Curious if does prepaying home loan affect Cibil score? This expert guide reveals the surprising truth. Learn how prepaying home loan affect Cibil score and what to do.

You’ve worked hard, saved diligently, and you’re finally in a position to do something incredible: prepay your home loan and become completely debt-free. It feels like the ultimate financial victory. But in the excitement, a crucial question is often overlooked. The hidden question on every homeowner’s mind is, “does prepaying home loan affect Cibil score?”

My name is Anwar Hashmi, and at cibilized.in, I’ve seen the confusion this causes. The answer is more complex than you might think. Yes, this smart financial move can have a surprising, and sometimes even negative, short-term impact on your Credit Report. This guide is your definitive masterclass on this topic.

By the end, you will understand the real answer to “does prepaying home loan affect Cibil score” and have a clear strategy to ensure the outcome is a positive one for your financial future. We will explore exactly why prepaying home loan affect Cibil score and how to manage it like an expert.

The Two Sides of the Coin: The Immediate CIBIL Score Impact

So, let’s get straight to the heart of the matter. When a client comes to me with their prepayment plan, the first question they always ask is, “does prepaying home loan affect Cibil score?” The answer is a surprising “Yes, it absolutely does,” but in two very different ways—one positive and one potentially negative.

Understanding this dual impact is crucial. The decision to prepay your home loan isn’t just about becoming debt-free; it’s a strategic move that will alter your credit profile. Let’s break down the two sides of this coin so you can make a fully informed decision.

The Good: A Lower Debt-to-Income Ratio

First, let’s talk about the significant, and often overlooked, positive. While many people worry about the CIBIL score, they forget about a different metric that lenders scrutinize just as closely: your Debt-to-Income (DTI) ratio.

Your DTI ratio is a simple percentage that shows how much of your monthly income goes towards paying your total monthly debt obligations (all your EMIs). When you prepay your home loan, you are eliminating your single largest monthly EMI. This causes your DTI ratio to plummet, which is a massive positive signal to all future lenders.

It proves that you have freed up a huge portion of your income, drastically increasing your capacity to take on new credit responsibly. So while the question, “does prepaying home loan affect Cibil score?” is important, it’s also crucial to remember this powerful positive impact on your overall financial profile.

The Bad: The Potential for a Score Drop

Now, let’s address the part that causes the most confusion. The surprising truth is that prepaying your home loan can cause a temporary drop in your CIBIL score, sometimes by 10 to 20 points. This can be shocking if you’re not expecting it.

This dip doesn’t happen because you’ve done something wrong. It happens because you have fundamentally changed the structure of your credit profile. There are two main technical reasons why this occurs. Understanding these is the key to truly answering the question, “does prepaying home loan affect Cibil score?”

The “Credit History Age” Impact

One of the key factors in your CIBIL score calculation is the “Average Age of Your Credit Accounts.” Lenders love to see a long, stable credit history because it gives them more data to assess your reliability.

For a vast majority of Indians, their home loan is their oldest active credit account. It acts as the anchor of their credit history. When you prepay this loan, the account is marked as “Closed.” While it remains on your Credit Report for years as a positive mark, it no longer contributes to the average age of your active accounts.

This can shorten your average credit age, and this reduction is a key reason prepaying home loan affect Cibil score in the short term.

The “Credit Mix” Impact

The second reason for the temporary drop relates to your “Credit Mix.” CIBIL’s algorithm gives a positive weight to users who can responsibly manage a healthy mix of different types of credit:

- Secured Loans: Loans backed by an asset, like a home loan or a car loan.

- Unsecured Loans: Loans with no collateral, like personal loans and credit cards.

A home loan is a high-quality, long-term secured loan. When you prepay it, you are removing this powerful element from your active credit mix. If you are only left with unsecured credit cards, your profile can suddenly look less diverse and slightly riskier to the algorithm. This shift in your credit mix is the second major way prepaying home loan affect Cibil score.

Strategic Prepayment: A Checklist to Protect Your CIBIL Score

Now that you understand the dual impact of prepayment, you can move from a place of uncertainty to one of strategy. In my experience, the decision to prepay should not be based solely on the desire to be debt-free; it should be a calculated move that aligns with your broader financial goals and your current credit profile.

The temporary dip in your CIBIL score is not a reason to avoid prepayment, but it is a factor you must plan for. Before you make that final payment, I want you to walk through this pre-prepayment CIBIL checklist.

This is the high-value, actionable core of this article, designed to help you determine if now is the right time and to ensure a positive outcome when prepaying home loan affect Cibil score.

