Discover why you should pay credit card bill before the statement date to boost your CIBIL score. Learn the secret of how to pay credit card bill before the statement date for maximum impact.

You just paid your ₹50,000 credit card bill down to zero, on time. You feel financially responsible. But when you check your CIBIL report, it shows you have a high balance and your score hasn’t budged. What’s going on?

This is a deeply frustrating situation I hear about all the time. The problem isn’t that you paid, but when you paid. The secret to mastering your score lies in understanding the critical, misunderstood difference between the “Statement Date” and the “Due Date.”

My name is Anwar Hashmi, and at cibilized.in, my mission is to give you that clarity. This guide is a complete masterclass on the ‘Pay Before Statement Date’ hack, a powerful tactic within the broader strategy of how to improve your CIBIL score.

By the end, you will understand how to strategically time your payments to ensure a lower balance is always reported to CIBIL. This is the expert’s secret for how to pay credit card bill before the statement date effectively.

Statement Date vs. Due Date: The Most Important Secret on Your Bill

To truly master your CIBIL score, you must understand a secret that separates amateur credit users from the pros. This secret is hidden in plain sight on every credit card bill you receive: the critical difference between your “Due Date” and your “Statement Date.”

For years, I’ve seen people focus entirely on one of these dates while completely ignoring the other, and it’s the primary reason their scores stagnate despite paying on time. Grasping this concept is the foundation of learning how to pay credit card bill before the statement date effectively.

The “Due Date”: What 99% of People Focus On

The “Due Date” is the one we all know. It is the final deadline that the bank gives you to pay at least the minimum amount due for your billing cycle.

Its role is simple and singular: it governs your Payment History. As long as you pay the minimum amount before this date, you will avoid late fees and a negative mark. This is critical, as failing to do so can eventually lead to a loan settlement, which is far more damaging to your Credit Report.

The “Statement Date”: The Secret CIBIL Reporting Date

The “Statement Date,” often called the “Billing Date,” is the most overlooked but most powerful date on your bill. This is the day the bank “closes the books” on your monthly spending and generates your bill.

Crucially, the outstanding balance on your card on this specific date is the exact number that gets reported to the credit bureaus like CIBIL. This reported balance is what is used to calculate your Credit Utilization Ratio (CUR), the second most important factor in your score.

This is why the strategy to pay credit card bill before the statement date is a game-changing hack. By making a payment before this date, you can strategically lower the balance that CIBIL ever gets to see, directly and positively influencing your score. Learning how to pay credit card bill before the statement date is about controlling the data that gets reported about you.

A Clear Comparison

Let’s put them side-by-side to make the distinction crystal clear. This is the core of understanding how to pay credit card bill before the statement date.

| Date Type | What It Is | Impact on You |

| Statement Date | The date your monthly bill is generated. | Directly impacts your CIBIL score by setting the balance used for your Credit Utilization Ratio. |

| Due Date | The final deadline to pay your bill. | Directly impacts your payment history. Missing this date results in a negative “late payment” mark. |

As you can see, both dates are important, but they affect completely different parts of your CIBIL report. While paying before the due date keeps you from getting a negative mark, the secret to proactively boosting your score is to pay credit card bill before the statement date. This is the professional’s approach to mastering credit, and it’s a key tactic in any serious plan for how to pay credit card bill before the statement date.

The “Mid-Cycle Payment” Hack: Your Step-by-Step Strategy

Now that you understand the critical difference between your Statement Date and your Due Date, you have the knowledge to unlock an expert-level strategy. This is a powerful technique that I personally use to maintain a high CIBIL score.

This “hack” is known as making a “mid-cycle payment,” and it is the most practical and effective way to implement the strategy to pay credit card bill before the statement date. It allows you to control the exact balance that gets reported to the credit bureaus, giving you a direct lever to pull to boost your score.

The Core Principle: Lowering Your Reported Balance

The core principle is simple: you are making a payment before the bank finalizes your monthly bill. By doing this, you are strategically reducing the outstanding balance that appears on your statement. Since this statement balance is the number reported to CIBIL, you are ensuring that a much lower, healthier Credit Utilization Ratio (CUR) is recorded for that month.

