Understand the joint home loan CIBIL score impact before you co-sign. This guide reveals the hidden risks, ensuring the joint home loan CIBIL score impact is a positive one for all applicants.

Joint Home Loans: Understanding the CIBIL Score Impact for All Applicants

A young couple is trying to buy their first home, but their loan eligibility is falling just short. The bank suggests a simple solution: add a parent with a stable income as a co-applicant. It seems like the perfect fix, but what does this decision truly mean for everyone’s financial future and what is the real joint home loan CIBIL score impact?

While a joint home loan is a powerful tool, its lifelong and often misunderstood consequences for the CIBIL scores of all co-applicants can lead to serious financial issues if not managed correctly. Understanding the full joint home loan CIBIL score impact is a topic filled with myths and half-truths.

My name is Anwar Hashmi, and at cibilized.in, we provide clarity. This guide will be your definitive resource on the joint home loan CIBIL score impact, outlining both the significant benefits and the critical risks you need to be aware of before you sign on the dotted line.

How Lenders Scrutinize All CIBIL Reports in a Joint Loan

When you apply for a joint home loan, the bank’s underwriting process becomes significantly more complex. They don’t just add up your incomes; they merge your financial histories. This means pulling the full CIBIL reports for all co-applicants and scrutinizing them with equal importance. The entire application is often judged by the profile of the “riskiest” applicant, a principle known as the “weakest link.”

The “Weakest Link” Principle Explained

From a bank’s perspective, a joint loan application is only as strong as its weakest co-applicant. If one applicant has a history of missed payments or a low score, it introduces a significant risk to the entire loan, regardless of how pristine the other applicants’ records are. This is why a thorough check of all reports is the first step for any lender.

The Power of a High-Score Co-Applicant

This is the primary reason people opt for a joint loan. By adding a co-applicant with a strong financial profile, you are essentially pooling your creditworthiness. This provides a significant layer of security for the lender, making them more confident in approving the loan.

For instance, if a primary applicant has a score of 720, adding a co-applicant where is 780 a good CIBIL score (yes, it’s considered excellent) can unlock a higher loan amount. The bank sees a household with a proven track record of financial discipline, which directly translates to a lower risk of default and a positive joint home loan CIBIL score impact on the application’s strength.

Hidden Dangers: Why the Full Report Matters

Lenders don’t just look at the three-digit score; they look at the detailed history. A past negative mark on a co-applicant’s report is a major red flag. For example, a previous personal loan where a settlement affects the CIBIL score can seriously jeopardize the entire home loan application. A “Settled” status tells the lender that the co-applicant did not repay their previous debt in full, raising serious questions about their reliability for a new, larger loan.

The Lifelong Connection: A Deep Dive into the Joint Home Loan CIBIL Score Impact

This is the part most people misunderstand. When you co-sign a loan, you are creating a financial link that lasts for the entire tenure, which can be 20 years or more. Understanding the long-term joint home loan CIBIL score impact is non-negotiable.

Shared Record, Shared Responsibility

The home loan account is reflected on the CIBIL reports of all co-applicants. It is not listed as a “primary” or “secondary” account; for credit reporting purposes, every co-applicant is viewed as being equally responsible for the entire loan amount. Think of it like a joint bank account on your credit report; every transaction, good or bad, is visible to both owners and affects both equally. This shared record is the foundation of the joint home loan CIBIL score impact.

The Positive Impact: A Powerful Credit Builder

When managed well, the joint home loan CIBIL score impact is incredibly positive. Consistent, on-time EMI payments act as a strong signal of creditworthiness for everyone involved. For a young co-applicant, it’s an excellent way to build a strong credit history early. For all applicants, successfully managing a large, secured loan diversifies their credit profile, which is a significant long-term positive.

The Critical Negative Impact: One Mistake Affects Everyone

This is the most significant risk. Because every co-applicant is considered equally liable, a single misstep has a cascading negative effect. A single missed EMI on a joint loan will impact the CIBIL score of every single co-applicant negatively. The bank does not care who was responsible for making the payment that month; the CIBIL report will simply show a late payment for everyone. The negative joint home loan CIBIL score impact of a default is severe for all parties.

The Strategic Dilemma: A Pre-Signature Checklist & Analysis

Before you decide to co-sign, it’s essential to analyze the situation from all angles. This involves an honest conversation with all co-applicants and a clear understanding of the pros and cons.

Pre-Signature Checklist for All Co-Applicants

- Full Transparency: Have we shared our complete CIBIL reports with each other? Are there any past issues, like settlements or defaults, that we need to discuss?

- Worst-Case Scenario: Do we have a clear, written plan for who will make the EMI payment if one person faces a job loss, medical emergency, or financial hardship?

- Future Credit Needs: Does any co-applicant plan to take another large loan (like a car loan or business loan) in the next 5-10 years? This joint loan will appear on their credit report and will reduce their future borrowing capacity.

