A missed first credit card payment is scary. This guide reveals your 3-step emergency action plan for what to do after a missed first credit card payment to protect your CIBIL score.

You just realized you missed the due date on your very first credit card bill. Your heart sinks. You’re flooded with questions: “Have I ruined my CIBIL score forever? Will I be charged a huge penalty?” The anxiety of a missed first credit card payment can be overwhelming.

Take a deep breath. This is a very common mistake, and the good news is, it is fixable. I’ve spoken with countless young professionals who have been in this exact situation. The feeling of making a missed first credit card payment is a terrible one, but it is not the end of your financial journey.

What This Emergency Guide Will Do For You

My name is Anwar Hashmi, and at cibilized.in, my mission is to replace that panic with a calm, clear-headed action plan. This guide will show you the three immediate steps to take right now to minimize the damage to your wallet and your CIBIL score.

This is your emergency plan for a missed first credit card payment. We will turn this moment of panic into a powerful learning experience that will make you a more confident and responsible credit user for life. This guide will show you that a missed first credit card payment is a problem with a solution.

Table of Contents

The Immediate Aftermath: Understanding the Two Penalties

The moment you realize you’ve missed first credit card payment, a wave of panic can set in. Your mind starts racing with worst-case scenarios. It’s a stressful situation, but the first step to taking control is to understand exactly what happens next.

When you miss a due date, the bank’s automated systems trigger two distinct penalties. One affects your wallet immediately, while the other can have a longer-lasting impact on your financial future. Understanding these two consequences is a critical part of knowing what to do after you’ve missed first credit card payment.

Penalty #1: The Late Payment Fee

This is the most immediate and visible penalty. A “Late Payment Fee” is a fixed charge that the bank levies as a penalty for failing to pay at least the Minimum Amount Due by the specified Due Date.

How it’s Calculated

This fee is not a random amount. According to guidelines from the Reserve Bank of India (RBI), late payment fees are charged on a tiered basis, based on your total outstanding balance. While the exact numbers can vary slightly from bank to bank, a typical structure might look like this:

| Total Outstanding Balance | Typical Late Payment Fee |

| Less than ₹500 | ₹0 |

| ₹501 to ₹1,000 | ₹100 |

| ₹1,001 to ₹10,000 | ₹500 |

| More than ₹10,000 | up to ₹1,300 |

This means that a missed first credit card payment on a large bill can instantly cost you over a thousand rupees. This fee will be automatically added to your next month’s credit card statement.

Penalty #2: The Interest Charges (The Hidden Trap)

This second penalty is far more costly and is the one that traps most new credit card users in a cycle of debt. It’s a critical concept to understand, especially after a missed first credit card payment.

The Loss of Your “Interest-Free Grace Period”

Every credit card in India comes with an “interest-free grace period,” which is typically 20-50 days. This means that if you pay your entire bill (the “Total Amount Due”) by the Due Date, you are not charged any interest on your purchases. This is the biggest benefit of a credit card.

However, the moment you fail to pay the full amount by the due date—which is what happens when you’ve missed first credit card payment—you lose this grace period.

How the Interest Trap Works

Once the grace period is lost, two things happen immediately:

- Interest on the Old Balance: The bank starts charging you a very high interest rate (often 3-4% per month, which is over 40% per year) on your entire outstanding balance from the date of each transaction.

- Interest on New Purchases: This is the most dangerous part. All your new purchases for the next billing cycle will start accruing interest from the very day you make them. There is no grace period at all.

This system of daily compounding interest can cause your debt to snowball very quickly. If left unchecked, this can lead to a situation where a loan settlement becomes the only option, which is far more damaging to your Credit Report.

You will only get your interest-free grace period back after you have paid the entire outstanding balance down to zero. The financial cost of a missed first credit card payment is often far greater than just the initial late fee.

Your 3-Step Emergency Action Plan (To Be Done Today)

You’ve understood the penalties. Now is the time for calm, decisive action. The steps you take in the next 24 hours can make a massive difference in minimizing the financial damage and protecting your CIBIL score.

