Let’s set the scene: It is the final week of the month, your bank balance is practically laughing at you, and you are standing at the grocery billing counter. Your favorite payment app suddenly flashes a shiny “Pre-Approved Credit” button, you scan the QR code, and walk out feeling like an absolute boss.

It feels like you just unlocked an infinite money glitch in the matrix, right? But hold your horses, because we need to clearly define exactly what this financial “magic” is for the record before you celebrate.

A UPI credit line is a pre-approved, unsecured loan limit authorized by your bank that allows you to make instant UPI payments even with a zero bank balance.

Fast forward a few weeks, and that sweet financial convenience quickly morphs into a massive headache. You decide to check your credit health, and suddenly, you are frantically searching the internet for the UPI Credit Line Scam.

Why the sudden panic? Because your previously pristine credit report now looks like somebody threw a grenade right into the middle of it. Millions of Indians are feeling utterly trapped in what they loudly call a UPI Credit Line Scam after spotting weird, unknown loan accounts, causing the exact same panic as when an Old Loan Suddenly Appeared on Your CIBIL report out of nowhere.

You probably thought you were just using a modern “buy now, pay later” wallet feature for your daily expenses and evening snacks. Instead, the brutal reality of the UPI Credit Line Scam is that banks treat every ₹150 Swiggy order as a mini personal loan.

This so-called “free money” comes with severe, hidden CIBIL consequences that nobody bothered to explain in bold letters on the app. While it isn’t a literal fraud, the absolute lack of transparency is exactly why users feel victimized by the UPI Credit Line Scam.

To give credit where it is due, the Reserve Bank of India (RBI) officially introduced credit lines on UPI with good intentions to boost digital inclusion. Unfortunately, the overly enthusiastic marketing by payment apps has birthed the widespread UPI Credit Line Scam panic we see today.

When you casually clicked “Activate,” you unknowingly authorized a hard inquiry on your credit profile for a very small limit. People are only waking up to this UPI Credit Line Scam when their applications for actual, important loans (like a car or home) get inexplicably rejected.

Imagine getting your dream home loan denied because you missed a ₹300 repayment for a movie ticket you bought on digital credit! This is exactly why the UPI Credit Line Scam is trending; it feels like a ridiculous trap set up for the average, unsuspecting consumer.

It is ironically funny how we Indians will argue with a rickshaw wala for ₹10, but blindly accept terms and conditions that tank our credit scores. To ensure you aren’t secretly harboring these micro-loans, you must download and analyze your detailed CIBIL report immediately to check your active accounts.

If you choose to ignore this, the UPI Credit Line Scam will quietly inflate your Credit Utilization Ratio (CUR) and severely damage your financial credibility. You are essentially borrowing unsecured, high-interest funds just to pay for your weekend pizza cravings!

In the rest of this comprehensive guide, we will break down exactly how this UPI Credit Line Scam secretly reports to bureaus like Experian and CIBIL. Stay tuned, because we are going to help you escape this digital debt trap and fix your credit profile before it is too late.

Table of Contents

Does UPI credit line affect CIBIL score? The Brutal Truth

Let’s address the elephant in the room right away for everyone wondering about this digital trap. If you are frantically searching the internet asking, does a UPI credit line affect CIBIL score, here is the direct answer: “Yes, a UPI credit line directly affects your CIBIL score.”

It is definitely not just a casual digital wallet or a magical free pass to buy snacks when you are completely broke. The reality of how a UPI credit line affect CIBIL score is actually quite serious and mathematically strict.

