Have you ever wondered exactly what your three-digit credit number means to a bank? Understanding your credit health is the crucial first step toward true financial freedom.

A CIBIL score is a three-digit numerical summary of your financial history, typically ranging from 300 to 900. It acts as a report card that banks and non-banking financial companies (NBFCs) check before approving loans or credit cards.

Lenders rely heavily on this metric to evaluate your creditworthiness and estimate the risk of default. A higher score instantly tells the lender that you are a responsible borrower who pays dues on time.

As you review your financial standing, it is best to check your CIBIL Report and Credit Report parallelly. This helps you spot exactly how past credit behavior currently impacts your overall borrower profile.

Before applying for any new credit, borrowers must understand exactly where they fall on the CIBIL score range. Knowing your specific tier helps you anticipate whether a bank will approve your application or reject it.

So, What Is a Good CIBIL Score in India? Generally, any score of 750 or above is considered excellent by most major lenders, including the State Bank of India (SBI) and HDFC Bank.

Maintaining a good CIBIL score in India ensures you get quick loan approvals, higher credit limits, and the most favorable interest rates. Ultimately, having an ideal CIBIL score acts as your golden ticket to cheaper and faster credit.

Let’s break down the standard scoring model to see exactly how lenders interpret your financial habits. According to the official CIBIL website, scores are categorized into distinct risk brackets.

The Standard Credit Score Brackets

| CIBIL Score Range | Lender Interpretation | Loan Approval Chances |

|---|---|---|

| 300 – 549 | Poor (High Risk) | Very Low |

| 550 – 649 | Average (Medium Risk) | Low (High Interest Rates) |

| 650 – 749 | Good (Low Risk) | Moderate to High |

| 750 – 900 | Excellent (Minimal Risk) | Very High (Best Rates) |

If your score falls in the lower brackets, banks will view you as a high-risk applicant. In such cases, you might face immediate rejections or be forced to provide a guarantor.

Before applying for major credit, it is highly recommended to proactively learn how to increase your CIBIL score from 600 to 750 through disciplined repayment habits.

Even one missed payment can quickly shift you from the “Excellent” to the “Average” bracket. This is why reading your CIBIL Report and Credit Report parallelly on a regular basis is non-negotiable.

For major financial milestones, lenders are particularly strict regarding your credit history. If you are preparing to buy a house, exploring the ultimate guide to CIBIL score for home loans in India is highly recommended.

Understanding these brackets empowers you to make highly informed borrowing decisions. In the next section, we will explore exactly how these specific ranges affect your everyday banking and loan terms.

CIBIL Score Range Explained (300–900)

When you evaluate your CIBIL Report and Credit Report parallelly, the most prominent feature is a three-digit number ranging from 300 to 900. This numerical summary is a direct reflection of your past financial behavior and current debt management strategies.

Many everyday consumers frequently ask, What Is a Good CIBIL Score in India to secure fast loan approvals? To understand the answer, we must first examine how major Indian lenders categorize these numbers.

The higher your score climbs on this scale, the lower the financial risk you pose to banks and NBFCs.

CIBIL Score Range Chart

| CIBIL Score | Rating | Loan Approval Chances |

| 300–549 | Very Poor | Very Low |

| 550–649 | Poor | Low |

| 650–699 | Fair | Moderate |

| 700–749 | Good | High |

| 750–900 | Excellent | Very High |

What Each CIBIL Score Range Means for Borrowers

Understanding the official brackets helps you predict exactly how a bank manager will evaluate your application. Let’s break down what each specific tier signals to major financial institutions.

300–649: High Risk Borrower

If your score lands in this bottom bracket, mainstream banks like SBI or Kotak Mahindra will classify you as a high-risk applicant. This usually happens due to a history of late payments, previous defaults, or massive credit card debt.

Securing an unsecured loan is exceptionally difficult here, and if approved, the interest rates will be punishing. If you are struggling in this tier, it is highly recommended to explore a proven 6-month action plan to beat rejection for a home loan with a low CIBIL score.