Let’s walk through a clear, step-by-step example.

- You have a credit card with a ₹1,00,000 limit. Your statement date is the 15th of every month.

- On the 5th of the month, you make a large, necessary purchase of ₹40,000. Your current balance is now ₹40,000.

- If you do nothing, on the 15th, the bank will generate a statement with a ₹40,000 balance and report a 40% CUR to CIBIL, which is in the “Fair” or “Average” risk zone.

- However, you are a smart credit user. On the 13th of the month (two days before your statement date), you log in to your net banking and make a manual, mid-cycle payment of ₹30,000.

- On the 15th, when the bank generates your statement, your outstanding balance is now only ₹10,000.

- The bank reports this new, lower balance to CIBIL. Your CUR for that month is recorded as a very healthy 10%.

By taking one simple action, you have completely changed the story that gets told to the credit bureaus. This proactive management is especially critical in the months before you apply for a major loan, as it can significantly strengthen your CIBIL score for a home loan. This is the power of knowing how to pay credit card bill before the statement date.

Your Action Plan Checklist

Putting this strategy into practice is simple. It just requires a small change to your financial routine. This checklist is your guide to making this powerful habit a part of your life.

- [ ] Find Your Statement Dates: Log in to all your credit card accounts and find the statement generation date for each one. Write them down.

- [ ] Set Your Reminders: Go into your phone’s calendar and create a recurring monthly reminder for 2-3 days before each statement date. Label it “CIBIL Score Boost Payment.”

- [ ] Make the Mid-Cycle Payment: On your reminder day, log in and make a payment. You don’t have to pay the full amount, just enough to bring your balance well below the 30% utilization mark.

- [ ] Pay the Remainder by the Due Date: Remember to pay the remaining small balance on your statement before the final due date to maintain your perfect payment history.

This simple, proactive checklist is the most effective framework for how to pay credit card bill before the statement date. This small habit is a key differentiator between a good score and an excellent one.

For anyone serious about their credit health, learning how to pay credit card bill before the statement date is a non-negotiable skill. Consistently making the choice to pay credit card bill before the statement date is what builds a truly exceptional CIBIL score.

Advanced Application: Combining the Hack with the Individual Card Utilization Rule

Now that you have mastered the “Mid-Cycle Payment” hack, it’s time to apply it with the precision of a financial expert. To do this, we need to understand a crucial nuance that most people miss: CIBIL and other credit bureaus analyze not just your overall credit utilization, but also the utilization on each individual credit card.

This is a critical piece of the puzzle. You might think you’re safe because your overall utilization is low, but one maxed-out card can still act as a major red flag, pulling your score down. Understanding this is key to getting the most benefit when you pay credit card bill before the statement date.

Why This Hack is a Superpower for Your Most-Used Card

Think about how you use your cards. Most of us have one primary “go-to” card that we use for almost everything—online shopping, groceries, fuel—to maximize reward points. We might have other cards that we barely use, keeping them for emergencies.

This common behaviour can create a hidden problem. Even if your total spending is low, concentrating it all on one card can push its individual utilization ratio dangerously high. A lender seeing one card at 90% utilization might see you as a risk, even if your other cards are at 0%.

This is where our strategy becomes a superpower. By learning how to pay credit card bill before the statement date, you can specifically target your most-used card, neutralize its high utilization, and present a perfectly balanced and responsible credit profile to the bureaus every single month. This level of proactive management, similar to understanding how to remove a hard inquiry from your CIBIL report, is what separates a good score from a great one.

A Strategic Case Study: Priya’s Story

Let’s look at a real-world example. Meet Priya, a marketing manager who is diligently trying to improve her CIBIL score. She has a good understanding of the basics and always pays her bills on time.

Priya’s Credit Profile:

- Card 1 (ICICI Amazon Pay): This is her primary card.

- Credit Limit: ₹50,000

- Typical Monthly Balance: ₹45,000 (She uses it for everything and pays it off in full).