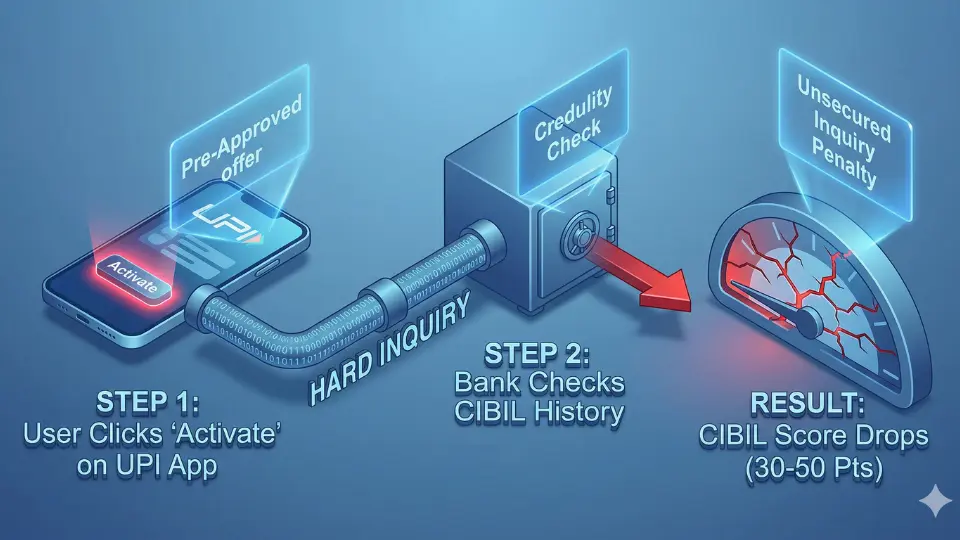

Every single time you excitedly accept that flashy “pre-approved” offer on your favorite payment app, the partner bank takes immediate action. They pull your credit history, which officially triggers a ‘Hard Inquiry’ on your overall credit profile. If you did not explicitly authorize this background check, you need to learn How to Remove Hard Inquiry from CIBIL Report immediately to restore your points.

Having too many hard inquiries in a very short span makes you look desperate and credit-hungry to other major lenders. This is the first hidden way a UPI credit line affect CIBIL score before you even spend a single rupee at the shop!

Now, let’s talk about the actual daily usage and how you spend this digital, invisible money. You might think buying a ₹500 grocery order won’t matter at all, but the lending banks are watching you like strict Indian parents.

When people frequently ask me how a UPI credit line affect CIBIL score, I always point them to the repayment cycle. Making your payments perfectly on time can actually help build your score slowly, acting just like a traditional credit builder loan.

However, the real danger lies in the ridiculously short billing cycles that catch most average users completely off guard. Missing a due date by just one single day is exactly where the financial disaster truly begins for most folks.

A minor 1-day delay on a tiny ₹500 milk and bread bill gets reported to the credit bureaus almost immediately. This is exactly how a UPI credit line affect CIBIL score in the most negative, frustrating, and brutal way possible.

That tiny delayed payment will reflect as a default or “Days Past Due” (DPD) on your official credit report for years. It can instantly drop your score by 30 to 50 points, completely ruining months of your good, disciplined financial behavior.

If you want to understand the exact mechanics of DPD, you can read the official educational guidelines on TransUnion CIBIL’s website. They clearly state that any unsecured credit facility delay, no matter how small, severely impacts your overall credit health.

It is almost funny how a delayed ₹500 weekend pizza payment can literally stop you from getting a ₹50 Lakh home loan later. But this is the harsh, unbending reality of how a UPI credit line affect CIBIL score in the current financial landscape.

Many terrified users simply uninstall the payment app thinking the loan will just magically disappear from their lives. Spoiler alert: deleting the app does not delete your legal debt, nor does it stop how the UPI credit line affect CIBIL score.

The loan account remains fully active under your PAN card until you officially clear the dues and get a No Objection Certificate.

We constantly see users in our forums crying over rejected premium credit card applications because of these tiny, forgotten hidden defaults. They only realize way too late that a UPI credit line affect CIBIL score exactly like a massive, unpaid personal loan default.

So, the next time you are tempted to casually scan that QR code on borrowed bank money, remember this brutal truth. Treat this micro-credit facility with the exact same fear and deep respect you would give to a strict, non-nonsense bank manager!

The Core Issue: Is UPI credit reported as personal loan?

