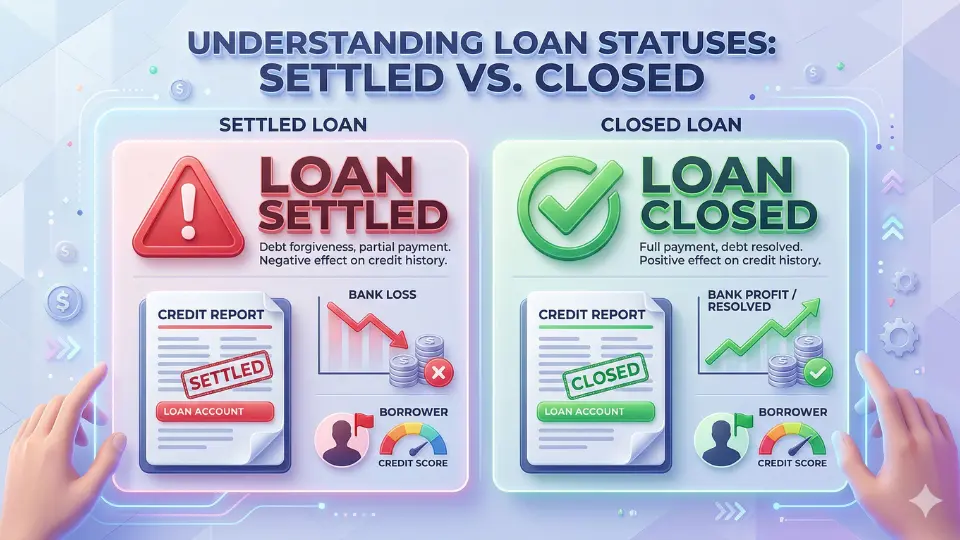

You pay the reduced amount, assuming your debt problems are completely over. However, when you download your latest CIBIL Report, the account status does not say “Closed”—it is permanently marked as “Settled”.

This specific one-word tag is a massive red flag for any financial institution reviewing your profile. It clearly tells future lenders: “This borrower takes money but does not return the full amount, forcing the bank to take a permanent financial loss.”

The Crucial Difference: A “Closed” status means you paid 100% of your principal and interest to the bank. A “Settled” status means the bank accepted a partial payment and wrote off the remaining balance as a complete loss.

According to the official CIBIL website, having a “Settled” remark severely damages your overall creditworthiness. It makes achieving a good CIBIL score in India almost impossible for the next several years.

Major banks like ICICI Bank and Kotak Mahindra Bank routinely reject new credit card and loan applications from individuals with a settlement history. They view you as a high-risk applicant who might easily default on them next.

If a recovery agent is currently pressuring you to compromise on your outstanding dues, you must understand the severe long-term consequences. I strongly suggest reading loan settlement vs loan closure credit report: explore the shocking truths in 25-26 before signing any agreement.

Settled vs. Written-Off Status in CIBIL: Which is Worse?

Borrowers frequently confuse the terms “Settled” and “Written-Off” when evaluating their CIBIL Report and Credit Report parallelly. You must clearly distinguish between these two dangerous tags to protect your long-term financial future.