- Card 2 (SBI SimplyCLICK): Her older, secondary card.

- Credit Limit: ₹1,00,000

- Typical Monthly Balance: ₹5,000

Let’s analyze her situation before she learns our hack.

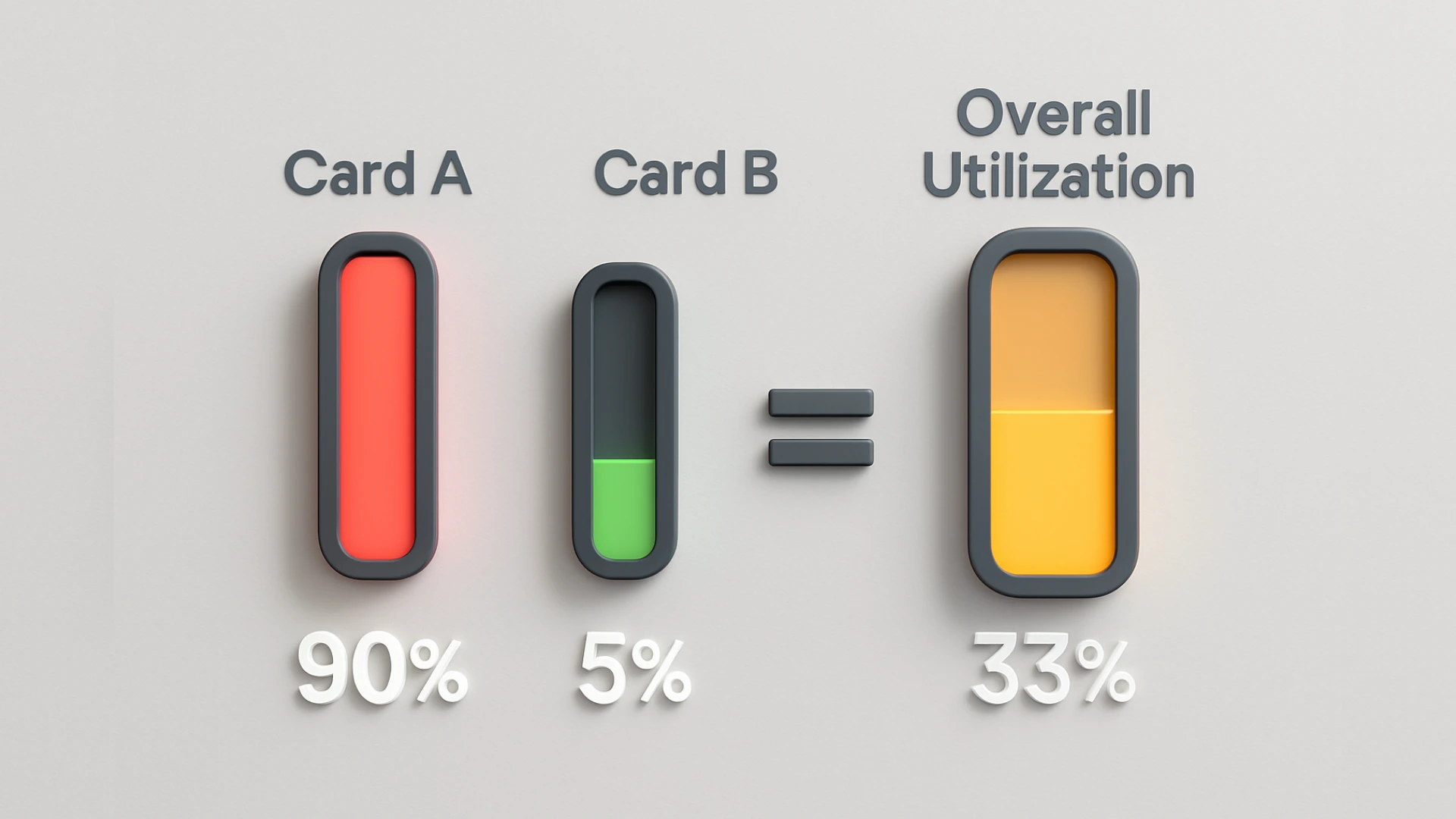

| Credit Card | Balance | Limit | Individual CUR |

| ICICI Amazon Pay | ₹45,000 | ₹50,000 | 90% (High Risk) |

| SBI SimplyCLICK | ₹5,000 | ₹1,00,000 | 5% (Excellent) |

| Overall | ₹50,000 | ₹1,50,000 | 33.3% (Borderline) |

Priya is frustrated. Her overall utilization is just over the 30% mark, but her score isn’t improving as fast as she’d like. The problem is her ICICI card. The 90% individual utilization is a massive red flag that is holding her back.

Then, Priya learns the secret: pay credit card bill before the statement date.

Priya’s New Action Plan:

- She finds that the statement date for her ICICI card is the 18th of each month.

- She sets a recurring calendar reminder for the 16th of every month.

- On the 16th, she logs in and makes a manual, mid-cycle payment of ₹40,000 to her ICICI card.

- The bank now generates her statement with a balance of only ₹5,000.

Let’s look at her new, reported credit profile.

| Credit Card | Reported Balance | Limit | Individual CUR |

| ICICI Amazon Pay | ₹5,000 | ₹50,000 | 10% (Excellent) |

| SBI SimplyCLICK | ₹5,000 | ₹1,00,000 | 5% (Excellent) |

| Overall | ₹10,000 | ₹1,50,000 | 6.6% (Excellent) |

The transformation is stunning. Even though Priya’s total monthly spending has not changed at all, her reported credit profile has gone from “borderline” to “excellent.” She has taken complete control of the data being sent to CIBIL.

This case study is the perfect illustration of why learning how to pay credit card bill before the statement date is a critical skill. By making the choice to pay her credit card bill before the statement date, she has fixed her biggest problem without altering her lifestyle.

This is the strategic way to pay credit card bill before the statement date for maximum CIBIL score impact.

From Reactive Payer to Proactive Planner

The journey to a high CIBIL score is built on a series of small, intelligent habits, and the one we’ve discussed today is perhaps the most powerful. For years, most of us have been conditioned to focus solely on the “Due Date.” We’ve operated in a reactive mode, waiting for the bill to arrive and then paying it.