This is not a time for panic or procrastination. This is your emergency action plan. I’ve used this exact framework to guide countless individuals through the stress of a missed first credit card payment. Follow these three steps today.

Step 1: Pay the Bill Immediately

Your first and most urgent task is to pay your credit card bill. Do not wait for your next salary or for a reminder from the bank. Log in to your net banking or mobile app and make the payment right now.

Crucially, you should pay the “Total Amount Due,” not just the “Minimum Amount Due.” Paying the full amount is the only way to stop the high-interest clock from ticking on your old balance and to restore your interest-free grace period for the next billing cycle. This is the most important step to take after you’ve missed your first credit card payment.

By clearing the entire balance, you are drawing a line in the sand and preventing the debt from spiraling. It’s a powerful first step in recovering from a missed first credit card payment.

Step 2: The “Goodwill Reversal” Phone Call

This is an expert-level secret that most new credit card users don’t know about. It is the single most powerful tool you have to reverse the financial penalty of your mistake. Banks want to build a long-term, profitable relationship with you, and they understand that good customers sometimes make a single, honest mistake.

A “goodwill reversal” is when you politely request the bank to waive your late payment fee as a gesture of goodwill. This is especially effective after you’ve missed first credit card payment, as the bank is often more lenient with new customers.

The Script: How to Politely Request a Late Fee Waiver

After you have paid the full amount, call your bank’s customer service helpline. Be polite, calm, and confident. Use the following script as your guide:

“Hello, my name is Anwar Hashmi. I’m calling about a late payment fee that I expect will be on my next statement for my credit card ending in [Last 4 Digits]. As this is my first credit card and my very first time ever missing a payment, I would like to request a one-time ‘goodwill reversal’ of this fee. I have already paid the full balance now.”

Why This Works: The Psychology of Customer Retention

This script is effective because it is not a demand; it is a polite request that highlights several key psychological triggers:

- You Acknowledge Your Mistake: You are not making excuses.

- You Highlight Your Value: You mention it’s your “very first time,” signaling that this is an exception, not a pattern.

- You’ve Already Fixed the Problem: By stating, “I have already paid the full balance now,” you show that you are a responsible customer.

Banks know that the cost of acquiring a new customer is very high. They would rather waive a ₹500 fee than lose a potentially valuable customer over their very first mistake. This is a crucial strategy to know after you’ve missed first credit card payment.

Step 3: Set Up a Foolproof System for the Future

The final step is to ensure this mistake never happens again. A single missed first credit card payment is a lesson; a second one is the beginning of a negative pattern that can seriously damage your CIBIL score. The key is to remove willpower and forgetfulness from the equation by creating an automated system.

Your Foolproof Payment System Checklist:

- [ ] Set Up Auto-Pay for the Minimum: Log in to your net banking portal and set up a standing instruction to automatically pay the “Minimum Amount Due” from your savings account 2-3 days before the due date. This is your ultimate safety net.

- [ ] Set a Calendar Reminder for the Full Amount: Create a recurring monthly event in your phone’s calendar for 3-4 days before your due date. Title it “Pay Full Credit Card Bill.” This alert will prompt you to manually pay the remaining balance to avoid interest charges. For an even more powerful strategy to manage your credit profile, many experts also pay their credit card bill before the statement date to lower their reported utilization.

By implementing this 3-step plan, you have successfully navigated the crisis of a missed first credit card payment. You’ve minimized the financial damage, and you’ve built a system to ensure it won’t happen again. This is how you turn a missed first credit card payment from a moment of panic into a powerful financial lesson.

The Long-Term Question: Will One Late Payment Affect My CIBIL Score?

You’ve completed the emergency action plan. You’ve paid the bill and spoken with the bank. Now, the biggest question remains, the one that causes the most anxiety: “Have I permanently damaged my CIBIL score?”

The answer, thankfully, is more nuanced than a simple “yes” or “no.” The real impact of your missed first credit card payment depends entirely on how late your payment was. Understanding this distinction is the key to assessing the long-term consequences and planning your recovery.