The modern convenience of scanning a QR code with zero bank balance feels like a magical digital superpower. However, the core technical mismatch happens because most users treat this feature like a simple, harmless “Buy Now Pay Later” wallet. The absolute burning question on everyone’s mind right now is whether UPI credit reported as personal loan by these partner banks.

It honestly feels like a massive financial betrayal to the average, hardworking Indian consumer. You thought you were just getting a friendly, invisible tab at your local kirana store for your monthly groceries. Instead, you wake up to find out that having UPI credit reported as personal loan is the harsh, underlying reality of this feature.

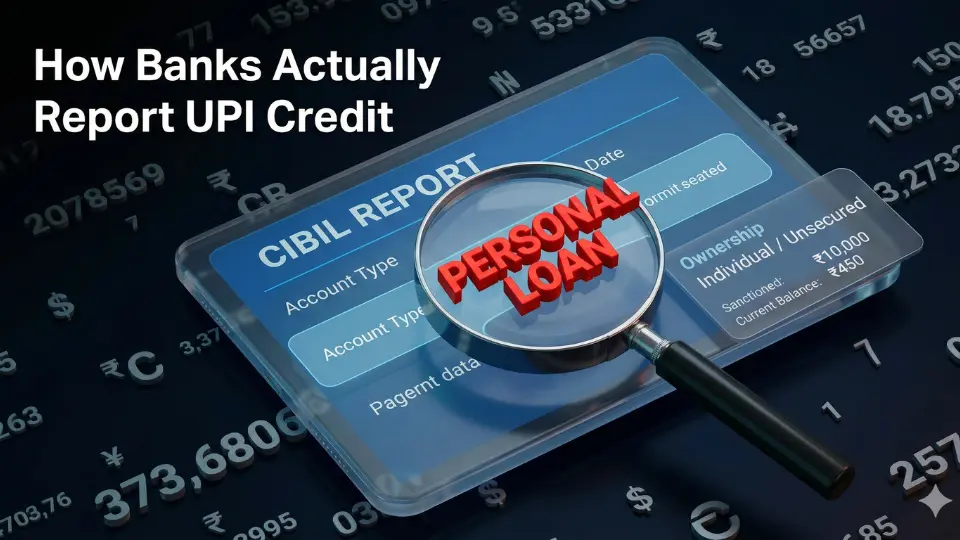

Let us completely clear the air on exactly how UPI credit reported as personal loan in the complex backend banking systems. Unlike a standard traditional credit card, which is officially categorized as “revolving credit,” this pre-approved UPI line is structurally completely different. It falls strictly under the rigid umbrella of unsecured digital lending.

Depending on the specific NBFC or partner bank backing your favorite payment app, the exact reporting format on your file can actually vary. While some institutions report it as a short-term ‘Overdraft’ facility, the most common scenario is seeing UPI credit reported as personal loan. Both of these specific formats will drastically impact your overall credit utilization ratio.

Why should you genuinely care if UPI credit reported as personal loan on your official credit bureau file? Because major credit bureaus evaluate revolving credit cards and unsecured personal loans very differently in their core scoring algorithms. A personal loan makes you look like you have a heavier financial burden compared to a standard, flexible credit card limit.

To make this complex banking concept crystal clear, let’s look at a practical, real-world example of this sneaky entry. Below is an exact visual mockup showing exactly how you will see UPI credit reported as personal loan when you finally download your file.

Mockup: 2026 CIBIL Report Entry

As you can clearly see in the text box above, having UPI credit reported as personal loan makes your financial profile look quite messy and cluttered. Instead of having one clean, high-limit credit card, you suddenly have a history of multiple tiny, unsecured loans. It makes you look desperate for quick cash to other major lenders reviewing your file.

This strict reporting mechanism isn’t just a random choice made by the payment applications to intentionally annoy you. The Reserve Bank of India’s strict digital lending guidelines legally mandate that all such micro-credit facilities must be reported to Credit Information Companies (CICs). The government does this to prevent systemic defaults across the banking sector.

