Don’t know What to Do After Credit Card Application Rejected? This guide reveals the #1 mistake to avoid. Learn the expert plan for What to Do After Credit Card Application Rejected.

The Frustrating “You Have Been Rejected” Email

The Sinking Feeling of Rejection

You found the perfect credit card, filled out the application with excitement, and waited. Then the email arrives. “We regret to inform you…” It’s a frustrating and often embarrassing moment that leaves you with one big question:

What do I do now? This is especially critical if you are planning for a major life goal, as a pattern of rejections can even impact your eligibility for a home loan with a low CIBIL score.

This is a situation I’ve helped countless readers navigate. A rejection feels like a final judgment, but it’s actually a valuable piece of feedback if you know how to read it.

The most important step in figuring out What to Do After Credit Card Application Rejected is understanding the hidden message the bank is sending you.

The Golden Rule: Your First Move is to Do Nothing

My name is Anwar Hashmi, and I’m going to give you the most important piece of advice right now. Your first instinct might be to immediately apply for a different card. This is the single biggest mistake you can make.

This guide is your strategic action plan. It will show you exactly What to Do After Credit Card Application Rejected, starting with this crucial “cooldown” period.

We will turn this frustrating moment into the first step of your successful comeback story. Learning What to Do After Credit Card Application Rejected is about being strategic, not reactive.

Why Your Application Was Rejected: Becoming a Credit Detective

After the initial frustration of a rejection, the most pressing question is always, “Why?” Unfortunately, the reason provided by the bank is often a vague and unhelpful phrase like “does not meet our internal credit policy.” This can leave you feeling powerless and in the dark.

But in my experience, this is almost always a code phrase. The “internal policy” is, in over 90% of cases, directly related to a specific issue on your CIBIL or Credit Report. Your first step in figuring out What to Do After Credit Card Application Rejected is to stop guessing and start investigating. It’s time to become a credit detective.

It’s Almost Always Your CIBIL Report

Lenders are data-driven. Their decision to approve or reject you is based on the story your financial history tells. While factors like your income and employment stability matter, the initial and most important filter is your credit history.

A bank’s internal policy is designed to minimize their risk, and your CIBIL report is the primary tool they use to assess that risk. A low score, a high debt level, or a history of missed payments are all red flags that their automated systems are programmed to catch.

Therefore, the answer to What to Do After Credit Card Application Rejected always begins with a deep dive into your own credit file.

Your “Rejection Audit” Checklist

Before you can form a recovery plan, you need a precise diagnosis. Your first action should be to download your free, official CIBIL report. You are legally entitled to one free report per year from each of the four credit bureaus. This report is your evidence, your diagnostic tool that will reveal the exact cause of the rejection.

Once you have your report, use this detailed checklist to perform a “Rejection Audit.” This is the most crucial part of learning What to Do After Credit Card Application Rejected.

Checking for a Low CIBIL Score (Below 720-750)

This is the most common reason. Look at your three-digit score. While there is no “official” cutoff, most banks prefer applicants with a CIBIL score of 750 or above for their prime credit card products. If your score is below 720, it was likely the primary reason for your rejection.

Checking for a High Credit Utilization Ratio

This is the “silent killer” for many applicants. Look at each of your existing credit cards on the report. Is the “Current Balance” on any single card close to its “High Credit” or limit? A Credit Utilization Ratio above 40-50% on any card is a major red flag, even if you pay on time.

Checking for Recent Late Payments or Negative Remarks

Scrutinize the 36-month payment history for every account. Lenders are particularly sensitive to recent mistakes. A single payment that was late by 30 or 60 days in the last 6-12 months can be enough to trigger an automatic rejection, as it signals current financial instability.

Checking for Too Many Recent Hard Inquiries

Look at the “Enquiries” section of your report. If you have applied for multiple loans or credit cards in the last 3-6 months, you will see several “Hard Inquiries.” Too many inquiries in a short period make you look “credit hungry” to lenders, which is another common reason for rejection.

Checking for Errors on Your Credit Report

Finally, read through every line of your Credit Report. Is there an account listed that isn’t yours? Is a loan you paid off still showing as active? A simple reporting error could be the culprit, and this is a critical check for anyone wondering What to Do After Credit Card Application Rejected.