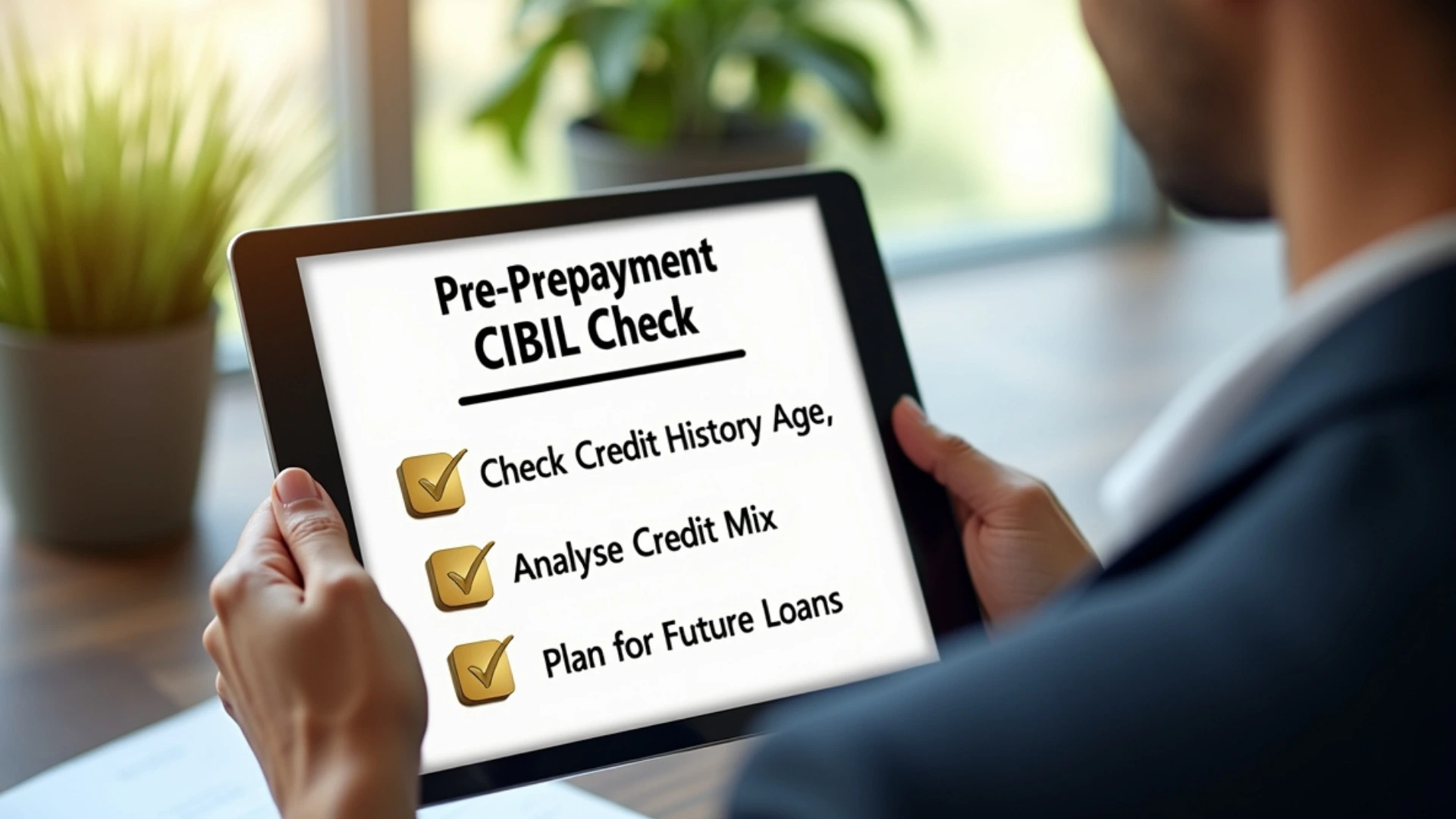

Your Pre-Prepayment CIBIL Checklist

[ ] Check Your Credit Report First: Is Your History Anchored?

Before you do anything, pull your latest Credit Report. The most important question you need to answer is: “Is my home loan my oldest active credit account?” If the answer is yes, you need to be prepared for the impact on your credit history age.

To mitigate this, ensure you have other old, active credit accounts (like a credit card that’s 5+ years old) that will remain open. These accounts will become the new “anchors” of your credit history, softening the blow of closing your oldest loan. This is a critical step because prepaying home loan affect Cibil score most significantly if it erases your longest credit relationship.

[ ] Analyze Your Credit Mix: What Will Be Left?

Look at the “Account Information” section of your CIBIL report. After your home loan is marked “Closed,” what types of active credit will you have left?