This hidden reporting mechanic is exactly why we constantly advise our readers to stay highly vigilant about their data. Do not let a forgotten payment app quietly ruin your future borrowing power!

So, the next time your friend confusedly asks you, “Is UPI credit reported as personal loan?” you can confidently tell them the brutal truth. It is definitely not just a harmless digital ledger extending you a quick, friendly favor for the weekend. It is a legally binding, fully tracked unsecured credit facility that demands absolute discipline.

Knowing the exact backend mechanics of how UPI credit reported as personal loan allows you to make much smarter financial choices. You will definitely think twice before blindly scanning a QR code for a quick cup of tea or a snack. Let’s absolutely not let a simple ₹20 chai bill ruin our financial peace of mind and CIBIL score in 2026!

5 Major Pre approved UPI credit line disadvantages You Must Know

Scanning a merchant’s QR code when your bank account is completely empty feels like a fantastic superpower in the moment. However, you need to wake up to reality, because the long-term hidden costs and severe UPI credit line disadvantages can secretly damage your financial health.

The Trap of Frictionless Overspending

The biggest trap of these micro-loans is simply how ridiculously smooth the technology is. Scanning a QR code doesn’t feel like spending “real money,” making it way too easy to blindly overspend on late-night food deliveries and random shopping sprees.

Before you even realize it, that casual daily ₹100 tea bill piles up into a massive, unmanageable monthly debt. This psychological disconnect is one of the most dangerous UPI credit line disadvantages, perfectly designed to make you spend far beyond your salary without feeling the pinch!

A Cluttered and Messy Credit Profile

We all have that temptation to click “Activate” when apps like GPay, PhonePe, or Paytm throw flashy pre-approved offers at our screens. But here is one of the most ignored UPI credit line disadvantages: activating multiple limits creates an incredibly cluttered and messy credit report.

The credit bureau doesn’t see you as a savvy tech user; it sees a desperate need for credit. This results in multiple small, unsecured loans permanently sitting on your CIBIL report, which is a massive red flag for any serious financial institution analyzing your profile.

The Double Penalty of Auto-Debit Bounces

What exactly happens when your linked bank account lacks funds on the auto-debit repayment date? You get hit by a financial truck. A highly punishing entry on the list of UPI credit line disadvantages is the dreaded “double hit” penalty that drains your wallet.

First, your bank will slap you with a heavy NACH bounce penalty fee (often ₹500 or more) for the failed mandate, as per standard RBI procedural guidelines regarding auto-debits. Second, you take a direct, immediate hit on your CIBIL score for a missed loan payment.

Negative Impact on Future Big Loans

Let’s look at the long-term consequences for your major life goals. When you finally sit down with a strict bank manager to secure funds for a house, the UPI credit line disadvantages become painfully clear.

However, if the digital damage is already done, there are still proven banking strategies to secure a Home Loan with a Low CIBIL Score if you act quickly.

Traditional lenders strongly hesitate to approve high-value applications, like home or car loans, for applicants with several active “micro” unsecured credit lines.

To a bank underwriter, relying on a ₹5,000 digital loan signals underlying financial instability. To protect your major life goals, you should regularly monitor your detailed credit report to ensure these tiny debts aren’t ruining your chances of buying your dream home.

Understanding these critical UPI credit line disadvantages is essential before you happily scan that next QR code. Being fully aware of these UPI credit line disadvantages today will easily save you from years of frustrating credit repair headaches tomorrow.

Exposing the UPI credit line hidden charges 2026

Let’s be brutally honest for a second: there are absolutely no free lunches in the modern Indian banking sector. If an app is aggressively offering you a shiny, instant limit to buy your evening biryani, you are about to encounter some serious UPI credit line hidden charges.

People easily get lured by the massive ‘zero interest’ marketing trap, completely believing the ‘free money’ myth, which is dangerously similar to the shock many face when discovering Amazon Pay Later Hidden Charges on their monthly statements.. But the reality of digital lending is quite different, highly conditional, and often much more expensive than you initially anticipate.