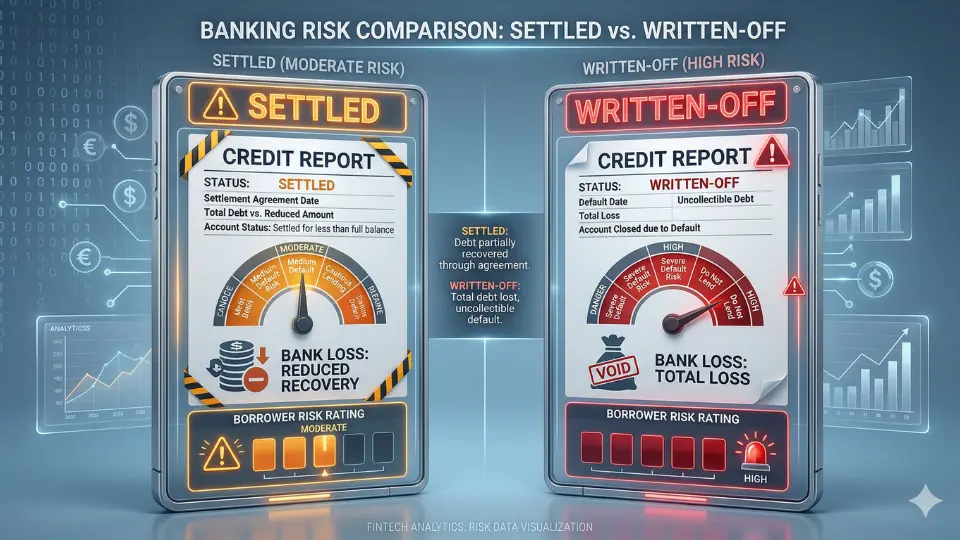

A “Settled” status occurs when you negotiate a mutual compromise with the lender after missing several payments. You pay a reduced, lump-sum amount, and the bank accepts a partial financial loss to close the file.

Conversely, a “Written-Off” status means the bank aggressively tried every method to recover the funds and failed completely. They officially declare a 100% total loss on their balance sheet because you abandoned the debt entirely.

Both of these severe negative remarks instantly destroy your chances of achieving a good CIBIL score in India. However, major banks strictly consider “Written-Off” the absolute worst status a borrower can ever possess.

Lenders like HDFC or ICICI view a settlement as a sign you at least attempted to resolve the issue. A write-off proves to future lenders that you completely walked away from your legal financial obligations.

If a collection agent currently offers you a massive discount, realize that accepting it ruins your profile for years. You must thoroughly explore the harsh realities of loan settlement vs loan closure credit report before signing any agreement.

Here is exactly how the banking system and credit bureaus categorize the fundamental differences between these two outcomes:

| Feature | Settled | Written-Off |

| Bank’s Financial Loss | Partial loss | 100% total loss |

| Borrower Payment | Paid a negotiated, reduced fraction | Paid absolutely nothing |

| Future Loan Chances | Extremely low, heavily scrutinized | Practically zero chance of approval |

| Official Bank View | High-risk borrower | Extreme-risk defaulter |

If you suddenly spot a written-off remark for a forgotten account, act immediately to contact the institution. You must understand how to fix an old loan that suddenly appeared on your CIBIL report to stop the ongoing damage.

According to official RBI guidelines and bank policies, the only way to genuinely repair this damage is full repayment. You must pay the originally waived balance and demand an NOC to finally upgrade your status to “Closed”.

Loan Settlement Impact Calculator

Estimate how a loan settlement today may increase your future loan interest because of a damaged CIBIL profile.

Can You Get a Loan After Settlement?

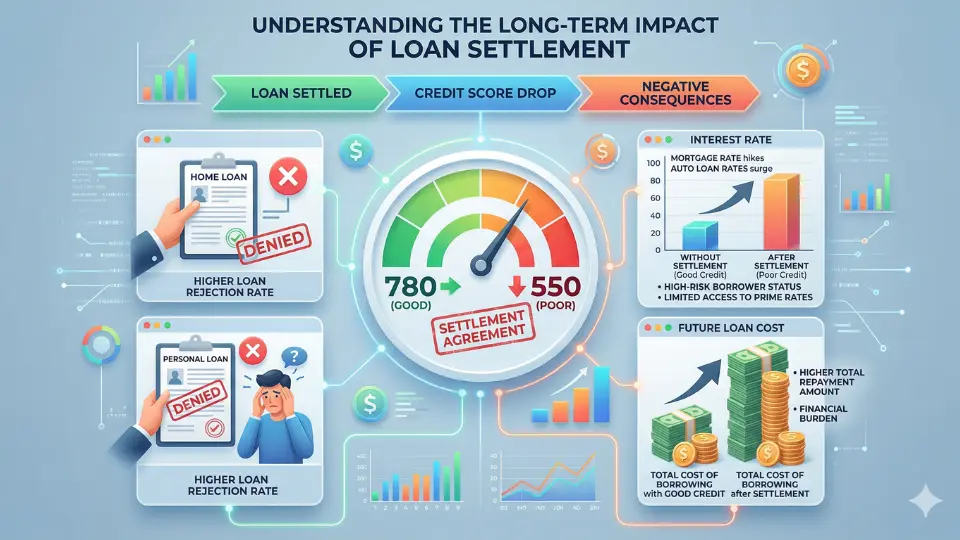

Let us be quite honest about your future borrowing capacity. If your CIBIL Report shows a “Settled” tag from the last five to seven years, top-tier banks like SBI, HDFC, and ICICI will almost instantly reject your new applications.