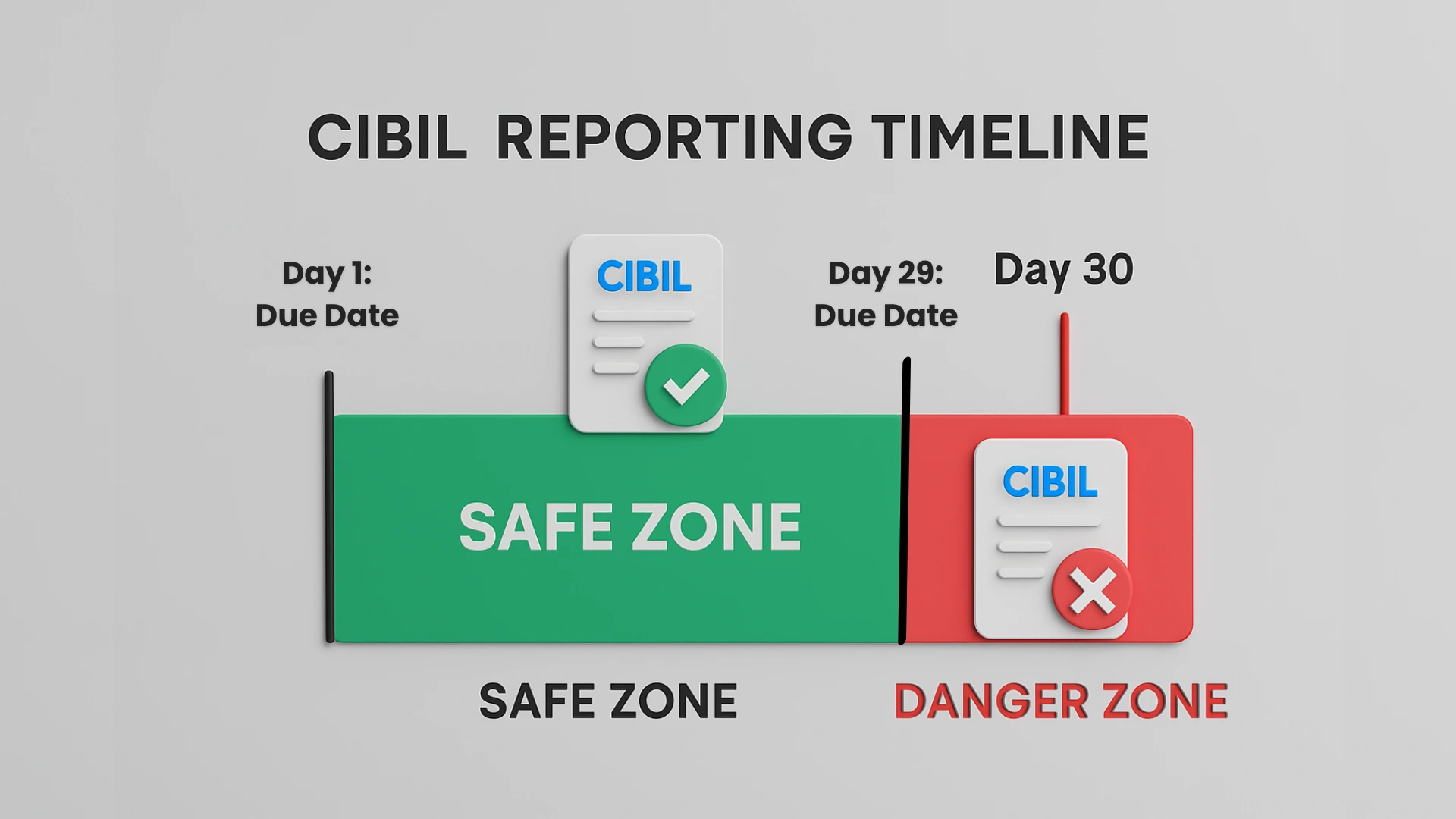

The “30-Day” Rule Explained

This is the most important rule in the world of credit reporting that you need to know right now. While your bank considers your payment “late” the day after the due date and charges you a fee, they typically do not report this negative information to the credit bureaus like CIBIL immediately.