The exact moment your rapid billing cycle ends and you accidentally forget to pay, a whole menu of UPI credit line hidden charges suddenly appears out of thin air. This complete lack of upfront transparency is exactly why frustrated consumers are aggressively calling it a UPI Credit Line Scam on social media platforms.

When evaluating flashy financial products, ignoring the fine print where UPI credit line hidden charges secretly live is your biggest mistake. These sudden fees act like silent financial ninjas, quietly draining your hard-earned bank balance while you sleep.

You might genuinely think you just borrowed a harmless ₹500 for weekend groceries, but your final monthly statement will shock you. Experiencing this sudden, unexpected financial drain due to UPI credit line hidden charges is incredibly painful for an average earner.

To make informed decisions, it helps to look at the official Reserve Bank of India guidelines on digital lending which strictly mandate transparency. The RBI requires banks to issue a Key Fact Statement (KFS) to clearly disclose the Annual Percentage Rate (APR) and any associated fees.

However, payment apps often bury these crucial details deep inside boring, unreadable terms and conditions that nobody ever clicks on. To save you from a nasty financial shock, we are thoroughly exposing these sneaky UPI credit line hidden charges right now.

Here is an eye-opening table breaking down the exact industry average charges in 2026 and how you can practically dodge them:

| Type of Charge | Average Industry Cost (2026) | How to Avoid It |

| Activation / Onboarding Fee | ₹199 to ₹499 + 18% GST (One-time or Annual) | Read the welcome screen carefully before clicking “Accept”. Reject offers with high setup fees. |

| Transaction Processing Fee | 1% to 2% per transaction (or flat ₹10 – ₹50) | Use a standard zero-balance debit card for daily small transactions instead of credit lines. |

| Late Payment Penalty | ₹250 to ₹750 per default cycle | Set up a strict auto-debit mandate from your primary salary account to ensure you never miss a date. |

| Post-Due Date Interest Rate | 36% to 42% Annually (Calculated Daily) | Never, ever carry a balance forward. Pay the entire utilized amount well before the deadline. |

Looking closely at those terrifying numbers, it is incredibly clear why these massive out-of-pocket costs are a huge problem. That “free” ₹300 coffee date can easily cost you an extra ₹500 in bank penalties if you just blink and miss the short due date.

The sheer aggression of these late penalties is a core reason why understanding UPI credit line hidden charges is an absolute necessity today. Furthermore, dealing with this complex and confusing fee structure directly impacts your overall financial stability and peace of mind.

When your digital bill inflates rapidly with these UPI credit line hidden charges, paying it off becomes significantly harder. This easily leads to missed payments, which then get reported directly to major credit bureaus as unsecured loan defaults.

If you suspect you have been secretly hit by an avalanche of UPI credit line hidden charges and it has dragged down your credit profile, do not panic. You need to immediately check your detailed CIBIL score on Cibilized.in to accurately assess the overall damage to your PAN card.

Ultimately, while the underlying payment technology is incredibly convenient, the financial burden it secretly carries is undeniable. By actively acknowledging the massive impact of these UPI credit line hidden charges, you can safely navigate the digital payment space.

Always read the fine print, be a smart consumer, and do not let these UPI credit line hidden charges quietly eat away at your hard-earned savings in 2026!

Head-to-Head: UPI credit line vs credit card CIBIL impact

We Indians absolutely love a good, heated comparison. Whether we are comparing Sharma Ji’s son’s marks to our own, or arguing endlessly over Android versus iPhone, we just need to know who the ultimate winner is. So, when the banking sector threw a shiny new digital toy at us, the ultimate financial showdown became inevitable: analyzing the UPI credit line vs credit card CIBIL impact.

It sounds like a boring heavyweight boxing match between two bank managers, but it is actually about saving your financial future from a sudden knockout punch. You might assume that borrowing money is the same across the board, but the UPI credit line vs credit card CIBIL impact is drastically different behind the scenes.