- Financial Discipline: Are we all aligned on the absolute importance of making every single EMI payment on time, without fail? Do we have a shared system for ensuring the payment is made?

A Clear Breakdown: Pros and Cons for Your CIBIL Score

| Pros (The Benefits) | Cons (The Risks) |

| Increased Loan Eligibility: Combining incomes allows you to qualify for a larger loan amount. | Shared Financial Liability: You are legally responsible for the entire loan, even if the other person stops paying. |

| Get Approved with a Lower Score: A co-applicant with a high score can help you get approved. | Your Score is at Risk: Another person’s financial mistake will directly damage your CIBIL score. |

| Builds Credit for All: Timely payments build a strong credit history for every co-applicant. | Reduced Future Eligibility: This loan will appear on your report, reducing your own capacity to take on new loans. |

| Better Interest Rates: A strong combined profile can help you secure a lower interest rate. | Difficult to Exit: The process for removing a co-applicant from a home loan’s CIBIL record is complex. |

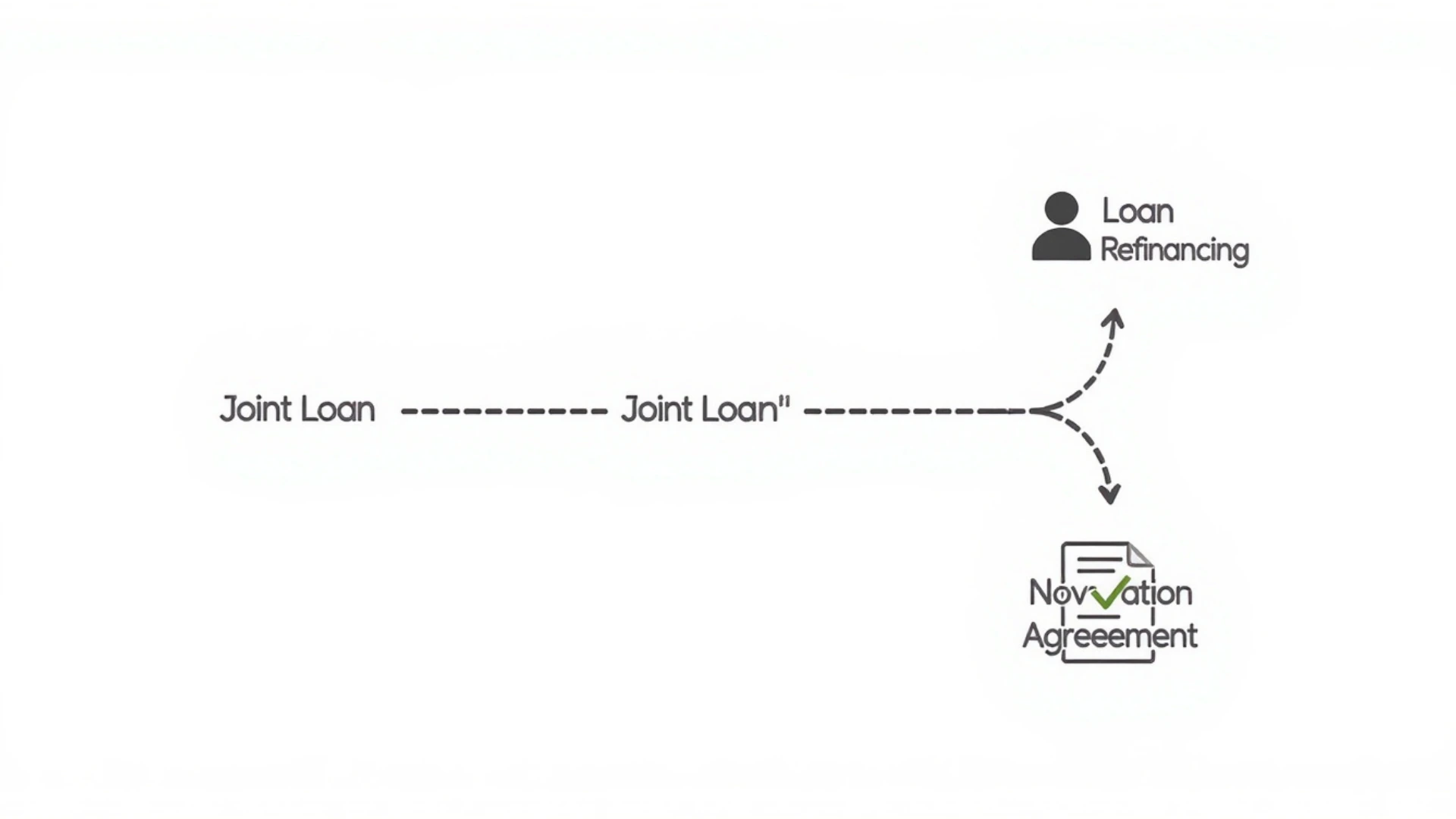

The Exit Strategy: Removing a Co-Applicant From a Home Loan CIBIL Record

Life changes. What happens if a co-applicant needs to be removed due to divorce, financial separation, or other personal reasons? Understanding the exit strategy is crucial.