650–699: Fair Credit Profile

Borrowers sitting in the fair category have a moderate chance of loan approval, but they lack strong negotiating power. You might get that car loan or personal loan, but it won’t feature the most favorable interest rates.

Lenders might also require a co-applicant or a larger down payment to safely process your file. Before making a major financial move, take the time to learn how to increase your CIBIL score from 600 to 750 through disciplined repayment.

700–749: Good Creditworthiness

This is a strong position to be in, representing reliable and consistent credit habits. According to the official CIBIL website, individuals in this tier are generally viewed as safe and responsible borrowers.

You will experience much smoother approval processes for credit cards and retail loans without heavy scrutiny. However, to grab the absolute lowest promotional interest rates on home loans, you may still need to push your score slightly higher.

750–900: Excellent Credit Profile

This top-tier bracket represents an excellent credit profile and is the ultimate financial goal for Indian consumers. Leading banks actively compete for customers in this range by offering pre-approved loans, premium cards, and zero processing fees.

You hold all the negotiating power here, ensuring you secure the cheapest credit available in the market. To protect this prime status, ensure you understand how to read your credit card statement properly so you never miss a hidden charge.

How Different CIBIL Scores Affect Loan Approval

When you submit a loan application, the bank’s system immediately pulls your credit history. This simple check acts as the ultimate deciding factor for your financial request, setting the tone for your relationship with the lender.

It determines not only whether you get the money, but also how much it will actually cost you over time. Understanding this approval process gives you a significant advantage as a smart borrower.

When everyday consumers ask, What Is a Good CIBIL Score in India, they are really asking what specific number guarantees the cheapest loan. Let’s look closely at how different marks impact your banking experience.

Is 700 CIBIL Score Good?

Many borrowers frequently wonder, is 700 CIBIL score good enough for a quick and easy approval? The reality is that this number is considered acceptable, but it is definitely not ideal.

Major banks like ICICI or Axis Bank generally view a 700 score as borderline. It shows you have credit experience, but you might have a recent history of late payments or high credit card utilization.

While your loan application might be approved, lenders will protect themselves by charging a higher interest rate. You will likely not qualify for their best promotional offers or pre-approved limits.

If you find yourself stuck at this number, you should review your history carefully. You might need to learn how to dispute errors on your CIBIL report to remove any inaccurate negative marks.

Is 750 CIBIL Score Good?

Moving up the ladder, is 750 CIBIL score good? Absolutely. According to the official CIBIL website, 750 is widely recognized as the golden standard for a strong and healthy credit profile.

This is the ideal score for most major banks and financial institutions across India. Hitting this target clearly signals that you are a highly responsible borrower who always pays dues on time.

You will immediately enjoy much better approval chances for premium credit cards, home loans, and personal loans. Furthermore, you will gain the power to negotiate lower processing fees and interest rates.

If you want to reach this premium tier, you should explore unlock 750+: a step by step plan on how to improve your CIBIL score.