According to official bank underwriting policies, this specific status marks you as a severe credit risk. Even if your current income is high, major lenders use strict internal filters to immediately block applicants who previously caused a financial loss to any institution.

Does this mean you can never borrow money again? No, you can still secure funds, but usually only through Tier-2 NBFCs or instant digital loan apps.

However, these alternative lenders will offset their risk by charging you a strict “penalty interest rate.” You can expect to pay anywhere from 2% to 5% higher than the normal market average, making your debt incredibly expensive over time.

This single negative remark severely restricts your access to major financial milestones. The following loan types are heavily affected by a settlement history:

- Home Loans: Banks demand absolute long-term repayment stability before approving massive property loans.

- Premium Credit Cards: Unsecured credit lines with high limits are strictly reserved for flawless financial profiles.

- Large Personal Loans: Top lenders will simply not risk high unsecured amounts on past defaulters.

If a top-tier bank recently handed you an outright denial, you must learn exactly what to do after credit card application rejected. Repeatedly applying to different banks will only generate destructive hard inquiries and worsen your situation.

Ultimately, carrying a settlement tag makes it nearly impossible to maintain a good CIBIL score in India. To permanently fix this roadblock, I strongly advise reviewing loan settlement vs loan closure credit report to understand how repaying the waived balance can finally upgrade your status to “Closed”.

Step-by-Step Guide: How to Change Settled Status in CIBIL Online

Step 1: Obtain and Analyze Your Credit Report

Before taking any action, you must know exactly which lender reported the negative remark. According to the official CIBIL website, every Indian citizen is entitled to one free credit report per year.

You must download this document and carefully review the “Account Information” section. Look for the specific loan or credit card number and the bank name that carries the “Settled” tag.

Identifying the exact account is critical because achieving a good CIBIL score in India requires you to fix these specific high-risk remarks. Note down the outstanding amount that was waived off during your previous settlement, as well as the date it was reported.

Step 2: Contact Your Lender to Renegotiate

Your next move is to directly approach the bank that marked your account as settled years ago. You must visit your home branch of SBI, HDFC, ICICI, or the specific NBFC involved.

If branch officials are unhelpful, immediately email their official Nodal Officer or Grievance Redressal Officer. State clearly: “I want to pay the outstanding balance that was previously waived, including any applicable penalties, to convert my account status to ‘Closed’.”

Do not deal with third-party recovery agents for this process, as they often lack the authority to change official credit reporting. The bank will pull up your archived file and calculate the exact amount you still owe them.

This sum represents the actual financial loss they took when you previously compromised on the debt. Negotiating this can be intimidating, but it is the only legal pathway to clear your name.

If you are dealing with aggressive agents over unrelated accounts during this time, review our 5-step action plan stops the calls if a collection agency is calling for a debt that is not yours.

Step 3: Clear the Outstanding Balance in Full

Once the bank calculates your final outstanding balance, you must ask for these exact payment terms in writing. Demand an official email from the bank’s official domain stating that paying this specific amount will permanently change your status to “Closed”.

Never transfer a single rupee based on a verbal promise from a branch manager or customer care executive. Verbal agreements hold zero legal weight if the bank later refuses to update the credit bureaus.

After you receive the official written confirmation, pay the agreed amount in full through a traceable banking channel like NEFT or RTGS. Keep the transaction reference number safely recorded for your final records.

Step 4: Obtain the No Dues Certificate (NOC)

The moment your payment clears the banking system, you must demand a No Dues Certificate (NOC) or No Dues Letter from the lender. Never leave the bank branch or close the email thread without securing this crucial document.

Ensure the certificate explicitly mentions your original loan account number and states that the outstanding balance is strictly zero. This physical piece of paper or official PDF is your only legal proof that you owe the bank absolutely nothing.

It forces the lender to officially acknowledge that the debt is 100% resolved. Unfortunately, some lenders purposely delay issuing this document to former defaulters.

If you face this hurdle, you must learn what to do when a bank is not giving NOC after loan settlement: 2026 legal fix to force their compliance.

Step 5: Raise a Dispute with CIBIL Online

Even after taking your money, banks frequently forget to report the updated “Closed” status to the credit bureaus. You must take matters into your own hands to ensure your profile is actually updated in the national database.