Based on the standard reporting practices of most major banks in India, a payment is usually only reported as “late” or “overdue” to CIBIL after it has been overdue for more than 30 days.

This 30-day buffer is a critical grace period. It means that how you react after a missed first credit card payment can make all the difference between a minor financial inconvenience and a long-term credit score problem.

A “Before 30 Days” vs. “After 30 Days” Scenario

Let’s break down the two possible scenarios to see how this rule affects you directly. This will help you understand the true impact of your missed first credit card payment.

Scenario 1: You Paid Within a Few Days (Before the 30-Day Mark)

This is the best-case scenario and the most common one for responsible new credit users. You missed the due date, but you realized your mistake a few days later and immediately paid the full amount, as outlined in our emergency action plan.

In this situation, you can breathe a huge sigh of relief. Because the payment was not overdue for more than 30 days, it is highly unlikely that the bank will report any negative information to CIBIL.

- What Happens to Your CIBIL Report: Nothing. The payment will simply be reflected as “Paid” in the next reporting cycle. There will be no “DPD” (Days Past Due) mark on your Credit Report.

- The Bottom Line: You will have paid a late fee and some interest (which you should try to get reversed), but your CIBIL score will be completely unharmed. For your credit history, it’s as if the missed first credit card payment never happened. This is why acting fast is so critical after a missed first credit card payment.

Scenario 2: Your Payment Was More Than 30 Days Late

This is a more serious situation. If, for any reason, you were unable to make a payment for more than 30 days after the due date, the bank will report this negative event to CIBIL.

- What Happens to Your CIBIL Report: A “DPD” mark of “030” (or “060” if it was 60 days late) will be added to your payment history for that account. This negative mark will remain on your Credit Report for up to seven years.

- The Score Drop: Yes, your CIBIL score will drop. A single 30-day late payment can cause a significant drop, sometimes by as much as 50-80 points, especially if you have a new or “thin” credit file. This is the unfortunate consequence of a missed first credit card payment that crosses the 30-day threshold.

However, this is not a catastrophe. A single late payment is a serious mistake, but it is not an unrecoverable one. Lenders are more concerned with a pattern of late payments than a single, isolated incident from your past.

Your recovery plan is simple: from this point forward, you must build a long and flawless track record of on-time payments. After 6-12 months of perfect payments, the negative impact of that one missed first credit card payment will begin to fade, and your score will start to recover. Lenders will see that your missed first credit card payment was an exception, not the rule.

Frequently Asked Questions About a Missed First Credit Card Payment

1. What are the immediate consequences of missing the first credit card payment?

The main consequences of missing the first credit card payment are a late payment fee and high interest charges that start accruing immediately. The long-term consequences of missing the first credit card payment can include a lower CIBIL score if the payment is over 30 days late.

2. I missed my credit card payment by one day in India, will it be reported to CIBIL?

If you missed your credit card payment by one day in India, it is highly unlikely to be reported to CIBIL. Banks usually have a grace period and only report payments that are over 30 days late, so even if you missed your credit card payment by one day in India, paying it immediately should protect your score.

3. Will a single missed first credit card payment ruin my CIBIL score forever?

No, a single missed first credit card payment will not ruin your score forever. While a reported missed first credit card payment can cause a significant score drop, the damage is not permanent and can be overcome with 6-12 months of consistent, perfect payments going forward.

4. What is a goodwill reversal and how does it help?

A goodwill reversal is when a bank agrees to waive a charge, like a late fee, for a good customer as a gesture of goodwill. You can often request a goodwill reversal for your first late fee, which can save you a significant amount of money.

5. How do I ask for a late payment fee to be waived for the first time?

To get a late payment fee waived for the first time, you should call your bank’s customer care, politely state that it’s your very first mistake, and request a goodwill reversal. Getting a late payment fee waived for the first time is often successful for new customers with an otherwise clean record.