If you will still have a healthy mix (for example, a car loan and a credit card), the impact will be minimal. However, if your home loan is your only secured loan and you will be left with only unsecured credit cards, your credit mix will become less diverse. Understanding this is a key part of answering if prepaying home loan affect Cibil score negatively in your specific situation.

[ ] Plan for Future Loans: What’s on Your 12-Month Horizon?

This is the most important strategic question. Do you plan to apply for another major loan (like a business loan, a car loan, or another property loan) in the next 6-12 months?

If the answer is yes, it might be better to wait before prepaying your home loan. The potential short-term dip in your score could affect your eligibility or the interest rate you are offered on your new loan. It’s crucial to consider how prepaying home loan affect Cibil score in the context of your immediate financial goals.

By waiting until after your next major loan is approved, you ensure you are applying with the highest possible score. Acknowledging that prepaying home loan affect Cibil score allows you to time your actions for maximum benefit.

The Long-Term View: Why Prepayment is Almost Always a Win

After learning about the potential for a temporary score drop, it’s natural to feel a little hesitant. You might be asking yourself, “If there’s a risk, is it even worth it?” This is where it’s crucial to shift your perspective from the short-term fluctuation to the massive, long-term benefits.

In my years as a financial writer, I can tell you with absolute confidence that prepaying your home loan is one of the most powerful and positive financial decisions you can make.

The key is to understand that the minor, temporary dip in your score is insignificant compared to the permanent, positive story you are telling on your Credit Report.

Short-Term Pain, Long-Term Gain

Let’s be perfectly clear: any score drop you experience after prepaying your home loan is almost always minor and temporary. Think of it like a small dip in the stock market; it’s a momentary fluctuation, not a long-term crash.

Your score will typically recover and even surpass its previous level within 6 to 9 months, as the algorithm adjusts to your new, much lower debt-to-income ratio and continues to see your perfect payment history on other accounts.

So while it’s true that prepaying home loan affect Cibil score in the short term, this “pain” is a small price to pay for the enormous long-term gain.

The Power of a “Closed” Home Loan on Your Report

This is the most important benefit, and the ultimate answer to the question, “does prepaying home loan affect Cibil score?” When you successfully prepay your home loan, the account is marked as “Closed” on your CIBIL report. This “Closed” status is not a neutral event; it is a trophy.

It is the single most powerful, positive signal of creditworthiness you can have. It is a permanent, shining testament on your report that you successfully managed and paid off the largest and most significant financial obligation of your life. This mark remains on your Credit Report for years, acting as an undeniable reference for every future lender.

When a new lender pulls your report five years from now and sees that you successfully closed a home loan, it sends an incredibly powerful message. It tells them that you are a reliable, disciplined, and highly trustworthy borrower.

This single, positive mark can make it significantly easier for you to get approved for future loans at the best possible interest rates.

So, while the immediate answer to “does prepaying home loan affect Cibil score?” can be a small, temporary dip, the long-term answer is a resounding “yes” in a hugely positive way.

The ultimate proof that prepaying home loan affect Cibil score for the better is that “Closed” status, a gold star that will benefit you for years to come. That is why, from a strategic perspective, the benefit of prepayment almost always outweighs the minor, short-term risk.

From Borrower to Owner: The Final Verdict

The journey from being a home loan borrower to a homeowner is a significant and rewarding one. Prepaying your home loan is a fantastic financial goal and a powerful step towards true financial freedom. As this guide has shown, while the question, “does prepaying home loan affect Cibil score?” can be complex, the outcome is overwhelmingly positive.

The key takeaway is to approach this decision strategically. You now understand that while it can cause a small, temporary dip in your CIBIL score due to changes in your credit mix and history age, this is a minor fluctuation. The long-term benefits—both the massive savings in interest and the powerful, permanent “Closed” status on your Credit Report—far outweigh this short-term effect.

The foundation of a successful prepayment is a strong financial profile. For a complete picture of all the factors that contribute to an excellent score and to build a holistic credit strategy, read our main pillar post: The Ultimate Guide to CIBIL Score for Home Loans.

Frequently Asked Questions About Home Loan Prepayment and Your CIBIL Score

1. What is the most immediate impact of home loan closure on Cibil score?

The most immediate impact of home loan closure on Cibil score is often a small, temporary dip. This happens because closing your oldest account can shorten your credit history age, but the long-term impact of home loan closure on Cibil score is overwhelmingly positive.

2. Is it true that does prepaying home loan affect cibil score negatively at first?

Yes, it is true. The reason prepaying a home loan affects your Cibil score negatively in the short term is due to changes in your credit mix and average credit age. However, this minor dip is temporary, and understanding why prepaying home loan affect Cibil score this way is key to a smart financial strategy.