If you do find an inaccuracy, the good news is that you have the right to get it fixed, and our in-depth guide on how to dispute CIBIL report errors provides a complete, step-by-step framework for the entire process.

By the end of this audit, you will have moved from a state of confusion to one of clarity. You will no longer be guessing; you will have a precise list of the issues you need to fix. This diagnosis is the foundation of a successful plan for What to Do After Credit Card Application Rejected.

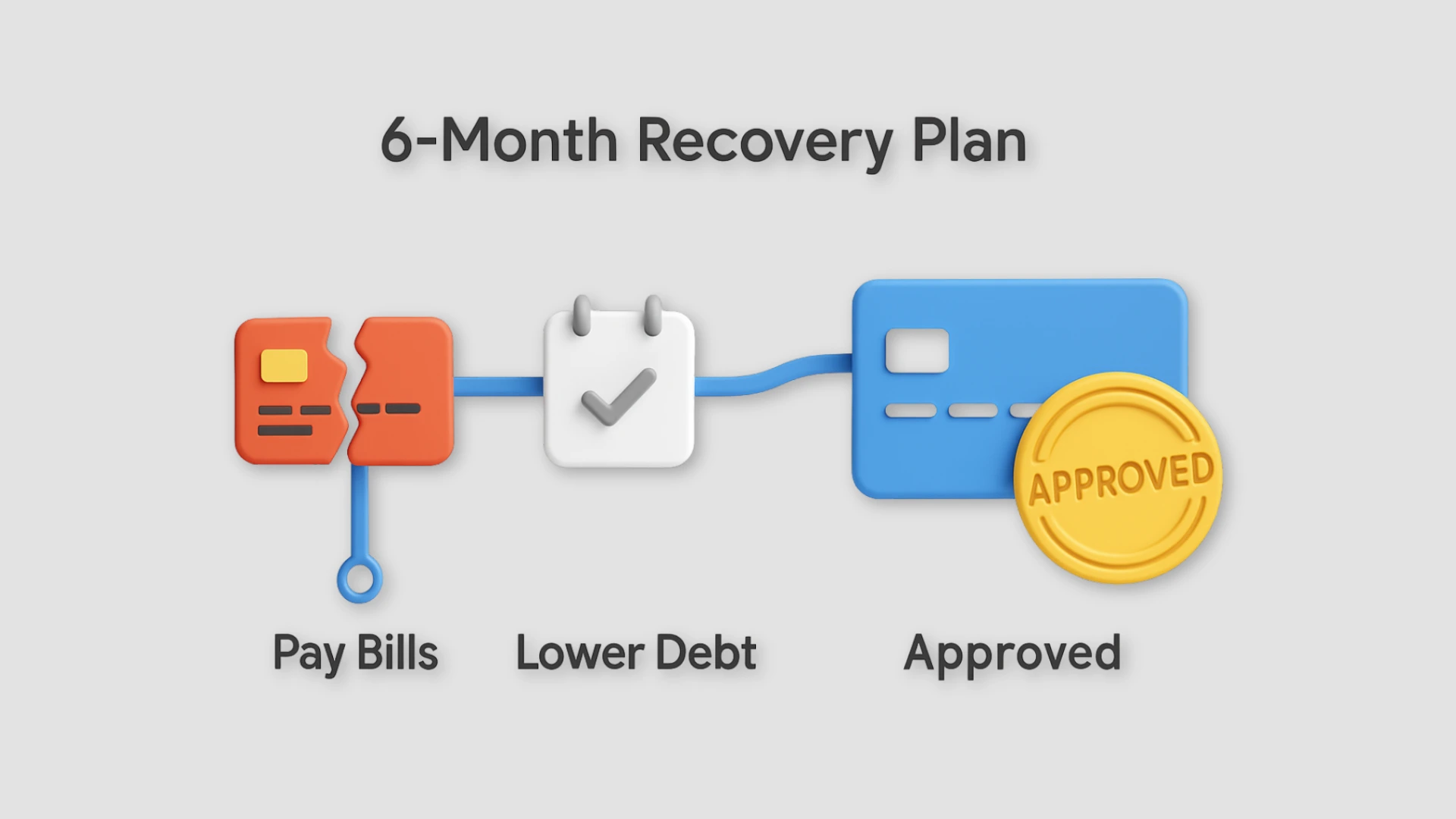

The Strategic Waiting Period: How Long to Wait After a Rejection

You’ve done the hard work of diagnosing your Credit Report. You now have a clear list of the exact issues that likely led to your rejection. The immediate temptation is to fix them and then quickly re-apply. However, the next step in our strategy is the most important, and for many, the most difficult: patience.

In my experience as a financial writer, the period after a rejection is where you can either set yourself up for future success or dig yourself into a deeper hole. Acting too quickly is a common mistake.

This section will provide a clear, strategic framework for this “credit cooldown” and explain exactly What to Do After Credit Card Application Rejected to ensure your next application is a success.

Why the 6-Month Rule is Your Best Friend

After a credit card application is rejected, the single most important piece of advice I can give you is to wait a minimum of six months before applying for any new form of credit. This isn’t an arbitrary number; it’s a strategic timeline based on how the CIBIL scoring algorithm works.

When you apply for a credit card, the lender creates a “hard inquiry” on your CIBIL report. While a single inquiry has a minor impact, multiple inquiries in a short period are a major red flag. By waiting six months, you achieve two critical goals:

- The Impact of Old Inquiries Fades: Hard inquiries have the biggest negative impact on your score for the first six months. By waiting, you allow that impact to diminish significantly, presenting a cleaner report to the next lender.

- You Build a New, Positive History: Six months is the minimum amount of time needed to establish a new, positive pattern of financial behaviour. It gives you enough time to make six consecutive on-time payments and significantly lower your credit utilization.

This waiting period is a non-negotiable part of any successful plan for What to Do After Credit Card Application Rejected. It transforms you from a “risky, recent applicant” into a “stable, recovering borrower” in the eyes of the lender.