The secret you have now learned is that the real power lies with the “Statement Date.” By understanding this critical distinction, you fundamentally change your relationship with your credit card. You are no longer just a consumer; you are a strategic financial planner. This is the core of the strategy to pay credit card bill before the statement date.

This single shift in timing—from paying after the bill is generated to paying before—transforms you from a reactive payer into a proactive credit manager. You are now in control of the exact data that gets sent to your Credit Report every month. You are telling the story you want to be told.

Mastering your utilization by learning how to pay credit card bill before the statement date is a key part of a bigger picture. To understand all the factors that contribute to an excellent score and to build a complete, long-term strategy, it’s essential to zoom out and look at your entire credit profile.

For those ready to explore the complete framework, from mastering on-time payments to leveraging advanced tactics, our main pillar post, the Ultimate Guide to Improving Your CIBIL Score, provides a comprehensive, step-by-step plan.

Frequently Asked Questions About Credit Card Payments & Your CIBIL Score

1. What is the most important difference between the statement date vs due date on my bill?

The most important difference is their impact on your CIBIL score. The statement date vs due date distinction is crucial: the statement date determines the balance reported for your utilization ratio, while the due date determines if your payment is marked as “on-time.” Understanding the statement date vs due date is key to proactive credit management.

2. Is there a specific strategy for how to pay credit card bill before the statement date for the best results?

Yes, the best strategy for how to pay credit card bill before the statement date is to make a “mid-cycle” payment 2-3 days before your statement is generated. This simple plan for how to pay your credit card bill before the statement date ensures the lowest possible balance is reported to CIBIL.

3. Will my CIBIL score really increase just by changing my payment date?

Yes, it can. While your payment history remains the most important factor, your CIBIL score is also heavily influenced by your Credit Utilization Ratio. By strategically timing your payments, you directly and positively influence this ratio, which can lead to a noticeable increase in your CIBIL score.