If you are using these features for larger digital purchases, you should also understand the strict mathematical differences between Buy Now Pay Later vs Credit Card EMI to protect your wallet.

To truly understand why one product might be silently tanking your profile while the other actively builds it, we have to put them head-to-head. When we break down the UPI credit line vs credit card CIBIL impact using raw data, the reality speaks for itself.

Take a look at this comprehensive comparison table to see exactly how these two products behave:

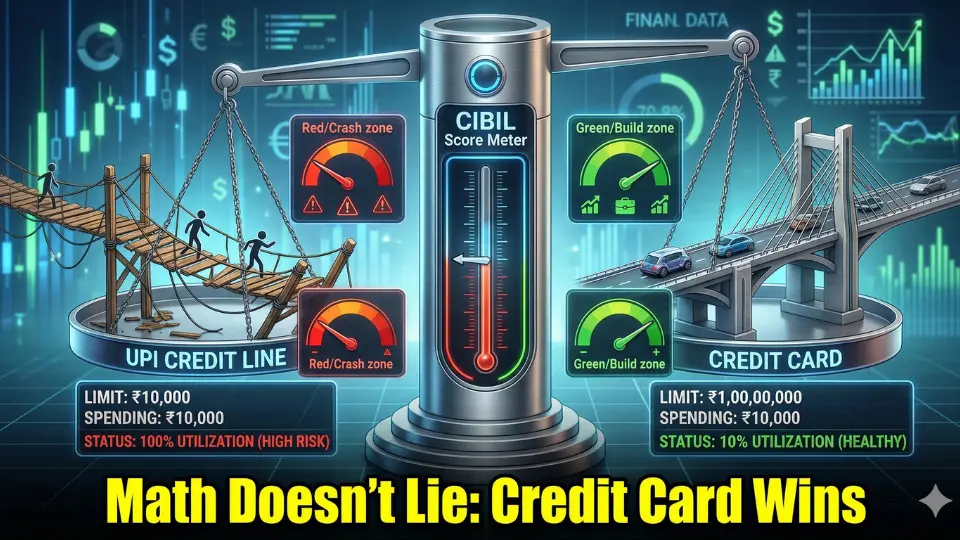

| Feature | Pre-Approved UPI Credit Line | Traditional Credit Card |

| Reporting Format | Unsecured Personal Loan / Overdraft | Revolving Credit Facility |

| Credit Utilization Impact | High Risk: Spending ₹10k on a ₹10k limit = 100% CUR (Massive Score Drop) | Low Risk: Spending ₹10k on a ₹1 Lakh limit = 10% CUR (Healthy Score Builder) |

| Grace Periods | Very Short: 15 to 20 days (or instant billing) | Luxurious: 45 to 50 days of interest-free period |

| Interest Structures | Aggressive daily penalties on minor defaults | Standard Monthly APR structure |

Looking at the official reporting formats, the UPI credit line vs credit card CIBIL impact becomes crystal clear. According to the official guidelines set by TransUnion CIBIL, a traditional credit card is safely reported as “revolving credit.” It is flexible and expected. On the flip side, the system treats these new digital UPI limits as rigid, short-term unsecured loans.

Now, let’s talk about the Credit Utilization Ratio (CUR), because this is exactly where the UPI credit line vs credit card CIBIL impact gets absolutely wild. Imagine you spend ₹10,000 on a weekend trip. If you max out a tiny ₹10,000 UPI credit line, your utilization hits a screaming 100%. That tells the algorithm you are completely broke! But spend that exact same ₹10,000 using a ₹1 Lakh limit credit card, and your utilization sits at a very sweet, healthy 10%.

Furthermore, the massive difference in repayment grace periods heavily dictates the overall UPI credit line vs credit card CIBIL impact. Credit cards give you a comfortable 45 to 50 days to arrange your funds without paying a single rupee in interest. UPI credit lines? They essentially want their money back yesterday. Miss that rapid 15-day window, and the penalties will hit you harder than a strict teacher.