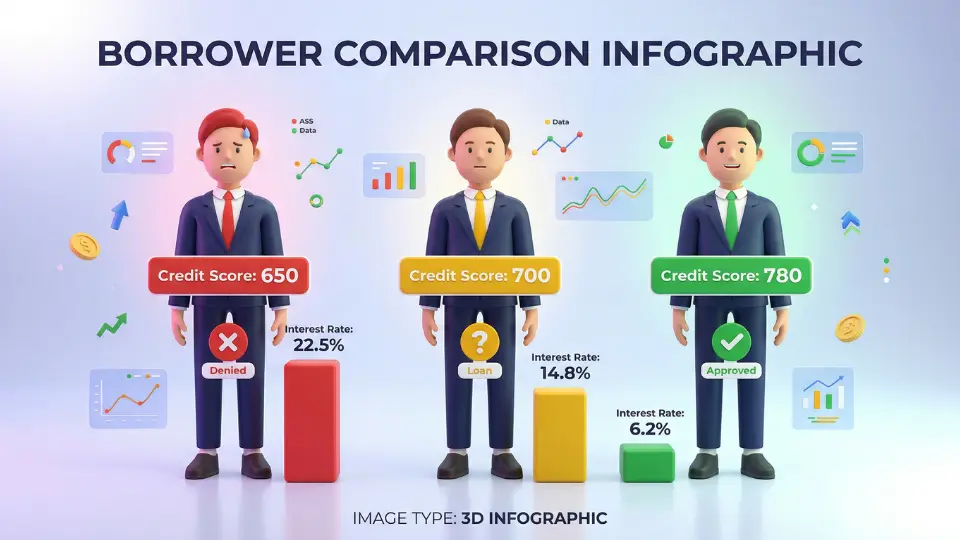

Real Example: How Credit Score Changes Loan Terms

To see exactly how lenders interpret credit scores in the real world, consider this practical scenario. Imagine three different individuals applying for the exact same personal loan at SBI.

| Borrower | Score | Loan Result |

| Borrower A | 650 | Loan rejected |

| Borrower B | 700 | Loan approved at higher interest |

| Borrower C | 780 | Loan approved at lower interest |

As the table clearly shows, Borrower A faces an immediate hurdle. If this happens to you, discovering what to do after credit card application rejected: best 3 step solution is your next crucial step.

Borrower B gets the necessary funds, but the extra interest will cost them thousands of extra rupees over the years.

Meanwhile, Borrower C enjoys the absolute cheapest EMI possible, proving that strong credit habits literally pay off. Maintaining excellent credit is simply the easiest way to keep more of your hard-earned money in your own pocket.

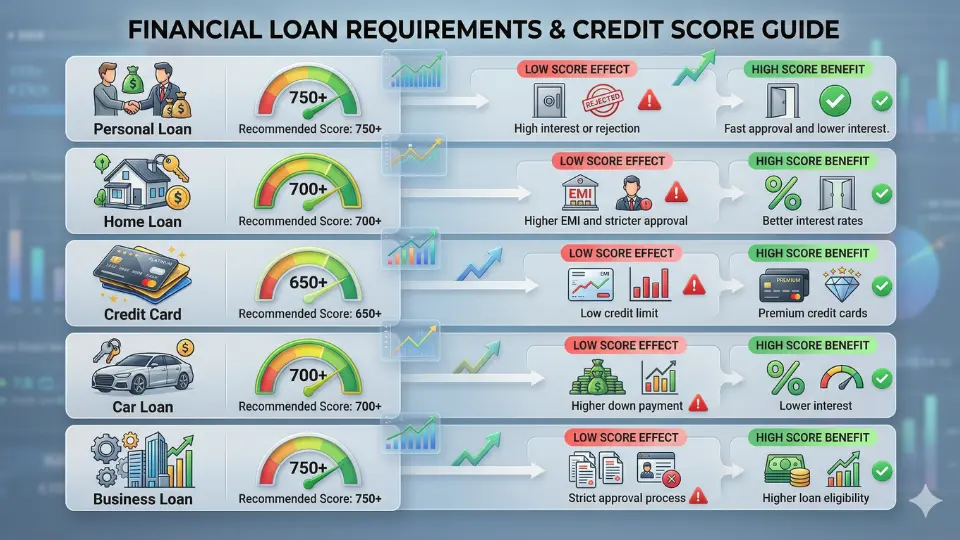

Good CIBIL Score Required for Different Loans

When everyday borrowers ask, What Is a Good CIBIL Score in India, the true answer often depends on the exact financial product they need. Different loan categories carry completely different risk levels for the bank.

Because of this varying risk, major Indian lenders have established unique benchmark scores for unsecured and secured credit.

Good CIBIL Score for Personal Loan

Personal loans are completely unsecured, meaning the bank has absolutely no collateral to claim if you default. Because the financial risk falls entirely on the lender, their approval criteria are incredibly strict.