What to Do During Your “Credit Cooldown”

This six-month period is not about passively waiting. It is your active training period. This is where you fix the problems you identified in your audit and build the strong credit profile that will guarantee your next approval. This is the core of What to Do After Credit Card Application Rejected.

Use this checklist as your month-by-month action plan.

Your 6-Month “Credit Cooldown” Checklist

- [ ] Month 1: The “Quick Wins”

- If you found any errors on your Credit Report, file a dispute with CIBIL immediately. Correcting a major error is the fastest way to see a score boost.

- Begin aggressively paying down your credit card balances using the “Avalanche” or “Snowball” method to lower your Credit Utilization Ratio.

- [ ] Months 2-5: Build a Flawless Track Record

- Make every single EMI and credit card payment on time, without fail. Set up auto-pay and calendar reminders to make it impossible to forget.

- Continue to pay down your credit card debt, with the goal of getting your overall utilization well below 30%.

- [ ] Month 6: The Final Review

- Download a fresh copy of your CIBIL report.

- Verify that any disputed errors have been corrected.

- Confirm that your payment history for the last six months is perfect.

- Check that your Credit Utilization Ratio is low.

By the end of this period, you will have a much stronger credit profile. This structured approach is the definitive answer to What to Do After Credit Card Application Rejected.

Instead of just hoping for a better result, you have actively built one. This is exactly What to Do After Credit Card Application Rejected to ensure your next application is successful.

Your 6-Month “Re-Application” Action Plan

You’ve completed your “Credit Cooldown” and have spent the last six months building a stronger financial profile. Now, it’s time to move into the final phase: applying again, but this time with a clear, confident strategy.

This is where we put all our hard work into action and provide the final, successful answer to the question of What to Do After Credit Card Application Rejected.

This is not about simply trying your luck again. This is a calculated plan to ensure your next application is a success. We will break this down into three distinct phases.

Month 1: The “Quick Wins”

The first month of your recovery plan is all about tackling the high-impact issues you identified in your credit report audit. This is the most critical part of What to Do After Credit Card Application Rejected, as it provides the fastest possible boost to your score.