This is exactly why managing the UPI credit line vs credit card CIBIL impact requires two completely different mindsets. One is a calm marathon; the other is a terrifying sprint.

So, what is the definitive conclusion when evaluating the UPI credit line vs credit card CIBIL impact? A traditional credit card is mathematically and structurally far safer for your long-term CIBIL score than a micro UPI line. Credit cards are beautifully designed to build your score if used smartly, offering high limits that naturally keep your credit utilization low.

UPI credit lines, with their tiny limits and aggressive billing cycles, are essentially digital credit traps waiting for you to trip over them. If you are worried about how these products are currently reflecting on your profile, you should definitely check your comprehensive credit report right here on Cibilized.in to evaluate the damage. When it comes down to the ultimate UPI credit line vs credit card CIBIL impact battle, the old-school plastic card wins flawlessly every single time!

Step-by-Step Guide: How to close UPI credit line account Permanently

Okay, take a deep breath and grab a glass of water. After reading about all those terrifying hidden charges, aggressive late fees, and sudden credit score drops, you are probably sweating a little bit. Don’t panic! You are definitely not doomed to carry this annoying digital debt forever.

A lot of panicked users are frantically searching the internet for the exact steps on how to close UPI credit line account Permanently, and honestly, who can blame them? Escaping this financial matrix is entirely possible, but simply uninstalling or deleting the payment app won’t magically make the bank loan disappear (nice try, though!).

To actually protect your long-term financial health, you need to know exactly how to close UPI credit line account Permanently without leaving any messy digital footprints behind. Let’s walk through the ultimate, foolproof checklist so you can finally learn how to close UPI credit line account Permanently and sleep peacefully tonight.

- Clear all pending dues immediately The very first rule of learning how to close UPI credit line account Permanently is understanding that banks simply do not let you break up with them if you still owe them money. Even if it is a tiny ₹10 outstanding balance or a sneaky unbilled late fee, you must pay it off right now. You absolutely cannot initiate the official closure process if your account ledger isn’t sitting at a perfect zero.

- Locate the deactivation setting inside the specific UPI app Once your dues are crystal clear, open the digital payment app where this whole saga originally started. Finding the exit door can sometimes feel like a maze, but it is a crucial step in understanding how to close UPI credit line account Permanently. Navigate to the specific ‘Credit’, ‘Postpaid’, or ‘Loan’ section within the app’s settings and hunt for the “Deactivate,” “Close Account,” or “Opt-out” button. If the app is playing hide-and-seek and doesn’t have a direct button, you will need to aggressively raise a formal closure request through their in-app customer support chat.

- Contact the partner bank/NBFC directly for an NOC (No Objection Certificate) This step is your golden ticket! Remember, the payment app is just the flashy middleman; the actual loan is provided by a backend partner bank or NBFC. To legally finalize how to close UPI credit line account Permanently, you must demand a formal NOC (No Objection Certificate) or Closure Letter from the lending institution. If you find your Bank Not Giving NOC After Loan Settlement, you have strict legal rights under RBI guidelines to force them to issue it. The Reserve Bank of India’s Fair Practices Code clearly empowers borrowers with the absolute right to receive their loan closure documents. Email the bank’s official customer care with your loan account number and forcefully ask for this certificate. Keep this PDF document highly secure; it is your ultimate proof that you are completely debt-free!

- Wait 30-45 days and check the CIBIL report to ensure the status shows “Closed” Patience is a virtue, especially when dealing with the Indian banking system. The final phase of how to close UPI credit line account Permanently requires a bit of waiting. Banks generally update credit bureaus at the very end of their monthly billing cycles, so it usually takes about 30 to 45 days for the “Active” loan status to officially change. After a month has passed, you must verify this backend update yourself. You can easily download and review your updated credit report on Cibilized.in to confirm that the ghost of this digital loan has officially left your PAN card, and the account status clearly reads “Closed” with a zero balance.

And there you have it! If your friends or family members are also stuck in this trap, be a good pal and teach them how to close UPI credit line account Permanently. By strictly following this actionable checklist, you are taking back full control of your financial profile and ensuring that no sneaky micro-loan will ever sabotage your future credit applications!