6. What is the biggest fear after a missed first credit card payment?

The biggest fear after a missed first credit card payment is a permanent, damaging mark on one’s CIBIL report. However, the good news is that if you pay the bill within 30 days of the due date, a missed first credit card payment is highly unlikely to be reported to the credit bureaus at all.

7. How does the credit reporting 30-day rule work in India?

The 30-day rule is an industry standard where banks typically only report a payment as “late” to CIBIL after it has been overdue for more than 30 days. This 30-day rule acts as a crucial grace period that can protect your CIBIL score from a single, quickly corrected mistake.

8. Will a late payment show up on my main Credit Report?

A late payment will only show up on your Credit Report if it is more than 30 days overdue. A clean Credit Report is your goal, so paying promptly within this 30-day window is critical to prevent any negative marks from appearing.

9. What is the first thing to do after a missed first credit card payment?

The absolute first thing to do after a missed first credit card payment is to pay the “Total Amount Due” immediately, not just the minimum. A fast response to a missed first credit card payment stops high-interest charges from accumulating and is the best way to prevent CIBIL reporting.

10. What are interest charges on a credit card bill?

Interest charges (or finance charges) are the fees applied to your outstanding balance when you don’t pay it in full by the due date. After a missed payment, these interest charges can accrue daily at a very high rate, making your debt grow quickly.

11. What is the typical late payment fee in India?

The late payment fee in India is usually charged on a tiered basis depending on your outstanding balance, often ranging from ₹100 to ₹1,300. This is why it’s so important to have a strategy to avoid a late payment fee by always paying on time.

12. Will one late payment affect my CIBIL score significantly?

Yes, one late payment can affect your CIBIL score significantly if it is reported (i.e., over 30 days late), potentially dropping it by 50-80 points. The impact of one late payment on your CIBIL score will diminish over time with a new history of good behavior.

13. How does a bank view a missed first credit card payment?

Banks are often more lenient with a missed first credit card payment, viewing it as a learning opportunity for a new customer, which is why a goodwill reversal for the fee is often granted. However, a pattern of late payments after the missed first credit card payment is viewed very negatively.

14. What is the first time credit card late payment CIBIL impact for a student?

The first time credit card late payment CIBIL impact can be quite significant for a student who has a “thin” credit file with very little history. For a new borrower, a first time credit card late payment CIBIL impact is a major negative mark that can make it harder to get future loans.

15. Does a late payment affect my score on Experian and other credit bureaus?

Yes, when a bank reports a late payment, they send that information to all four credit bureaus in India (CIBIL, Experian, Equifax, CRIF High Mark). The negative mark will appear on all your credit reports and affect your scores from all the credit bureaus.

16. What is the long-term CIBIL impact of a missed first credit card payment?

The long-term CIBIL impact of a missed first credit card payment depends entirely on how late it was. If it was over 30 days late, the negative mark from the missed first credit card payment can stay on your report for up to 7 years, but its impact on your score will fade with a new, consistent history of on-time payments.

From Your First Mistake to Your First Lesson

That moment of panic after you’ve missed your first credit card payment can feel overwhelming, but it is not a permanent failure. As this guide has shown, if you act quickly and strategically, the damage can be minimal or even completely avoided.

The most important takeaway is to reframe this event. A missed first credit card payment is not a catastrophe; it is a critical learning opportunity. It is your first real-world lesson in the importance of due dates, the power of a goodwill reversal, and the necessity of creating a foolproof payment system. You now have the knowledge and the action plan to ensure this mistake never happens again.

Now that you’ve handled this crisis, it’s time to build a strong foundation for the future. For a complete masterclass on all the strategies to build a high score, from mastering your payment history to advanced utilization hacks, our main pillar post, The Ultimate Guide to Improving Your CIBIL Score, provides a comprehensive, step-by-step plan.

Author’s Note

A Note from the Author: The feeling of a missed first credit card payment is a universal moment of panic. I wrote this guide to give you a calm, clear, and immediate action plan to turn that moment of stress into a powerful financial lesson.

- Anwar Hashmi, founder of

cibilized.in. For expertise on American finance, he is also the lead author atClaimCredits.online, specializing in USA Tax Credits.