Your two primary objectives for this month are:

- Dispute All Errors: If your audit revealed any inaccuracies—a fraudulent account, an incorrect late payment, or a paid-off loan still showing as active—you must file a dispute with CIBIL immediately. Correcting a major error is the single most powerful action you can take.

- Pay Down High Credit Card Balances: Your second objective is to aggressively attack any credit cards with a high Credit Utilization Ratio (CUR). Use the “Avalanche” or “Snowball” method to pay down your balances. Getting your overall CUR below 30% is a massive positive signal to the CIBIL algorithm.

Months 2-6: Building a Flawless Track Record

This is the phase where you prove that your positive changes are not a one-time fix, but a new, permanent habit. Consistency is the most important factor for lenders. For the next five months, your only job is to build a flawless track record of financial discipline.

During this period, you must:

- Make Every Single Payment On Time: Set up auto-pay for minimum dues as a safety net and use calendar reminders to pay the full balance before the due date. Six consecutive months of perfect payments is a powerful signal that your past mistakes are truly in the past.

- Keep Your Utilization Low: Continue to keep your credit card balances low. Never let your overall CUR creep back up above the 30% mark.

This period of consistency is the core of What to Do After Credit Card Application Rejected. It rebuilds the trust that was lost.

The Re-Application Strategy: Applying with Confidence

After your six-month action plan is complete, you are now in a position of strength. Your CIBIL score will be significantly higher, and your Credit Report will show a recent history of perfect financial management. Now, you can apply again, but this time, you will do it strategically.

The key is to apply for a card that matches your now-improved score. Do not make the mistake of immediately applying for a premium travel card. Your goal is to get a solid approval to continue building your positive history.

- If your score is now in the 680-720 range: Apply for a basic, entry-level, “no-frills” credit card from your primary bank where you have a savings or salary account. They are more likely to approve you as an existing customer.

- If your score is still below 680 or you had a major negative mark: Your best strategy is to apply for a Secured Credit Card. This is a card backed by a fixed deposit that is almost guaranteed to be approved. Using this card responsibly for another 6-12 months is the surest path to a 750+ score.

This intelligent, tiered approach is the final, crucial step. It proves you understand not just What to Do After Credit Card Application Rejected, but how to turn that rejection into a guaranteed approval. This is exactly What to Do After Credit Card Application Rejected to ensure long-term success.

Frequently Asked Questions After a Credit Card Rejection

1. What are the common reasons for credit card rejection besides a CIBIL score?

Besides a low score, the most common reasons for credit card rejection include a high Debt-to-Income ratio, unstable employment history, or errors in your application form. However, even these reasons for credit card rejection are often linked back to the overall health of your credit profile.

2. If I know my score is low, what’s the first step in what to do after my credit card application is rejected?

The absolute first step in What to Do After Credit Card Application Rejected is to get your latest CIBIL report and perform a detailed audit. You cannot form a successful recovery plan for What to Do After Credit Card Application Rejected until you identify the specific issues, like late payments or high utilization, that are pulling your score down.

3. How does a high credit utilization ratio lead to a rejection?

A high credit utilization ratio (above 30%) signals to lenders that you are overly dependent on credit, making you a high-risk applicant. Even with a decent score, a high credit utilization ratio is a major red flag that can be the primary cause of a rejection.

4. Will one recent late payment cause my application to be rejected?

Yes, a single recent late payment in the last 6-12 months can absolutely cause a rejection. Lenders place the most weight on your recent behaviour, and a recent late payment is a powerful indicator of current financial instability.

5. What is the single biggest mistake to avoid when figuring out What to Do After Credit Card Application Rejected?

The single biggest mistake in desiding What to Do After Credit Card Application Rejected is to panic and immediately apply for another card. This adds another hard inquiry to your report, making you look “credit hungry” and further damaging your score. The correct first step for what to do after credit card application is rejected is always to pause and diagnose the problem.

6. How long to wait after a credit card rejection before applying again?

The strategic answer for how long to wait after a credit card rejection is a minimum of six months. This “credit cooldown” period allows the negative impact of the hard inquiry to fade and gives you a crucial window to actively improve your score, ensuring you know how long to wait after a credit card rejection for the best results.