Frequently Asked Questions (FAQs)

Q1: Does checking my eligibility trap me in the UPI Credit Line Scam, and does UPI credit line affect CIBIL score immediately?

Simply checking your basic eligibility on a payment app will not trap you in the so-called UPI Credit Line Scam. However, the moment you click “Activate” or “Accept,” it triggers a hard inquiry on your PAN card. Once active, the answer to whether a UPI credit line affect CIBIL score is a resounding yes, as every transaction is closely monitored.

Q2: What are the UPI credit line hidden charges 2026 that make consumers call this a UPI Credit Line Scam?

The widespread panic regarding the UPI Credit Line Scam primarily stems from a severe lack of upfront transparency. The UPI credit line hidden charges 2026 often include unexpected onboarding fees, daily compounding interest on late payments, and heavy NACH bounce penalties. Always read the Key Fact Statement (KFS) to avoid these financial shocks.

Q3: Why is UPI credit reported as personal loan, and is this the actual reason behind the UPI Credit Line Scam?

Yes, the core reason many financial experts warn about this UPI Credit Line Scam is the rigid backend reporting structure. Because UPI credit reported as personal loan or overdraft by the partner NBFCs, it significantly raises your Credit Utilization Ratio. This strict reporting format instantly makes your credit profile look cluttered and desperate to other lenders.

Q4: How to close UPI credit line account permanently to finally escape the UPI Credit Line Scam?

Simply uninstalling your favorite payment app will not save you from the UPI Credit Line Scam or clear your active digital debt. To legally and safely learn how to close UPI credit line account permanently, you must pay off all pending dues first. Afterward, you must contact the lending bank directly to secure a formal No Objection Certificate (NOC).

The Final Verdict: Outsmarting the Digital Debt Trap in 2026

At the end of the day, financial convenience should never come at the hidden cost of your long-term credit health. The rising panic surrounding the UPI Credit Line Scam is a harsh wake-up call for millions of digital-first consumers across India.

While it is technically a legally approved banking product, the deceptive marketing makes the UPI Credit Line Scam incredibly dangerous for unsuspecting buyers. Treating this digital micro-loan like a casual “buy now, pay later” wallet will undoubtedly ruin your chances of securing major life loans in the future.

If you value your financial peace of mind, it is always mathematically safer to rely on a traditional credit card with a standard grace period. Do not let the digital convenience of the UPI Credit Line Scam quietly drain your bank account through aggressive hidden charges and penalties.

Take immediate control of your financial narrative today before a tiny digital transaction ruins your future. Head over to Cibilized.in to download your detailed credit report right now, and ensure your profile is completely free from these hidden micro-loans!

About the Author

Anwar Hashmi Chief Editor & Financial Credit Expert

Anwar Hashmi is the founder and Chief Editor of Cibilized.in, India’s leading platform for credit awareness and financial literacy. With years of experience in analyzing credit bureau reporting and banking policies, Anwar is on a mission to protect Indian consumers from digital debt traps and “hidden” loan products.

As a dedicated advocate for credit health, he specializes in decoding complex RBI guidelines and helping individuals repair their CIBIL scores to secure their dream home and car loans. When he isn’t auditing financial algorithms or writing deep-dive guides on the UPI Credit Line Scam, Anwar is actively working on the ground to simplify banking for the common man.

Connect with Anwar: anwar@aavaz.in | Check your CIBIL Score here

Pingback: Amazon Pay Later Hidden Charges: 5 Toxic Fees Ruining CIBIL

Pingback: Old Loan Suddenly Appeared on your CIBIL? 3 Fast Fixes to Use

Pingback: Buy Now Pay Later vs Credit Card EMI: 7 TTraps Exposed

Pingback: 1 Mistake Triggers Multiple CIBIL Inquiries: Learn How to Avoid Them

Pingback: Home Loan Rejected After Sanction Letter? 3 Point Action Plan