4. What is the main benefit if I pay my credit card bill before the statement date?

The main benefit is significantly lowering your reported Credit Utilization Ratio (CUR). When you pay your credit card bill before the statement date, you ensure a smaller balance is sent to CIBIL. This is a powerful reason to pay credit card bill before the statement date for a faster score boost.

5. How much of my balance should I clear before the statement date for the best Credit Utilization Ratio?

For the best Credit Utilization Ratio, you should aim to pay your balance down to below 30% of your credit limit. Ideally, for the most powerful positive signal, a Credit Utilization Ratio below 10% is considered excellent by lenders.

6. Does the advice to pay credit card bill before the statement date apply to all banks in India?

Yes, this is a universal principle. All banks report your balance to CIBIL based on your statement date, so the strategy to pay your credit card bill before the statement date is effective regardless of the card issuer. This is the most reliable way to pay credit card bill before the statement date for a predictable outcome.

7. How will this strategy appear on my Credit Report?

This strategy will positively influence your Credit Report by consistently showing a low Credit Utilization Ratio. Future lenders looking at your Credit Report will see a history of responsible, low-balance accounts, which is a major sign of creditworthiness.

8. What is the best way how to pay credit card bill before the statement date if I have multiple cards?

The best way how to pay your credit card bill before the statement date with multiple cards is to prioritize the card you use the most. Target the card that tends to have the highest balance to make the biggest impact on your individual card utilization. This strategic approach is key for how to pay credit card bill before the statement date effectively.

9. Can I just pay the minimum amount due before the statement date?

No, this is a common point of confusion. The “minimum amount due” is related to your Due Date and payment history. To lower your utilization, you must pay down the total outstanding balance, not just the minimum.

10. What is a “mid-cycle payment” and how does it help?

A “mid-cycle payment” is any payment made between your last statement date and your next one. It helps by reducing the balance that will be reported, making it a core tactic for anyone learning how to pay their credit card bill before the statement date. This is the most practical way to pay credit card bill before the statement date.

11. How can I find my statement date vs due date?

You can easily find your statement date vs due date on your monthly credit card statement, which is available via email or your bank’s net banking portal. Knowing the difference between the statement date vs due date is the crucial first step.

12. Will I still get a bill if I pay credit card bill before the statement date?

Yes, you will still receive a statement. It will simply show a much lower outstanding balance, or a zero balance if you paid in full. This statement is your official record, even when you pay credit card bill before the statement date, and it’s important to review it for accuracy. This process is a normal part of how to pay your credit card bill before the statement date.

13. Does this strategy to improve my CIBIL score fast actually work?

Yes, this is one of the most effective strategies to improve your CIBIL score fast because it directly impacts your Credit Utilization Ratio, which has no “memory.” By lowering your reported balance this month, you can see a positive change in your score much faster than by just building payment history, making it a key tactic to improve your CIBIL score fast.

14. What happens to my reward points if I pay early?

Your reward points are not affected. You earn points at the time of the transaction, not at the time of payment. Paying early is a smart financial move that will not impact your rewards.

15. Is there a downside to the strategy of how to pay credit card bill before the statement date?

There is no downside to your CIBIL score. The only consideration is your personal cash flow. The core of how to pay credit card bill before the statement date is simply making a payment earlier than you otherwise would have. As long as you have the funds available, this strategy for how to pay your credit card bill before the statement date is a purely positive action for your credit health.

16. How does a lower reported balance on my credit report help me?

A lower reported balance results in a lower Credit Utilization Ratio, which is a powerful positive signal to lenders. Consistently having a lower reported balance shows that you are a responsible borrower who does not rely heavily on credit.

About the Author

This expert guide on how to pay credit card bill before the statement date was written by Anwar Hashmi, the founder and Chief Editor of cibilized.in. He is a financial writer who excels at making complex financial systems simple, providing expert, data-driven guides on the Indian CIBIL score. For insights on U.S. finance, he is also the lead author at ClaimCredits.online, specializing in USA Tax Credits.