Typically, a good CIBIL score for personal loan approval sits securely at 750 or higher. Major private banks like HDFC and Axis prefer this premium range when offering their lowest interest rates.

If your current rating falls below this mark, you might face harsh interest rates. I highly suggest exploring unlock 750+: a step by step plan on how to improve your CIBIL score before applying.

Good CIBIL Score for Home Loan

Home loans are secured by the physical property, but the loan amounts are massive and span over several decades. Therefore, banks still thoroughly scrutinize your credit report to ensure long-term financial stability.

According to official CIBIL authority information, a good CIBIL score for home loan applications is generally 700 and above. However, to secure the absolute best promotional EMI rates, aiming for 750+ is highly recommended.

If you are worried about your numbers before buying your dream house, you should read the ultimate guide to CIBIL score for home loans in India (2026).

Good CIBIL Score for Credit Card Approval

Credit cards act as a revolving line of unsecured credit, and the barrier to entry is slightly lower than a personal loan. For basic entry-level cards, a score of 650 to 700 might secure an approval with a smaller limit.

However, premium reward cards with exclusive benefits almost always require a strong score of 750+. Remember, managing these cards poorly can quickly damage your standing.

If you are new to revolving credit, ensure you know how to read your credit card statement: the best step by step guide for 25-26 to avoid hidden penalty fees.

Recommended Score by Loan Type

To make things simple, here is a quick breakdown of what official banking institutions generally expect. Keep these targets in mind before submitting your next application.

| Loan Type | Recommended Score |

| Personal Loan | 750+ |

| Home Loan | 700+ |

| Credit Card | 650+ |

| Car Loan | 700+ |

| Business Loan | 750+ |

Determining exactly What Is a Good CIBIL Score in India often comes down to which specific financial institution you plan to approach. According to official bank guidelines, every top lender sets its own strict internal benchmarks for evaluating credit risk.

Minimum Score Requirements of Popular Banks

While analyzing your CIBIL Report, you should compare your current standing against the baseline requirements of India’s leading banks. Here is what you generally need to avoid an immediate rejection.

| Bank | Minimum Score |

| SBI | 700 |

| HDFC | 750 |

| ICICI | 720 |

| Axis | 700 |

| Kotak | 720 |

As the table highlights, private institutions like HDFC are heavily protective and demand premium numbers. If your profile is currently falling short of these targets, reviewing unlock 750+: a step by step plan on how to improve your CIBIL score is a smart move before applying.

Minimum CIBIL Score for SBI Loan

The State Bank of India (SBI) is the nation’s largest public sector bank and a preferred choice for millions. Typically, the minimum CIBIL score for SBI loan approval rests firmly at 700.

However, simply meeting this baseline does not guarantee the cheapest interest rates. For crucial products like housing finance, SBI heavily rewards applicants who cross the 750 mark with special processing fee waivers and discounted EMIs.

If your score is borderline and a sudden error pulls it down, you must know how to dispute errors on your CIBIL report to protect your eligibility.

Conversely, if an application is unexpectedly declined despite meeting the threshold, do not panic. Review what to do after credit card application rejected: best 3 step solution to understand how internal bank policies work. Always consult the official SBI website to verify their current credit tier requirements before submitting any fresh applications.

Factors That Influence Your CIBIL Score

To fully understand What Is a Good CIBIL Score in India, you must know exactly how the algorithm calculates your three-digit number. When checking your CIBIL Report and Credit Report parallelly, you will notice four core pillars that lenders constantly monitor.

Payment History

This is the single most critical factor in your financial profile. According to the official CIBIL website, consistently paying your EMIs and credit card bills on time builds supreme trust with banks.

Even one minor delay can drastically pull down your rating. For example, if you face the critical reality of same day NACH bounce impact on CIBIL score, you must act immediately to clear the dues and protect your profile.

Credit Utilization Ratio

Lenders closely watch how much of your available credit you actually spend. As a practical banking rule, you should keep your credit card balances below 30% of your total approved limit.