Log in to the official CIBIL dispute portal and initiate a correction request specifically for that targeted account. You will need to upload your newly acquired NOC as hard evidence of your full repayment.

If you are unsure of the exact online process, follow our comprehensive guide on how to dispute errors on your CIBIL report: best step by step guide by Anwar Hashmi. According to RBI guidelines, the bureau and the bank have approximately 30 to 45 days to verify and resolve your dispute.

Once approved, your report will finally reflect a clean “Closed” status. After this 45-day window, pull a fresh report to verify the changes and start rebuilding your creditworthiness from scratch.

Beware of CIBIL Settlement Agencies

Desperate borrowers often fall into dangerous traps when trying to rebuild a good CIBIL score in India. You will likely encounter numerous online advertisements for “credit repair gurus” claiming they can instantly erase your negative history.

You must understand that no third-party agency or private lawyer possesses the power to manipulate the credit bureaus. According to the official CIBIL website, the bureau only accepts and updates financial data directly submitted by registered member banks.

These fake settlement agencies typically demand a massive upfront fee, sometimes around ₹10,000, promising a guaranteed deletion of your “Settled” remark. Once you transfer the funds, they simply disappear, leaving your credit profile just as damaged as before.

⚠️ Fraud Alert: If any company guarantees to remove a legitimate “Settled” or “Written-Off” status from your report for cash, it is a 100% scam. Only your original lender can authorize an official status change after you pay your outstanding dues in full.

Fraudsters routinely exploit desperate individuals who lack proper financial knowledge. To protect yourself from similar financial traps online, you should discover the truth behind the UPI credit line scam: hidden charges and CIBIL impact in 2026.

You must always deal directly with your specific bank’s official branch to resolve any past defaults. Avoid illegal shortcuts, follow the official negotiation process, and safely rebuild your creditworthiness over time.

Key Takeaways

- A “Settled” status in CIBIL means the bank accepted a partial payment and wrote off the remaining balance as a loss.

- This remark severely damages your chances of maintaining a good CIBIL score in India and getting loans from major banks.

- The only legitimate way to remove settled status from CIBIL is by paying the remaining outstanding balance to the lender.

- After repayment, you must obtain a No Dues Certificate (NOC) as legal proof that the debt is cleared.

- If the lender does not update the record automatically, you should raise a dispute on the official CIBIL portal and upload your NOC.

- The correction process generally takes 30 to 45 days, after which your account status should change from Settled to Closed.

- Once corrected, focus on responsible financial habits like on-time payments, low credit utilization, and limited loan inquiries to rebuild your creditworthiness.

Frequently Asked Questions (FAQs)

Is it possible to remove settled status from CIBIL entirely?

Yes, it is entirely possible, but there are absolutely no magic shortcuts or quick fixes. You must pay the originally waived balance in full directly to your respective bank.

Once the lender officially receives this pending payment, they will update your status from “Settled” to “Closed”. If you are unsure about making this financial move, review our detailed breakdown on loan settlement vs loan closure credit report: explore the shocking truths in 25-26.

How long does it take to remove your name from CIBIL settlement?

After you clear your final outstanding dues with the bank, the official reporting process requires patience. According to the official CIBIL website, updating a credit record usually takes between 30 to 45 days.

If the bank fails to notify the bureau within this specific window, your profile will remain damaged. In such cases, you must promptly learn how to dispute errors on your CIBIL report: best step by step guide (25-26) to legally force the correction.

How to remove settled accounts from credit report completely?

You must first contact your lender’s nodal officer and request to pay the exact remaining balance from your past compromise. After making the full payment, you must legally secure your No Dues Certificate (NOC) from the branch.

Keep this document safe, as it is your ultimate proof of zero outstanding debt. Permanently converting these accounts to “Closed” is the only proven, legal pathway to eventually rebuild a good CIBIL score in India.

About the Author

This article is written by Anwar Hashmi, the Chief Editor and lead financial author at Cibilized.in. Translating complex financial jargon into clear, actionable advice is a personal passion of mine.

My mission is to empower everyday borrowers with the exact knowledge needed to take control of their credit health, negotiate with confidence, and achieve lasting financial freedom.

Beyond the digital publishing world, I am deeply committed to grassroots community development. I actively drive education and health initiatives through my local NGO work right here in my hometown of Seohara, Uttar Pradesh.