Method 1: Loan Refinancing

This is the most common method. The primary applicant applies to refinance the home loan in their sole name. This essentially means taking out a brand new loan to pay off the old joint loan. To be approved, the remaining applicant must have a sufficient income and a high enough CIBIL score to qualify for the entire loan amount on their own. They will have to go through the entire application and verification process from scratch.

Method 2: Novation Agreement

This is a formal legal process where you request the bank to create a new contract, releasing one co-applicant from all past and future liability. The remaining applicant assumes full responsibility. This is less common, requires the bank’s explicit consent, and is often harder to get approved than refinancing, as it involves more complex legal paperwork.

Understanding these options is a key part of managing the long-term joint home loan CIBIL score impact.

[Image Suggestion: A simple graphic showing two paths diverging from one, one labeled “Refinance” and the other “Novation Agreement.” Alt Text: An infographic showing the two main exit strategies for a joint home loan.]

Conclusion

A joint home loan is a powerful financial tool, but the joint home loan CIBIL score impact is a significant, long-term commitment that intertwines the financial fates of all co-applicants. It can be incredibly positive, building a strong credit history for everyone, but the risks are equally significant.

Before you co-sign, have an open and honest conversation about financial discipline. It’s a decision based not just on income, but on mutual trust and a shared commitment to managing the joint home loan CIBIL score impact responsibly.

What is the most significant joint home loan CIBIL score impact I should be aware of?

The most significant joint home loan CIBIL score impact is the concept of shared liability. A single missed or late EMI payment by any co-applicant will negatively affect the CIBIL score of every person on the loan agreement equally. This shared risk is the most critical joint home loan CIBIL score impact to consider before co-signing.

2. How much does a co-applicant’s CIBIL score matter for a joint home loan?

A co-applicant’s CIBIL score matters immensely; it can make or break your application. Lenders assess all applicants’ reports, and if a co-applicant has a low score or a history of defaults, it can lead to rejection, even if the primary applicant’s score is high. Therefore, ensuring every co-applicant’s CIBIL score matters and is in good standing is crucial for approval.

3. What is the minimum CIBIL score requirement for a joint home loan?

While the exact CIBIL score requirement for a joint home loan varies by lender, most banks prefer to see all applicants with a score of 750 or above. If you ask, “is 780 a good CIBIL score for this?” the answer is yes, a score of 780 is considered excellent and will significantly strengthen your joint application, helping you meet the lender’s CIBIL score requirement for a joint home loan.

4. What is the missed EMI on a joint loan impact for all co-applicants?

The missed EMI on a joint loan impact is severe and equal for all co-applicants. CIBIL does not differentiate who was responsible for the payment. A late payment will be reported on every co-applicant’s credit history, leading to a significant drop in their individual CIBIL scores and affecting their future borrowing capacity.

5. How does a past settlement affect the CIBIL score of a co-applicant?

A past settlement has a significant negative effect on a CIBIL score and can be a major red flag for lenders reviewing a joint home loan application. When a lender sees that a settlement affects the CIBIL score, it indicates the co-applicant did not repay a previous loan in full. This past credit behavior can lead to higher interest rates or even rejection of the entire joint application.

6. What are the main pros and cons of a joint home loan for my CIBIL?

The main pros and cons of a joint home loan for your CIBIL are dual-sided. The biggest pro is that timely payments build a strong credit history for all co-applicants. The biggest con is that one person’s financial mistake becomes everyone’s negative CIBIL event, making the pros and cons of a joint home loan for CIBIL a matter of shared risk versus shared reward.

7. Is removing a co-applicant from a home loan’s CIBIL report a simple process?

No, the process for removing a co-applicant from a home loan’s CIBIL record is very complex and is not guaranteed. It typically requires refinancing the entire loan in a single name, which means the remaining applicant must qualify for the full loan amount on their own. Successfully removing a co-applicant from a home loan’s CIBIL report requires the full consent and cooperation of the bank.

8. In summary, how does a joint home loan affect your credit score long-term?

Ultimately, how a joint home loan affects your credit score depends entirely on payment discipline. If all EMIs are paid on time, it acts as a powerful, long-term credit builder for everyone involved. If payments are missed, it becomes a long-term negative mark on everyone’s report, demonstrating precisely how a joint home loan affects your credit score through shared responsibility.

Author:

Anwar Hashmi is a financial writer and the founder of cibilized.in. He excels at demystifying complex financial systems, providing expert, data-driven guides on the Indian CIBIL score. As the lead author for ClaimCredits.online, he also specializes in U.S. tax credits, bringing a breadth of international financial expertise to his readers.

Pingback: CIBIL Score for Home Loan: 7 Tips to Get Approved Faster. - CIBILized