Maxing out your limits frequently signals financial distress to institutions like HDFC or ICICI. To manage this effectively, consider reading the ultimate guide to paying your credit card bill before the statement date to keep your reported balances low.

Length of Credit History

A longer, well-maintained track record gives banks more historical data to evaluate your reliability. Retaining your older credit cards is a smart strategy to maintain a solid average account age.

If you absolutely must shut down an old account, ensure you learn how to close a credit card without affecting CIBIL score in easy 5 steps.

Multiple Loan Inquiries

Every time you apply for new credit, banks trigger a hard inquiry on your profile to assess your risk. Applying for several loans simultaneously makes you appear credit-hungry, causing an instant drop in your score.

To protect your profile during major purchases, discover how 1 mistake triggers multiple CIBIL inquiries and avoid submitting applications to multiple banks at the exact same time.

Common Mistakes That Damage Your CIBIL Score

Maintaining a strong financial profile requires constant vigilance and discipline. Even if you already know exactly what is a good CIBIL score in India, a few careless financial habits can pull your numbers down drastically.

Let’s look at the most frequent errors everyday borrowers make that hurt their credit profiles.

Missing Credit Card Payments

Your repayment history is the absolute backbone of your credit report. Skipping an EMI or delaying a credit card bill immediately signals financial distress to major lenders like SBI or ICICI.

Even a single default is reported directly to the credit bureaus. If you are new to revolving credit, you must understand the severe consequences of a missed first credit card payment to avoid long-term penalties.

Loan Settlements

Many borrowers mistakenly think settling a distressed loan for a lesser amount closes the chapter cleanly. However, according to official CIBIL guidelines, a “settled” status severely damages your creditworthiness.

Banks view a settlement as a direct financial loss. To understand the severe long-term impact on your file, you should explore the harsh realities of loan settlement vs loan closure credit report.

Too Many Credit Applications

Applying for multiple credit cards or personal loans within a short time window makes you look credit-hungry. Each formal application triggers a hard inquiry by the bank, which temporarily drops your score.

Always pace your applications carefully. It is crucial to learn how 1 mistake triggers multiple CIBIL inquiries so you do not accidentally ruin your chances of future approvals.

High Credit Utilization

Maxing out your credit limits every single month shows a high dependency on borrowed money. Financial experts and major banks generally recommend keeping your credit utilization ratio strictly below 30%.

Consistently crossing this threshold hurts your overall rating. Try to clear your outstanding balances early before the statement date to keep your reported utilization ratio in check.

Frequently Asked Questions About Good CIBIL Score

As we conclude our comprehensive guide on What Is a Good CIBIL Score in India, you might still have a few specific scenarios in mind. Here are clear, straightforward answers to the most common borrower queries.

What is a good CIBIL score for home loan?

According to most major bank websites, a strong profile for housing finance typically starts at 700. However, to unlock the absolute lowest EMI rates and processing fee waivers, aiming for 750 or higher is highly recommended.

Can I get a loan with 650 CIBIL score?

Yes, it is possible, but your options will be severely limited. Since banks classify 650 as a “Fair” or medium-risk score, you will almost certainly face harsh interest rates.

Furthermore, the bank might demand a co-applicant to secure the funds. Be cautious with this, as a default can easily lead to a 7-year CIBIL nightmare for a loan guarantor in India.

Is 750 CIBIL score good for personal loan?

Absolutely. A 750 rating is universally recognized as the premium benchmark by financial institutions across the country.

Holding this excellent score gives you strong negotiating power. It ensures quick, hassle-free approvals and the cheapest possible interest rates on unsecured personal credit.

What is the minimum CIBIL score for SBI loan?

While specific underwriting rules vary depending on the exact financial product, the standard minimum requirement for most SBI loans is 700.

If your number suddenly drops below this threshold right before applying, you must learn how to dispute errors on your CIBIL report to correct the issue and restore your eligibility quickly.