7. Do banks tell you the specific reason for a credit card rejection?

Banks are not legally required to provide a specific reason for a credit card rejection, often citing vague “internal policies.” However, these policies are almost always based on your CIBIL report, which is why a self-audit is the best way to understand the true reason for a credit card rejection.

8. How do too many recent hard inquiries affect my chances of approval?

Having too many recent hard inquiries (more than 2-3 in six months) signals high risk to lenders. Even with a good score, too many recent hard inquiries can be a primary reason for rejection, as it suggests you may be in financial distress.

9. How does my CIBIL report help me figure out what to do after my credit card application is rejected?

Your CIBIL report is your roadmap. The answer to what to do after credit card application is rejected lies within that document. By auditing your report, you can identify the exact “score killers”—like high utilization or late payments—that need to be fixed, which is the core of what to do after credit card application is rejected.

10. Will finding and disputing errors on my credit report help my next application?

Absolutely. Finding and disputing errors on your credit report is one of the most powerful actions you can take. If a significant error is corrected, your score can jump dramatically, which is why checking for errors on your credit report is a critical step in your recovery plan.

11. What is the best way how to get approved for a credit card after rejection?

The best way how to get approved for a credit card after rejection is to follow a disciplined 6-month plan: fix any errors, pay down debt, and build a perfect payment history. The most effective strategy for how to get approved for a credit card after rejection is to re-apply from a position of strength, not desperation.

12. Is applying for a secured card a good plan for what to do after my credit card application is rejected?

Yes, it’s an excellent plan. A key part of what to do after credit card application is rejected is to rebuild your credit history. A secured credit card is almost guaranteed to be approved and allows you to build a new, positive payment record, making it a perfect tool for what to do after credit card application is rejected.

13. Can I apply for a different card from the same bank after credit card application was rejected?

You can, but it is not recommended until you have waited at least six months and have improved your credit profile. If a bank’s system has already flagged your profile as risky, a new application will likely be rejected for the same reasons. Dealing with a credit card application that was rejected requires fixing the root cause first.

14. Does my income level matter more than my low CIBIL score?

For credit cards, a low CIBIL score is often a more significant factor than a high income. Banks see a low CIBIL score as a sign of poor credit management, which even a high salary cannot always overcome.

15. What is the ultimate goal of any strategy for what to do after my credit card application is rejected?

The ultimate goal is not just to get a card, but to build a strong credit profile that opens doors to all financial products. The plan for what to do after credit card application is rejected is a chance to reset your financial habits. The real victory in knowing what to do after credit card application is rejected is the lasting improvement in your financial health.

16. Is a secured credit card a guaranteed approval after a rejection?

While not 100% guaranteed, a secured credit card has the highest approval rate of any credit product because you provide a fixed deposit as collateral. For someone with a damaged credit history, a secured credit card is the most reliable path to rebuilding a positive track record.

From Rejection to Approval: Your Path Forward

Receiving that “rejected” email can feel like a final verdict, a frustrating dead end. However, as this guide has shown, it is not a failure. A credit card rejection is one of the most valuable pieces of data you can receive. It is the bank giving you a free, expert analysis of the weakest link in your Credit Report.

The key takeaway is to transform this moment from one of frustration into one of strategy. By following the “credit cooldown” period and the 6-month action plan, you are no longer guessing what to do after credit card application is rejected; you are executing a proven plan. You are taking control, fixing the root cause of the problem, and building a stronger financial profile.

This plan is your first step. For a complete masterclass on all the strategies to build a high score, from mastering your payment history to advanced utilization hacks, our main pillar post,

The Ultimate Guide to Improving Your CIBIL Score, provides a comprehensive, step-by-step plan. It is how you turn a frustrating setback into your most powerful comeback story.

Author’s Note

A Note from the Author: The question of what to do after credit card application is rejected is one of the most stressful and confusing moments in personal finance. I wrote this guide to replace that panic with a calm, strategic action plan that puts you back in control.

- Anwar Hashmi, founder of

cibilized.in. For expertise on American finance, he is also the lead author atClaimCredits.online, specializing in USA Tax Credits.