3. What is the difference between home loan foreclosure vs prepayment cibil impact?

In terms of CIBIL impact, a home loan foreclosure vs prepayment are seen very differently. A prepayment is a positive event. A foreclosure, which is an involuntary closure by the bank due to non-payment, is a major negative event. The CIBIL impact of a home loan foreclosure vs prepayment is the difference between being a responsible borrower and a high-risk one.

4. Will my CIBIL score after closing home loan be permanently lower?

No, your CIBIL score after closing your home loan will not be permanently lower. After a small, temporary dip, your CIBIL score after closing your home loan will recover and likely increase within 6-9 months as your lower debt-to-income ratio is factored in.

5. How important is my credit history age for my CIBIL score?

Your credit history age is a significant factor, making up about 15% of your score. Lenders value a long and stable credit history age as it proves your experience and reliability in managing credit over time.

6. Why does prepaying home loan affect cibil score if I have paid everything perfectly?

The reason prepaying home loan affect Cibil score is purely technical, not a reflection of bad behaviour. It changes the structure of your credit profile by altering your credit mix and history age. The long-term record of a successful closure proves that prepaying your home loan affects your Cibil score in a hugely positive way over time.

7. Should I worry about a temporary score drop after prepaying my loan?

No, you should not worry about a temporary score drop. This small dip is an expected and normal part of the process. The long-term benefits of being debt-free and having a closed home loan on your report far outweigh the minor, temporary score drop.

8. What are the main home loan prepayment pros and cons for Cibil?

The main home loan prepayment pros and cons for Cibil are clear. The pro is the massive positive signal of a successfully closed loan on your report. The con is the minor, temporary score dip. Ultimately, for your CIBIL score, the home loan prepayment pros and cons weigh heavily in favor of prepayment.

9. How does prepaying my home loan improve my debt-to-income ratio?

Prepaying your home loan dramatically improves your debt-to-income ratio by eliminating your single largest monthly EMI. A lower debt-to-income ratio is a massive positive for future lenders, showing you have more disposable income to handle new credit.

10. What is the most important document to get after a home loan closure?

After a home loan closure, the most critical document you must obtain from your lender is the “No-Dues Certificate” (NDC). This is your official, irrefutable proof that the loan has been fully paid off and the account is closed, preventing any future disputes.

11. Is it a good idea to prepay my loan if it’s my only active loan and will hurt my credit mix?

If it’s your only loan, the impact on your credit mix will be higher. In this specific case, it might be strategic to first open a simple credit card and build a few months of payment history before closing the loan to maintain a healthy credit mix.

12. So, does prepaying home loan affect Cibil score more than just closing a credit card?

Yes. The reason prepaying a home loan affects your Cibil score more is due to the size and type of the loan. A home loan is a large, secured loan that acts as a major anchor for your credit history, so closing it has a more noticeable, albeit still temporary, impact than closing a small credit card. Understanding how prepaying home loan affect Cibil score is about understanding its scale.

13. What is the main long-term benefit of prepayment for my CIBIL report?

The primary long-term benefit of prepayment is the powerful “Closed” status that remains on your report for years. This is the ultimate proof of creditworthiness, and this single long-term benefit of prepayment will help you secure better terms on all future loans.

14. If I need a new loan soon, does prepaying my home loan affect my Cibil score in a way that could cause rejection?

Yes, it could. This is why our guide recommends not prepaying if you plan to apply for another large loan within the next 6-12 months. The reason prepaying home loan affect Cibil score with a temporary dip could be the difference between approval and rejection for that new loan, so timing is critical if you want to ensure prepaying home loan affect Cibil score in the right way for your goals.

15. Does the bank automatically report my home loan closure to CIBIL?

Yes, banks are required to report your home loan closure in their next reporting cycle (within 15-30 days). However, it is always a good practice to check your CIBIL report 1-2 months after receiving your NDC to confirm the home loan closure has been updated correctly.

16. I am ready to prepay, does prepaying my home loan affect my Cibil score enough that I should wait?

For most people, no. Unless you need to apply for another major loan in the immediate future, the answer to “does prepaying home loan affect Cibil score?” is that the minor, temporary dip is a small price to pay for the massive financial freedom and long-term credit benefits. The fact that prepaying home loan affects Cibil score is simply a technical detail in an overwhelmingly positive financial decision.

About the Author

This expert guide on the CIBIL score impact of prepaying a home loan was written by Anwar Hashmi, the founder and Chief Editor of cibilized.in. He excels at providing clear, strategic action plans for major financial decisions, helping Indians navigate the complexities of the credit system. For expertise on American finance, he is also the lead author at ClaimCredits.online, specializing in USA Tax Credits.